In the world of personal finance, where content and potential money-making opportunities are like sand on the beach, it’s way too easy to get lost.

Where do you even start? And what should you focus on?

I set out to condense the core areas you must take note of, and organised them in a way that is simple to understand, yet does not lack in depth.

The result of this is what I call the wedding cake strategy, and it’s my own take on how to significantly improve your personal finances, starting today.

As this topic is wide, throughout this article, there will be links to the related subtopics if you wish to explore them.

Note: this content should not be taken as formal financial advice.

In a Nutshell

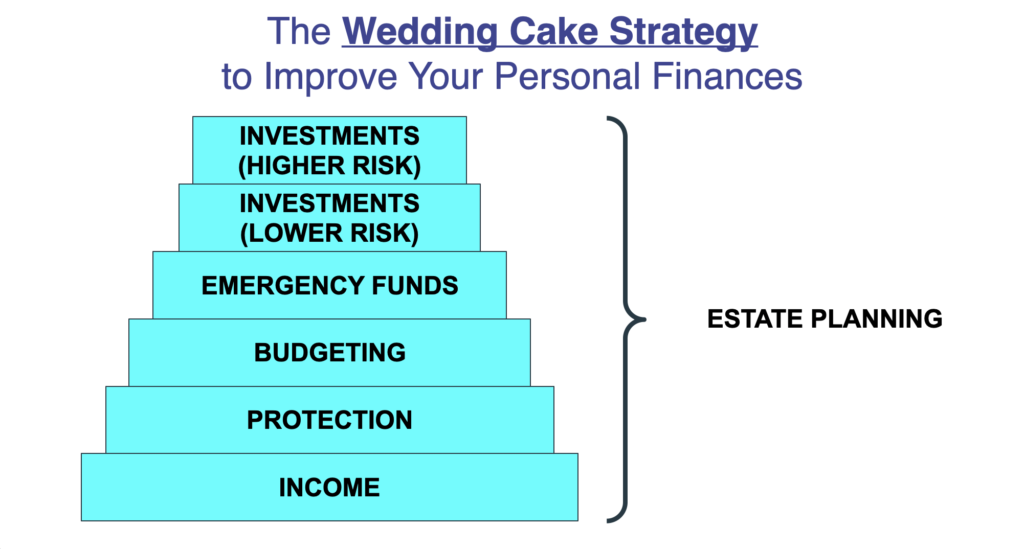

To build a wedding cake, you no doubt have to start from the bottom layer and work your way up. The bottom layers thus have greater importance.

Correspondingly, finances should be built in a similar fashion.

Here’s a snippet of the wedding cake strategy.

While it may look simple, and is intended to appear so, there is much more to this strategy than first meets the eye. In the following sections, I’ll not only cover surface-level information, but I’ll also dive deep into each of its components and the vital role they play in the big picture.

I’m certain you’ll gain valuable insights from reading further.

SIDE NOTE When was the last time you conducted thorough financial planning or reviewed your finances? In this day and age in Singapore, doing so will absolutely improve the quality of life for you and your loved ones. Here are 5 reasons why financial planning is so important.

What Is Personal Financial Planning?

To start off, let’s touch on something boring — what’s financial planning?

If you do a quick Google search, you’ll find fanciful definitions with intimidating financial jargon. Some will even give descriptions rather than definitions.

Really, the actionable answer just involves two things: Point A, which is where you’re currently at financially, and Point B, which is where you want to be financially.

Through the process of financial planning, you create a financial plan that enables you to get from Point A to Point B. And that’s extremely critical to improve the quality of life for you and your family.

Below are seven steps to help you reach your financial goals.

However, don’t worry too much if you’re unable to do all of them right now. This process of planning your finances is a marathon and not a sprint. Doing more than what you’re accustomed to increases the likelihood of you giving up entirely. The trick is to get moving and take small steps. This way, you won’t keep putting it off indefinitely.

1) Increase Income

Your income is the heart of everything.

It provides you the ability to pay for daily expenses, fulfil your financial responsibilities and commitments, and help you save for the future.

In my opinion, one of the best investments you can make is in your career (or business), especially in the early stages of life.

Businesses, big or small, are always for-profit. They want competent people who can help them increase revenue or reduce costs.

By being an expert at what you do (through constant learning, upgrading yourself and your skill sets, having professional qualifications, being proactive, etc), businesses depend on you.

And in order to retain you, they will offer you greater monetary rewards through pay increments, promotions, bonuses, etc.

So, if you focus on building your career, generally, you’ll have fewer issues with being able to provide financially. However, doing so does take tremendous effort and focus. Fortunately, you can still outsource the management of the rest of your finances.

Another way to increase income is to have a well-selected side hustle. Who knows? It could become a full-blown business in the future.

Apart from the above, there are two aspects that tie directly into your earned income, and those are CPF and taxes.

I take the view that we must be well-acquainted with how they work, as they have a material impact on our finances.

For example, tax reliefs and deductions enable you to reduce your taxable income, thus paying fewer tax dollars and saving more in the process.

Without knowing the ways to increase tax reliefs, such as contributing into your Supplementary Retirement Scheme (SRS) account, you may not be taking full advantage of the tools at your disposal.

Yes, reading about them may seem complex at first, but they are necessary.

2) Get Protection

If your income is everything, wouldn’t it make sense to ensure its continuity?

There are three events that could cripple your income-earning ability:

- Death

- Total and permanent disability (TPD)

- Critical illness (CI) or early critical illness (ECI)

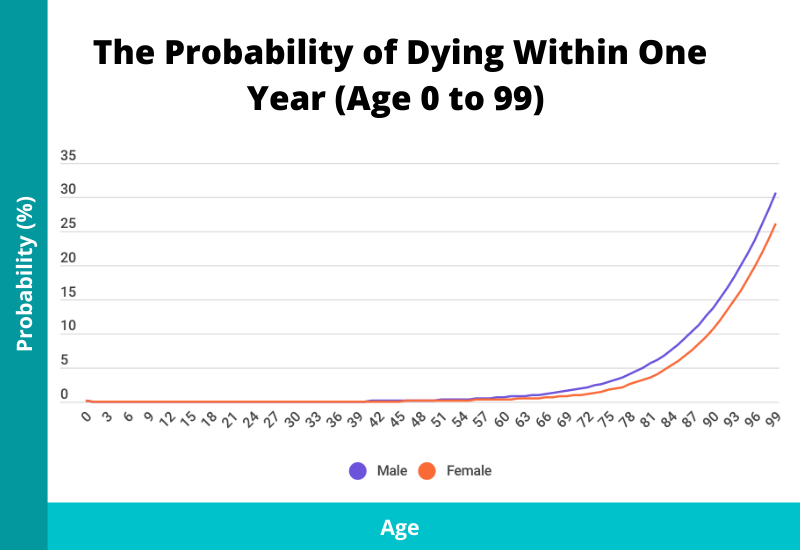

Statistically speaking, the occurrence of such events is much higher in the later stages of life.

But it’s not always as simple as that.

The same set of statistics also shows that these events can happen at any point of time, potentially causing a financial disaster for you or your family.

Thus, you should protect your income and your wealth through insurance.

I’ve assisted in submitting a few death claims before, and my heart always sinks whenever I do it, especially when I know the deceased and their family members well. Nobody wants to claim from insurance, but I can absolutely assure you that you’d never want your loved ones to take on any financial burdens if you were taken out of the picture.

This means having the right type of insurance plans with an adequate amount of coverage.

The financial risks that come with the above events can be reduced by having life insurance coverage, usually through a term insurance plan or a whole life insurance plan, as the lump-sum payout can replace the loss of income.

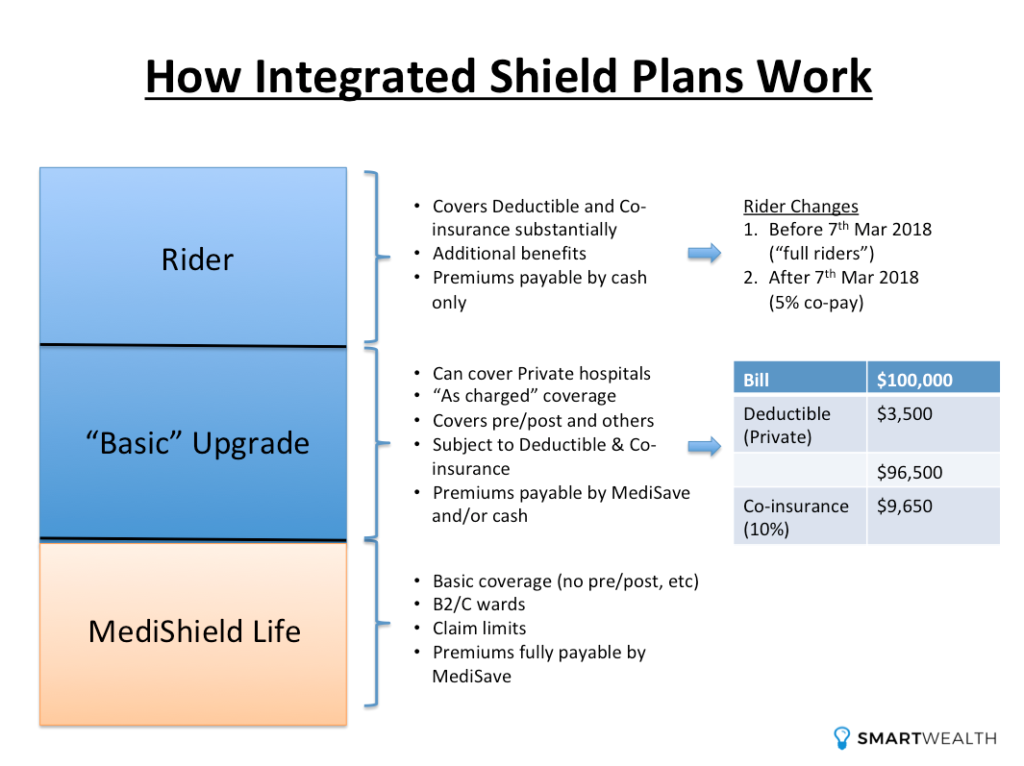

Apart from having sufficient life insurance coverage, medical or hospitalisation insurance is essential, even until old age. The hospital is where you’ll first go if injuries or illnesses happen. With the cost of healthcare increasing, if a huge medical bill is presented to you, you may need to dig into your hard-earned savings, sell off your beloved assets (properties, investments, etc), or even go into debt.

However, that risk can be substantially reduced if you have the proper coverage. MediShield Life coupled with the Integrated Shield Plan (IP) remain the best options for Singaporeans.

The government also has initiatives such as CareShield Life and ElderShield to provide payouts meant for long-term care when severe disabilities happen. You’re able to get better benefits if you upgrade with an insurer’s supplement.

Those are some of the common options for you to consider.

If you’re currently healthy, have no dependants, or your family has no medical history, and you don’t see a need for insurance now, know that every small ailment can affect your insurability in the future.

Getting insurance is paradoxical: when you need it the most, you won’t be able to get it.

Whatever insurance you choose, make sure that the premium makes sense (e.g., you can afford it) and is reasonable considering the coverage you will get. I would advise you to take the time to sit down and talk to a financial planner to review what you have.

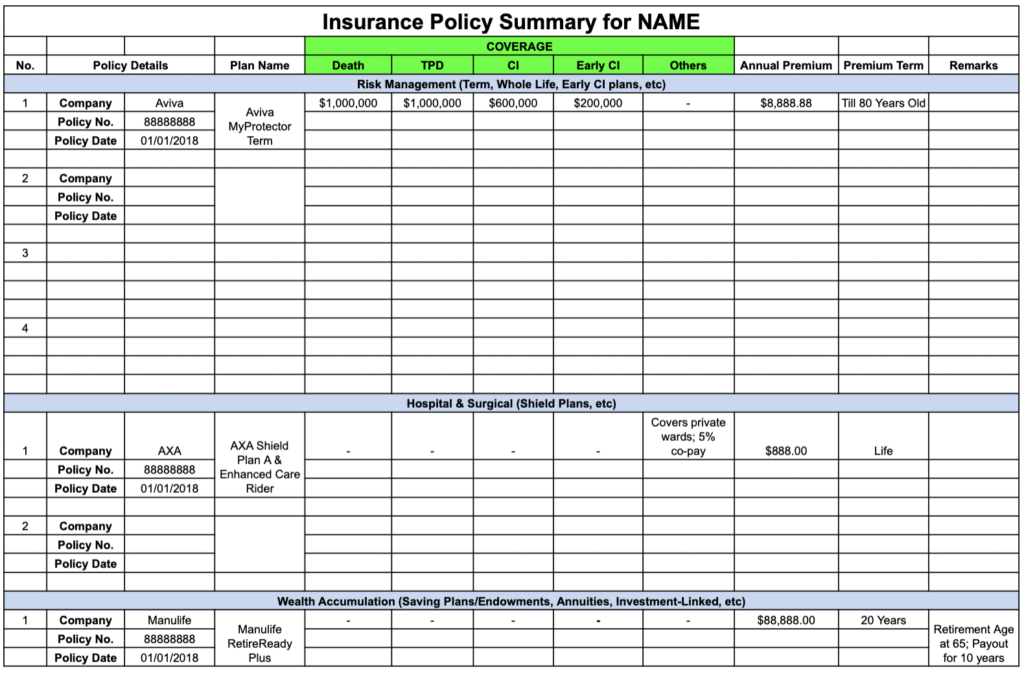

To wrap up this section, a lot of people I speak with don’t know what they’ve bought, such as how much they’re covered for and what type of plans they have. If you’re one of those people, do yourself and your family a favour by consolidating what you have with a simple insurance policy summary.

Here’s a template you can use for free. You can make a copy or download it as an Excel file.

3) Perform Budgeting

Knowing how much you spend (and thus save) is a foundational element to good financial planning, as you wouldn’t be able to improve what you didn’t measure.

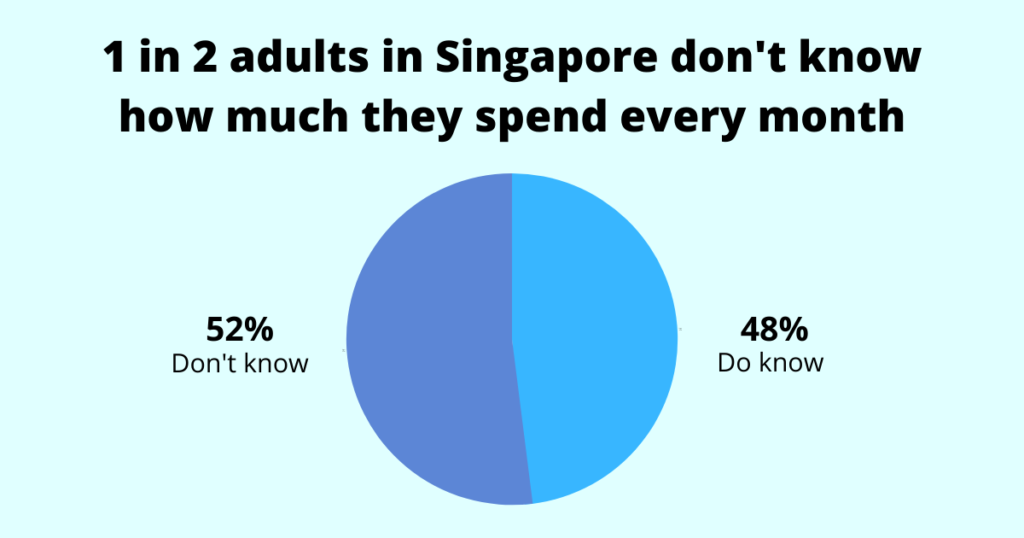

Unfortunately, in a survey we conducted, 52% of adults in Singapore are clueless as to how much they spend every month. And they’re likely to only save what’s left (if at all).

Therefore, a good practice is to budget your money, which is to preemptively decide how much of your income (percentage or absolute dollars) goes towards “needs”, “wants”, and “savings”. One budgeting rule you can start off with is the 50/30/20 rule. However, as everyone is different, you should tweak the ratios according to your situation and your preferences.

Your budget does not have to be rocket science. What’s important is that it’s a sound budget and one which you can stick to.

To further reduce mental resistance, once you receive your monthly salary, you should transfer out that specific savings amount (preferably using a standing instruction) into another savings account to be left there or await being invested. This ensures that you’re always saving first rather than later.

At this point, what you have left in your account is the amount you can spend on “needs” and “wants”. However, because of emotional spending, there can still be a tendency to overspend with impulsive purchases. To reduce the chances of this happening, consider keeping track of your expenses. You can use a mobile app, an online calculator, or a budgeting template. To further improve on the way you spend, for each item, decide whether to keep it, find a better/cheaper alternative, or eliminate it entirely.

(I personally don’t track every purchase I make. I consolidate all my expenses into one statement and just review them once a month.)

Whether you’re noting down every expense item or simply reviewing the transactions you’ve made that month, you’re sure to benefit from it.

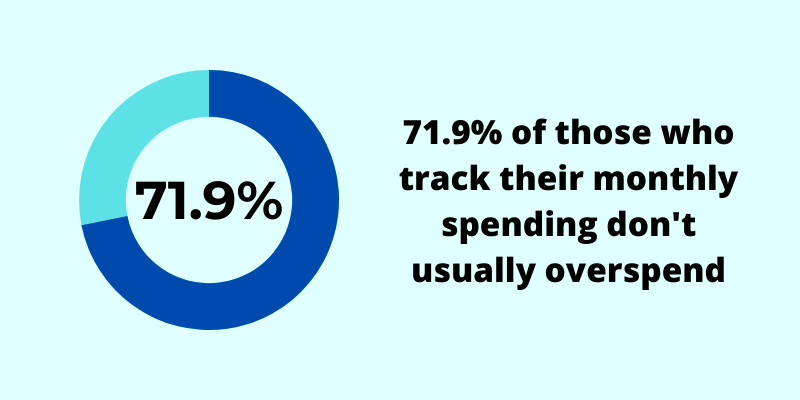

In the survey we conducted, we found that 71.9% of those who keep track of their monthly spending don’t usually overspend.

4) Hold Emergency Funds

Having done the above, you should have more money saved.

What should you do with your savings?

The first priority is to have an emergency fund of six-12 months of expenses. In light of the COVID-19 pandemic, which caused an extended period of disruption, I’d prefer to have 12 months of emergency funds.

Here are some examples of emergencies that could happen:

- Getting retrenched

- Needing major repairs

- Requiring immediate hospitalisation and surgery

- The death of a loved one

If these happen, you’ll need immediate cash.

If you don’t have enough, you may need to resort to borrowing or risk selling off your investments at a loss.

Having too many of these emergency funds (which are usually placed in highly liquid and low-interest-earning assets) isn’t that great either.

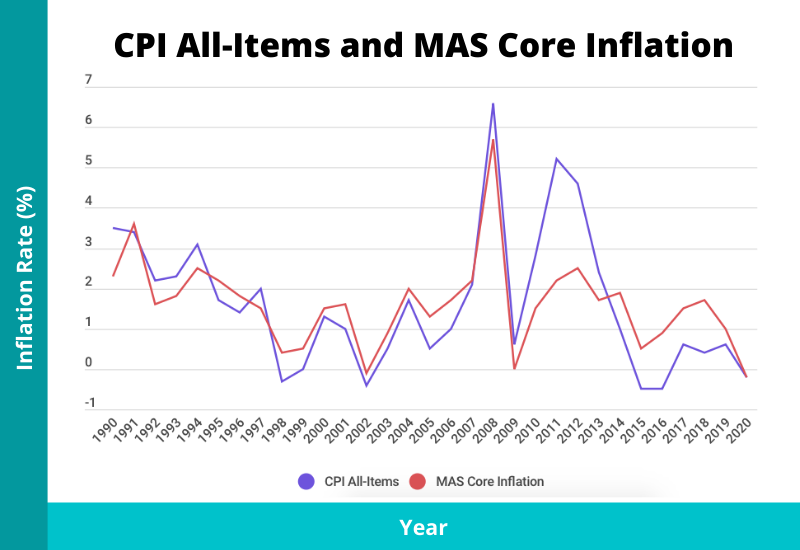

This is because over the past 20 years (2000 to 2020), the annual average core inflation rate was 1.52%.

So, holding some is more than enough because money left in low-interest instruments (e.g., a regular bank savings account giving 0.05% per year) is bound to devalue over time. And when you need it the most in the future, you might be in for a rude awakening.

Depending on how accessible you want your emergency fund to be, here are some options to consider:

- Regular bank savings account

- High-yield savings account

- Fixed deposits

- Singapore Savings Bonds (SSBs)

- Cash management accounts (although they can still go in the red)

You don’t need to choose just one; a mixture can work well too.

Apart from holding assets meant for emergencies, I believe the rest of your money should be invested, depending on your risk appetite.

5) Make Investments (Low-Risk & High-Risk)

When you’ve done the above, you will have protected yourself against major financial catastrophes and unexpected emergencies.

And if you’ve focused on your career and/or business and budgeted effectively, you’re likely to have excess cash.

Should you do something with the money you’ve saved up?

Most definitely yes, unless you’re absolutely sure that the income alone is sufficient to accommodate all your financial goals and you need nothing else.

But for most people, investing allows you to:

- Beat inflation

- Make your money work harder by getting higher potential returns so that you can achieve more in a shorter amount of time

Because it carries a certain degree of risk, you shouldn’t invest money meant for your emergency fund and very short-term goals. In short, it makes greater sense to invest in long-term financial goals, such as building your retirement fund or providing a university education for your children.

And you should invest according to your risk appetite.

Investments range broadly from low-risk to high-risk. And they both have their parts to play. For example, low-risk investments can provide stability and potential “ammunition” when markets are down. On the other hand, high-risk investments can represent growth.

I’m certain there are more than a million ways to invest, which makes it impossible to cover everything in this section.

In addition to the list of ways to park your emergency funds (which could be considered investments too), here are some other popular investment options:

- Properties

- Real Estate Investment Trusts (REITs)

- Retirement annuity insurance plans

- Individual stocks and shares

- Investment funds (ETFs, unit trusts)

- Cryptocurrencies and NFTs

In my opinion, a combination of different investments work better because of diversification.

But ultimately, it boils down to you. Here are some factors to consider:

- The degree of how hands-on you want to be

- The purpose of the investment

- The level of risk you’re willing to take

- Your current age

- Your investment time horizon

If you don’t know where to start or you choose to focus more on your career/business and want to take a hands-off approach, you should go through a financial planning session so that suitable solutions can be provided.

6) Do Estate Planning

Death is an inevitable part of life — it will come; the question is when.

Yet many of us steer away from thinking or talking about it.

In doing so, if it happens unexpectedly, would you or your family be caught unprepared?

Accepting your mortality can also be liberating, as it allows you to appreciate the here and now and live life more fully.

As to your assets and liabilities, do you really know what’s going to happen to them?

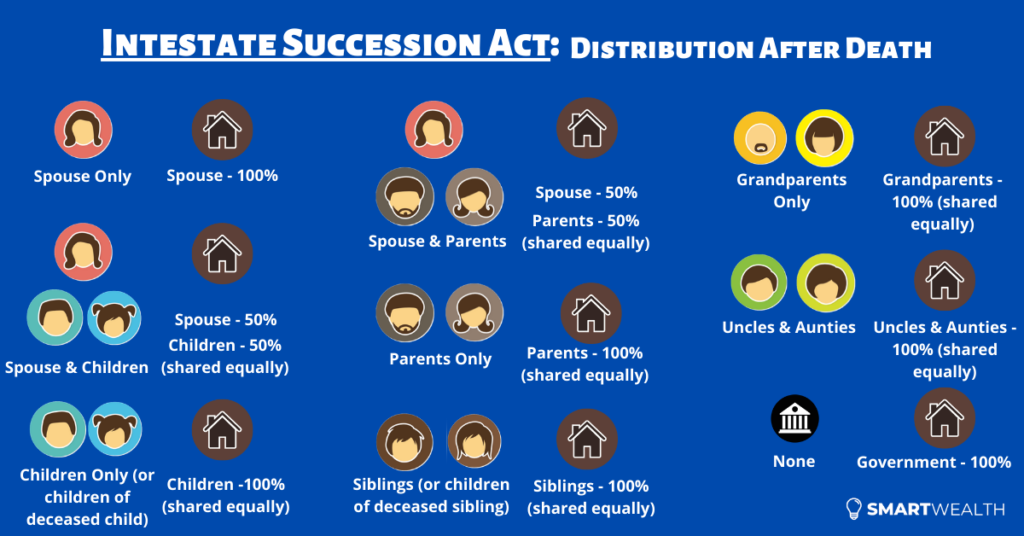

If you’ve done absolutely nothing, your assets are usually distributed according to the Intestate Succession Act or the Muslim law.

Apart from your assets not going to intended parties in a proportion you desire, your loved ones will find the process of “unlocking” your assets tedious and time consuming.

For example, in this digital age, where paper statements are becoming non-existent and your assets are all over the place in the digital world, your loved ones might not be able to uncover all that you have. Think cryptocurrencies.

There are three basic tools you can utilise, which are to make a CPF nomination (which can be done online now), to nominate your beneficiaries for some insurance policies, and lastly, to make a will.

While making a will may seem very formal (which it should be), it will spell out clearly what’s going to happen after death. It costs a few hundred dollars to get a will written up, but it saves a whole lot of time and hassle.

If you haven’t gotten to writing a will yet, at the very least, you should list your assets and liabilities all in one place, with their details. You can use this free template and share a copy with your loved ones. At least if anything happens, they’ll know exactly what you have and which entities to approach.

All these will kick in if death occurs. But what if you’re mentally incapacitated instead and can’t make any form of decision?

This is where advance care planning comes in, and like estate planning, it has to be done prior.

There are three tools you can consider using:

- Advance care planning workbook

- Lasting power of attorney (LPA)

- Advance medical directive

Collectively, they ensure your wishes towards healthcare, personal welfare, and your properties are spelt out and/or are handled by someone you trust.

These two areas (estate planning and advance care planning) are often overlooked and neglected, but they can make a huge difference to your next generation.

7) Review Regularly

Lastly, sound financial planning requires regular review.

Your situation, responsibilities, and objectives will change over time. And your financial plans will have to be tweaked accordingly — what worked in the past may not work in the future.

Set intervals where you review your finances and see whether there are some things you can change to protect or grow your wealth more efficiently. These can be reducing expenses, optimising your insurance portfolio, changing the ratio of savings, and looking for better-suited investment alternatives.

Do You Need Help in Financial Planning?

If you have reached this point, I hope you’ve benefited from this article in one way or another.

If you still don’t have a solid financial plan, don’t know where to start, or have lingering doubts, do consider going through a comprehensive financial planning session.

You can receive specific advice based on your situation and goals, which will be different from the person next to you.