Compare and get personalised quotes from 19 life insurance providers to find the best whole life insurance plan in Singapore for your needs.

What Is Whole Life Insurance & Why Is It Important?

The whole life insurance plan combines two things:

- Coverage

- Cash value

For those concerned about buying insurance without getting anything back (if there are no claims), a whole life plan might be just right for you.

Best Whole Life Insurance in Singapore (Comparison for 2026)

Here’s a non-exhaustive list of whole life insurance plans that we can compare:

| Insurance Company | Plan Name |

|---|---|

| AIA | Guaranteed Protect Plus IV |

| Singlife (formerly Aviva) | Whole Life Choice |

| HSBC Life (formerly AXA) | Life Treasure III |

| FWD | Life Protection |

| Manulife | LifeReady Plus II |

| Income Insurance (formerly NTUC Income) | Complete Life Secure |

Singlife Whole Life Choice

The base coverage for Singlife Whole Life Choice includes protection against death and terminal illness.

You can select an additional coverage amount of 100%, 200%, 300%, or 400% of the basic sum assured. This additional coverage will remain in place until your chosen additional cover age of 65, 70, 75, 80, or 85.

In addition to the base coverage, you can add riders for total and permanent disability (TPD), critical illness (CI), and early critical illness (ECI).

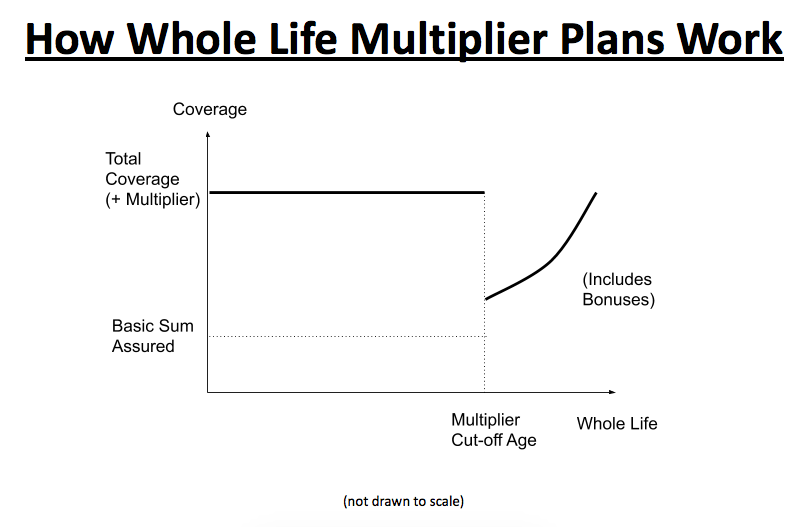

A unique feature of this plan is that, once the insured reaches the selected additional cover age, the additional coverage reduces by 12.5% each policy year for 8 years until it becomes 0. This gradual reduction period is longer than similar plans with phased reductions. This feature not only applies to the base cover (death and terminal illness) but also to eligible riders (TPD, CI, and ECI).

For premium payments, you can choose a term of 10, 15, 20, or 25 years, or pay up to age 65.

Promotion: For plans with an annualised premium of $4,000 or more, enjoy a 4% cashback on the first-year premium for premium terms of 10 years or more. This promotion ends on 31 August 2026.

HSBC Life – Life Treasure III

The basic cover includes protection against death, terminal illness, and TPD. You can add riders to cover CI and ECI.

The plan offers multiplying factor options of 2.5, 3.5, 4.5, and 6 times the basic sum assured.

The multiplier coverage age options are 65, 70, and 80.

This plan features a gradual reduction of the multiplied insured amount upon reaching the multiplier coverage age. The multiplier benefit decreases by 10% annually for the subsequent five years. After this, it remains at 50% for the rest of the policy term. For example, if your basic sum assured is $200,000 and you select a 3.5 times multiplier, you would have a coverage amount of $700,000 until age 70 (or the multiplier coverage age option you’ve chosen). This amount would reduce by $70,000 per year over the next five years, leaving a final figure of $350,000.

It’s important to note that this gradual reduction applies only to the basic coverage (i.e., death, terminal illness, and TPD). It does not affect CI and ECI riders.

Premium payment term options are 10, 15, 20, 25, and 30 years.

Manulife LifeReady Plus II

Manulife LifeReady Plus II offers protection with its base plan, covering death, terminal illness, and TPD. You can enhance your plan with riders that provide coverage for CI and ECI.

The plan includes coverage multiplier options of 1, 2, 3, 4, and 5 times the basic sum assured. The multiplier benefit is available until either age 70 or 80, depending on the option you select.

You have several choices for paying your premiums. You can opt for payment terms of 10, 15, 20, or 25 years, or extend payments up to age 99 — a rare option for similar plans.

A unique feature of this plan is its “Health Advantage” benefit. If you meet the prevailing underwriting guidelines at the time of application, you can enjoy a premium discount on the base plan for the first two years. This discount can be extended for subsequent years if you meet specific health targets. These targets are assessed through a form certified by a medical examiner. However, if the health targets are not met, the standard premium rate will apply. Terms and conditions apply.

Promotion: 10% discount on your first-year premiums. Offer is available until 30 June 2026.

AIA Guaranteed Protect Plus IV

The base coverage for AIA Guaranteed Protect Plus IV is on death and TPD. To enhance your plan, you can add optional riders for CI and ECI.

This plan allows you to choose between 2x, 3x, or 5x the basic sum assured. The multiplier benefit is available until the cutoff ages of 65 or 75.

Premium payments can be spread over 15, 20, or 25 years.

Income Insurance Complete Life Secure

Income Insurance Complete Life Secure provides a base cover that protects against death, terminal illness, and TPD. You can add riders for CI and ECI too.

The plan offers a minimum protection value of 100%, 200%, 300%, 400%, or 500% of the basic sum assured. This benefit is available until the expiry ages of 65, 75 or 80 (last birthday).

Premium payment terms are adaptable, with options of 5, 10, 15, 20, 25, or 30 years. Alternatively, you can choose to pay until age 64 (last birthday).

Promotion: For plans with a minimum premium payment term of 10 years, receive up to $350 in FairPrice vouchers. Enjoy $50 in FairPrice vouchers for a minimum annual premium of $1,000, $150 for a minimum annual premium of $1,800, or $350 for an annual premium of $3,000 or more. This promotion ends on 31 May 2026.

FWD Life Protection

The base coverage is on death, terminal illness, and TPD. You also have the option to include CI and ECI riders.

The plan allows you to multiply your coverage by 2x, 3x, or 5x. You can also select a minimum protection level age of either 75 or 85 years.

Premium payment terms are flexible, with limited-pay options of 5, 10, 15, 20, or 25 years.

A notable feature of this plan is the gradual reduction of the coverage amount upon reaching the minimum protection level age. The coverage reduces by 10% annually for the next five years and then remains level for the rest of the policy term. This gradual reduction also applies to eligible riders such as CI and ECI.

Whole Life Insurance Premiums

The following tables show quotes for a male and female, each with a date of birth of 01/01/1997 (age 30 at their next birthday). Both are non-smokers, work in non-high-risk occupations, and have no pre-existing medical conditions. The premium term is 25 years.

Basic Sum Assured of $100,000 for Death & TPD

| Insurer and Plan Name | Total Death Cover (Basic + Enhanced) | Multiplier Selected | Enhanced Cover Expiry Age | Annual Premium (Male) | Annual Premium (Female) |

|---|---|---|---|---|---|

| Singlife Whole Life Choice | $300,000 | 200% | 75 | $2,155.00 | $1,978.00 |

| HSBC Life – Life Treasure III | $350,000 | 3.5 times | 80 | $2,649.00 | $2,271.00 |

| Manulife LifeReady Plus II | $300,000 | 3 | 80 | $2,335.49 | $2,225.06 |

| AIA Guaranteed Protect Plus IV | $300,000 | 3x | 75 | $2,240.00 | $2,020.00 |

| Income Insurance Complete Life Secure | $300,000 | 300% | 75 | $1,808.70 | $1,770.30 |

| FWD Life Protection | $300,000 | 3x | 75 | $1,963.00 | $1,812.00 |

Basic Sum Assured of $100,000 for Death & TPD, and $50,000 for Early CI

| Insurer and Plan Name | Total Death Cover (Basic + Enhanced) | Multiplier Selected | Enhanced Cover Expiry Age | Annual Premium (Male) | Annual Premium (Female) |

|---|---|---|---|---|---|

| Singlife Whole Life Choice | $300,000 | 200% | 75 | $3,206.00 | $3,113.00 |

| HSBC Life – Life Treasure III | $350,000 | 3.5 times | 80 | $3,711.25 | $3,431.25 |

| Manulife LifeReady Plus II | $300,000 | 3 | 80 | $3,265.32 | $3,257.35 |

| AIA Guaranteed Protect Plus IV | $300,000 | 3x | 75 | $3,335.00 | $3,360.00 |

| Income Insurance Complete Life Secure | $300,000 | 300% | 75 | $3,233.05 | $3,364.85 |

| FWD Life Protection | $300,000 | 3x | 75 | $2,750.30 | $2,650.90 |

Notes and Disclaimers:

- The quotes are accurate as of 13 January 2026.

- Insurers have varying standards for determining age (using either age at next birthday or age at last birthday), which may result in policy terms deviating by one or two years.

- Do note that we try to compare fairly; however, because the plans may be structured differently (e.g., not having the same enhanced cover expiry age, a gradual reduction in the sum assured, or differences in how the multipliers work), it may be difficult to compare them side by side.

- The table is intended as a cost indication only and should not be regarded as financial advice, as it does not take into account your personal financial situation or objectives. Additionally, there are other policy aspects, such as cash values not shown here, which may influence your decision.

- Although the table may suggest that a particular plan is cheaper, this may not hold true for everyone, as individual profiles and needs differ. Likewise, while one plan may appear less competitive in price, it could offer more attractive benefits in other areas.

- While we strive to ensure the highest accuracy of information, we cannot be held responsible or liable for any errors, omissions, or inaccuracies.

- The figures provided are indicative only and may not reflect the actual cost. For up-to-date quotes, you should consult a licensed financial consultant.

We Compare 19 Insurance Companies to Find the Best Whole Life Insurance Plan for Your Needs

Our Trusted Providers

- AIA

- Allianz

- China Life

- China Taiping

- Etiqa

- Friends Provident

- FWD

- HSBC Life

- Income Insurance

- Life Insurance Corporation

- Manulife

- Monument International

- Raffles Health

- Singlife

- Sun Life

- Swiss Life

- Tokio Marine

- Transamerica

- Utmost International

Frequently Asked Questions

- What is a whole life insurance plan in Singapore?

It is a policy that pays out in the event of death, total and permanent disability, or critical illness. The coverage typically lasts for life. Over time, it accumulates cash/surrender value. - Is whole life insurance better than term insurance?

Both plans have their pros and cons. Whether a whole life insurance is suitable to you depends on several factors, such as your budget, preferences, and the coverage amount you require. - Is this service free?

Yes, there’s no fee involved. - How long does the appointment take?

It typically takes around 45 minutes. However, it can be longer for more complex situations or if you have further questions. - Are there any obligations?

Depending on your situation, we may or may not recommend solutions. If we do, it’s entirely up to you to go ahead with it. As consumers ourselves, we dislike high-pressure tactics. - Should I bring my existing policies?

Yes! If you do have them, do bring them along (or a policy summary) as we can provide more accurate feedback. - How is this appointment conducted?

This can be done over a zoom video call or a meet-up.