Here’s the term vs whole life debate in one line: the same $1,000,000 of cover costs you $567.45 a year as a term plan, or $4,356 a year as whole life.

That’s a gap of 7.7 times. What you get (or don’t get) for the extra money is what this whole debate is really about.

Feature lists only tell you so much. So we got real quotes, on the same day in July 2026, for the same person.

Here are the actual numbers.

Key Takeaways

- Term life insurance covers you for a fixed period (say, until age 65) and pays nothing back if you outlive it. Whole life insurance covers you for life and builds a cash value you can surrender for money, but it costs far more for the same amount of cover.

- For $1,000,000 of death, terminal illness, and TPD cover to age 65, a 30-year-old male non-smoker pays $567.45 a year for term and $4,356 a year for whole life. That’s 7.7 times more.

- Surrendering the whole life plan at 65 returns $104,400 guaranteed, or up to $183,809 including non-guaranteed bonuses illustrated at 4.25% p.a., against $108,900 of premiums paid.

- The right choice depends on whether lifelong cover and a cash value are worth an extra $3,789 a year to you. Neither answer is wrong. This article shows you exactly what the extra money buys, so you can decide with numbers rather than adjectives.

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

What Term and Whole Life Insurance Are (Briefly)

Both plans do the same core job: they pay out a lump sum if death, terminal illness, or total and permanent disability (TPD) happens, so that your income is replaced for your loved ones.

The difference is in how long they cover you, and what happens to your money along the way.

Not sure how much cover you need in the first place? Our life insurance calculator gives you an estimate in a few minutes.

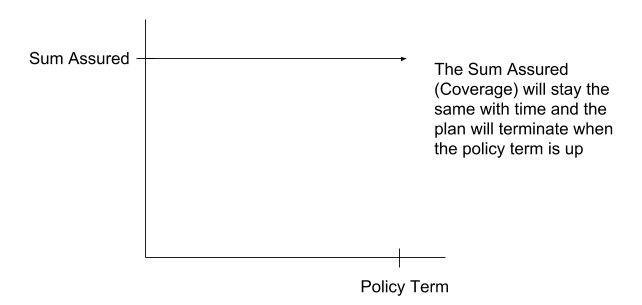

Term: pure protection for a fixed period

A term plan covers you for a period you choose, commonly until age 65.

Most of the premium you pay goes towards protection. When the term ends, the cover ends, and you get nothing back. That’s not a flaw. It’s the design, and it’s why term cover is so affordable per dollar of protection.

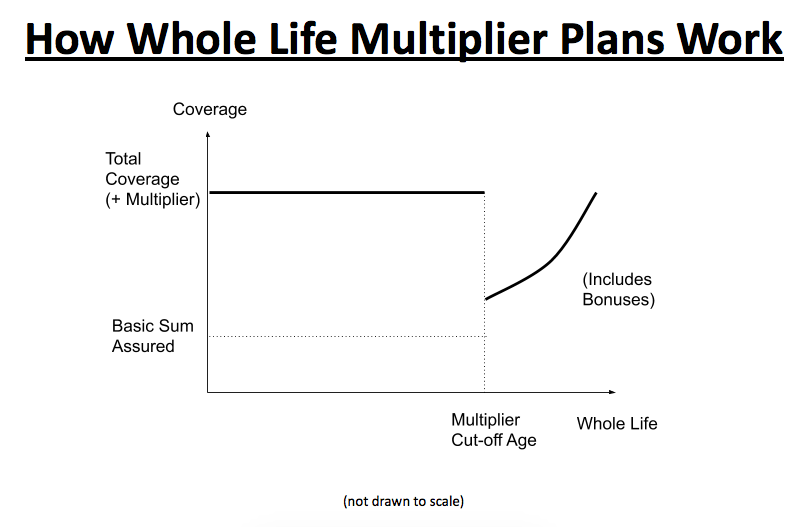

Whole life: protection plus cash value, with a multiplier

A whole life plan covers you for life, usually up to age 99 or 100, and builds a cash value you can surrender for money.

Modern whole life plans are sold with a multiplier. You buy a base cover (say $200,000), and an additional cover boosts your protection to a multiple of that (say five times, or $1,000,000) during your working years. After the multiplier period, the cover reverts to the base amount plus any accumulated bonuses.

Whole life plans come in participating, non-participating, and investment-linked forms. This article covers participating policies only, as they’re what most Singaporeans are offered.

The Real Numbers: $1,000,000 of Cover, Priced Both Ways

To make this a true like-for-like comparison, we quoted both plans, for the same person (male, 30 years old, non-smoker), with the same $1,000,000 of death, terminal illness, and TPD cover to age 65, on the same day in July 2026.

One thing to be clear about upfront: both quotes cover death, terminal illness, and TPD only, the basic protection. Critical illness and early CI cover can be just as important in a complete plan, but they’re deliberately left out here, because the point is to isolate the price difference between the two plan structures.

This is what came back:

| Term plan | Whole life plan | |

|---|---|---|

| Cover to age 65 | $1,000,000 | $1,000,000 ($200,000 base, boosted by a multiplier) |

| What’s covered | Death, terminal illness, TPD | Death, terminal illness, TPD |

| Annual premium | $567.45 | $4,356 |

| Premium paying term | 35 years (to age 65) | 25 years |

| Total premiums paid | $19,861 | $108,900 |

| Cover after 65 | Nil | $200,000 base + accumulated bonuses, for life |

| Cash value if you stop | Nil | Surrender value |

Source: quotes from a Singapore insurer, July 2026. Male, 30, non-smoker. Totals rounded to the nearest dollar. Full details in the methodology section below.

The premium gap is 7.7 times

In SmartWealth’s comparison, for the same $1,000,000 of death, terminal illness, and TPD cover to age 65, a 30-year-old male non-smoker pays $567.45 a year for term and $4,356 a year for whole life, a gap of 7.7 times.

Add it up over the life of each policy and the whole life plan costs $108,900 in total premiums against the term plan’s $19,861. That’s about 5.5 times more in absolute dollars, even though the whole life plan stops collecting premiums 10 years earlier.

A few things to note. Premiums rise with your entry age, so a 40-year-old will pay noticeably more for both plans. Female rates will also differ. Perpetual discounts, which the insurer applies for the entire premium term, are also factored in. And every application is subject to underwriting and health disclosure, so your own quote may differ.

What happens at 65 is the real difference

At age 65, the term plan simply ends. No payout, no refund, nothing. You’ve paid $19,861 for 35 years of protection, and that protection did its job.

The whole life plan carries on. The $200,000 base cover, plus accumulated bonuses that build up over time, continues for life. Some insurers also offer a multiplier that boosts your cover in the working years and steps it back down later, as with the $1,000,000 in this example. Whether your plan does this depends on the insurer and the option you pick.

So the honest framing isn’t “whole life covers you for life at $1,000,000”. It’s “whole life covers you at $1,000,000 during your working years, then at $200,000 plus bonuses for life”.

Is that worth nearly eight times the premium? That depends on the next section: what the plan hands back if you cash out.

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

What the Whole Life Plan Is Worth If You Cash Out

The surrender values below come from the plan’s benefit illustration, the document you receive with any whole life quote.

By age 65, our 30-year-old would have paid $108,900 in total premiums for the whole life plan. Here’s what surrendering it would return:

| Age at surrender | Guaranteed | Total at 3.00% p.a. | Total at 4.25% p.a. |

|---|---|---|---|

| 65 | $104,400 | $120,239 | $183,809 |

| 85 | $162,200 | $200,781 | $387,107 |

Source: figures from a Singapore insurer, July 2026. The totals are the guaranteed value plus non-guaranteed bonuses, illustrated at the two investment return scenarios required by LIA.

Surrender at 65 and the guaranteed value is $104,400, slightly less than the $108,900 paid in premiums. Add the non-guaranteed bonuses and the total illustrated value is $120,239 at the 3.00% scenario and $183,809 at 4.25%.

Hold until 85 and the guaranteed value alone reaches $162,200, more than total premiums paid. The total illustrated values are $200,781 and $387,107 at the two scenarios.

One thing these figures don’t show: the death benefit is often higher than the surrender value. Surrender and you take the cash value in the table. Keep the plan and it pays the $200,000 base cover plus accumulated bonuses when you die, which after 65 tends to run substantially above what you’d get by cashing out at the same age. So surrendering means giving up the larger payout for the smaller lump sum now.

Three caveats matter here. Bonuses are not guaranteed. The 3.00% and 4.25% figures are not predictions but illustration caps set by the industry, and actual participating fund performance may come in higher or lower. Also, surrendering ends the cover. You can’t surrender at 85 and still leave a payout behind.

Buy term, invest the rest

The classic argument against whole life is “buy term, invest the rest”. Let’s test it with our actual numbers.

The premium gap is $3,789 a year. Suppose our 30-year-old buys the term plan, invests that gap every year for 25 years (matching the whole life plan’s premium term), then lets the pot pay his remaining term premiums and grow. At an assumed 3% a year net return, here is how the invested pot compares against the whole life plan’s surrender value:

| At age | Invested pot (3% net) | Whole life surrender value |

|---|---|---|

| 65 | ~$179,000 | $104,400 to $183,809 |

| 85 | ~$324,000 | $162,200 to $387,107 |

On the same 3% return, the invested pot comes out ahead of the whole life plan’s cash value at both 65 and 85. What whole life gives you instead is a guaranteed floor the pot can’t match.

Here’s how the pot gets there, in three phases. From 30 to 54 (25 years), he pays in $3,789 at the end of each year, matching the whole life plan’s premium term. That’s $94,725 paid in over the 25 years. With each year’s $3,789 compounding annually at 3%, the pot reaches about $138,000 by 55. From 55 to 64, the whole life plan is paid up but the term cover still runs, so the pot itself covers the $567.45 term premium each year, growing more slowly to roughly $179,000 at 65. From 65 onwards the term cover has ended, so nothing goes in or out and the pot simply compounds, reaching about $324,000 by 85.

| Phase | Ages | What happens | Pot at end |

|---|---|---|---|

| Building | 30 to 54 | Invest $3,789 a year (total $94,725 paid in) | ~$138,000 |

| Coasting | 55 to 64 | Pot pays the $567.45 term premium each year | ~$179,000 |

| Compounding | 65 to 84 | No money in or out, pot just grows | ~$324,000 |

All figures assume a 3% net annual return; a higher or lower return would move the pot up or down accordingly.

But the maths leaves a few things out. It assumes you actually invest that $3,789 every year for 25 years, through every market crash, without skipping a year or raiding the pot for a renovation. Real returns don’t arrive in a tidy 3% line either, and an investment portfolio has no floor, so unlike the whole life plan’s guaranteed surrender value, it can drop below what you put in. There’s also the death benefit to remember: the whole life plan still pays out $200,000 plus bonuses after 65, and Singapore’s life insurers settle the vast majority of claims they receive, whereas the term-and-invest route leaves your family relying on the pot alone. And for a lot of people, the plain discipline of a premium notice landing each year is what makes the saving happen at all.

In my opinion, the numbers favour “buy term, invest the rest” for a disciplined investor, but discipline is precisely the part no illustration can guarantee. These projections are assumptions, not certainties.

The Differences at a Glance

The full comparison in one table:

| Aspect | Term | Whole life |

|---|---|---|

| Purpose | Pure protection | Protection plus a savings element |

| Sum assured | High cover is affordable, $1,000,000 is common | Lower base cover, boosted by a multiplier during working years |

| Claim payout | The sum assured | Base cover plus bonuses, or the boosted cover, whichever is higher |

| Cash value | None | Guaranteed plus non-guaranteed surrender value |

| Coverage period | Fixed: 20 or 30 years, to 65, or longer | Whole of life, usually to 99 or 100 |

| Premiums | Low | Several times higher for the same cover |

| Premium paying term | Usually the full policy term | Limited pay, commonly 20 or 25 years |

| Complexity | Simple, everything is spelt out | Non-guaranteed bonuses make outcomes harder to predict |

| Flexibility | Easy to drop or replace (subject to health) | A long commitment, surrendering early often loses money |

Three of these rows deserve one extra line each.

Coverage period: term doesn’t have to end at 65. Some plans stretch term cover to age 99, which narrows the gap between the two plan types, at a higher premium.

Riders: both term and whole life plans can add critical illness riders, which changes the price entirely. If CI cover is your real concern, compare early critical illness plans on their own merits rather than bundling by default.

Premium term: limited pay sounds attractive because premiums stop at retirement, but you’re simply paying more per year for fewer years. The comparison table above already reflects this.

How Should You Decide?

There’s no single right answer, but there’s usually a right answer for your situation. Here are the three most common ones.

If your budget is tight and your cover need is large

Go with term. Being underinsured during the years your family depends on your income is a bigger risk than going without lifelong cover, and term is usually the only affordable way to get $1,000,000 or more of cover on a modest budget. Our comparison of the best term life insurance plans in Singapore is the natural next step.

If you want cover or cash value beyond 65

Whole life earns its place here. The base cover plus bonuses continues for life, and as the surrender values showed, holding to 85 builds meaningful guaranteed value. Just go in with accurate expectations: you’re paying a large multiple of the term premium, and the $1,000,000 protection tapers to the base after your mid-60s. If that trade-off suits you, compare the best whole life insurance plans before committing.

If you want both

It doesn’t have to be either-or. A common structure is a large term plan covering your main earning years to 65, paired with a smaller whole life core that continues beyond. You get adequate cover now and a lifelong base later, without paying whole life premiums on the full $1,000,000.

Whichever direction you lean, your circumstances are what decide it: dependants, liabilities, health, and budget. Applications are subject to underwriting and health disclosure, and this article is informational rather than a recommendation for any specific plan.

In Closing

The term vs whole life debate is usually argued with adjectives. “Term is throwing money away.” “Whole life is a rip-off.”

The numbers say something more useful. For the same $1,000,000 of cover, term costs a fraction of the price and ends with nothing. Whole life costs 7.7 times more, hands back a surrender value that may exceed what you paid, and keeps a smaller cover running for life. Both answers are defensible, depending on what you’re buying insurance for.

Start with how much cover your family actually needs. Once that amount is clear, the right plan type usually becomes obvious, and it’s easier to see where this one decision sits in the wider protection picture. And if you’d rather work through it with a licensed consultant, our FullCircle planning session looks at your protection needs alongside the rest of your finances.

Methodology

Both quotes were generated on the same day in July 2026, from the same Singapore insurer, for the same profile: male, 30 years old, non-smoker, standard terms.

The term quote is a level term plan with $1,000,000 of cover for death, terminal illness, and TPD, covering to age 65 with premiums payable throughout. The whole life quote is a participating whole life plan with a $200,000 base cover boosted by a multiplier to $1,000,000 until age 65, covering the same three events, with premiums payable over 25 years. Neither quote includes critical illness or early CI riders, which would change the premiums substantially. Those covers matter in their own right, but this comparison isolates the basic life cover so the two plan structures can be priced side by side.

Annual premiums are as quoted, including the insurer’s prevailing discounts. Surrender values are taken from the whole life plan’s benefit illustration at the two investment return scenarios life insurers are required to show, currently capped at 4.25% and 3.00% a year under LIA guidelines in force since July 2021.

These figures are from one insurer and one profile. They illustrate the structural gap between the two plan types, not a market survey of every insurer’s pricing (our comparison pages handle that). The “buy term, invest the rest” projection assumes the annual premium gap is invested at the stated returns net of fees, with no missed contributions. Past performance and projections don’t guarantee future outcomes.

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.