Raising a child in Singapore can be a costly affair.

Among the many costs involved (child delivery, childcare, living expenses, and more), the biggest ticket item of all is their university education.

Helping to fund this final stage of their education journey, before they become a (real) adult, is one of the last big financial commitments we make as parents.

Singapore is a competitive place. Every edge you can give your child increases their likelihood of succeeding in the future.

Setting up an education fund for your children means that when it’s time for them to enter university, the money is there if they need it.

One popular way to fund an education is a child education endowment plan.

Today, we’ll take a look at what it is and how to weigh it against your other options.

How Much Will Your Child’s University Education Cost?

The very first step of saving for an education fund is to know where you want to send your kids for further studies.

Do you intend to send your child to a local or an overseas university?

Knowing that will tell you roughly how much you need to save.

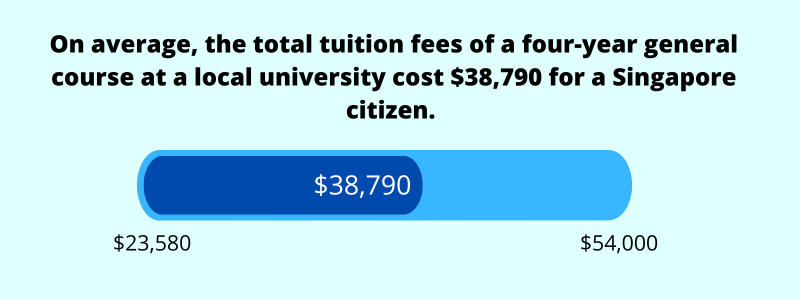

To give you an idea, you can expect to fork out around $38,790 in tuition fees for a degree at a local (public) university such as NUS or NTU, based on 2026 fees for Singapore citizens.

Although it seems expensive, a good proportion of people still view it as worth it.

For an overseas university, it’ll cost more. You can learn more about the costs of overseas studies.

But tuition fees are not the only costs to save for. There are still living expenses.

Annual living costs for a student in Singapore are estimated at $10,775 as of 2026, or about $43,100 over four years.

That brings the estimated cost of obtaining a local degree to around $81,890.

However, that’s in today’s prices. When we factor in the average inflation for tuition fees and the average general inflation, future costs will be much higher. If you’re not sure how much it’ll all cost, simply use our university education fund calculator.

There are a variety of ways to fund a university education. Saving and investing early is one of the most reliable.

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

It’s Almost Always Better to Start Saving Early

Unless you’re living from payday to payday or you have bad spending habits, you’re likely to have a healthy surplus of savings every month. If not, do check out how to budget efficiently and control your expenses.

By using our education fund calculator, you can see what your shortfall is and how much you’ll need to have at a certain age. The time horizon is fixed, so the goalposts don’t shift.

The more you delay saving or investing, the harder hitting your goals will be.

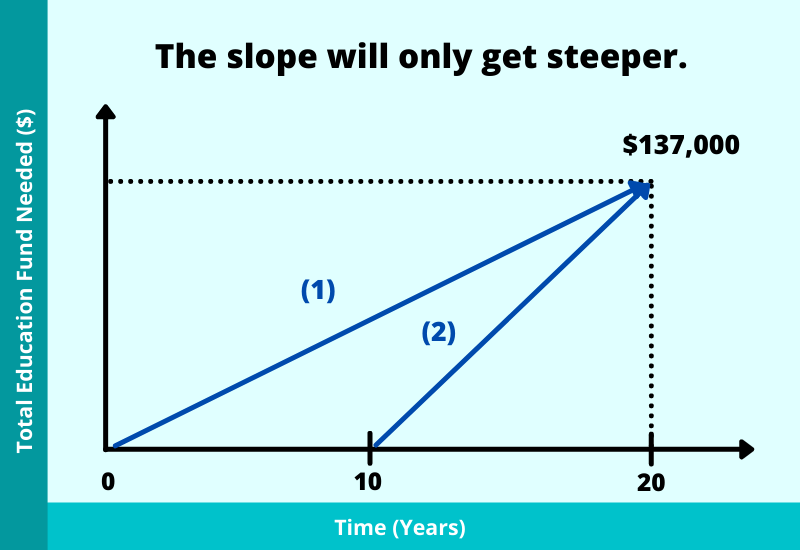

Here’s an illustration, assuming you need to save a total of $137,000 in 20 years’ time:

When you start earlier, the monthly commitment is smaller and more digestible. When you start later, there is much less time to accumulate, so your monthly commitment must increase in order to hit the target. The slope only gets steeper.

If your child is eligible to receive bursaries or scholarships in the future, these funds can still be used for other purposes, such as paying for their wedding, partially funding their first home, or supplementing your retirement.

Investing to get more out of your dollar allows you to set aside an even smaller monthly commitment while still being able to hit your end goals.

One such option is the child education endowment plan.

What Is a Child Education Savings Plan (& How Does It Work)?

To put it simply, a child education plan is an insurance product that aims to provide funds for your child’s university education by a specified time.

There are many variations of savings plans. Some plans are education-specific and pay out a stream of money over a few years, while others are simpler and pay out a lump sum after a fixed period of time.

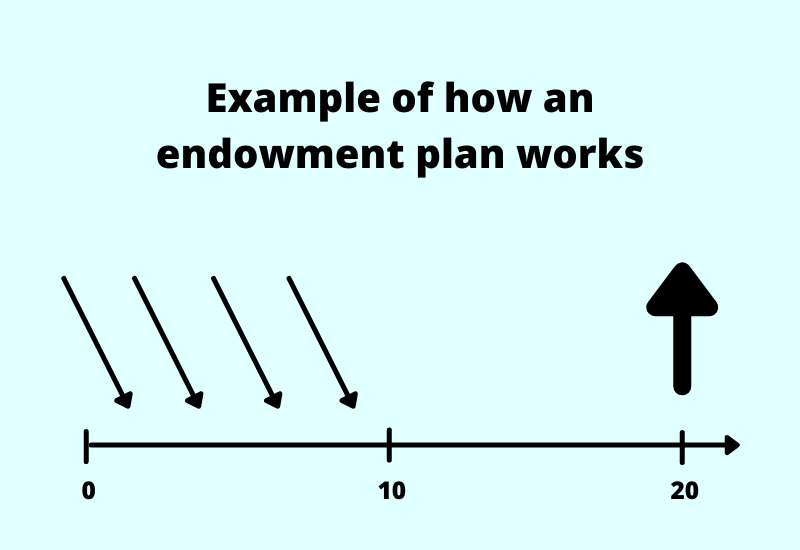

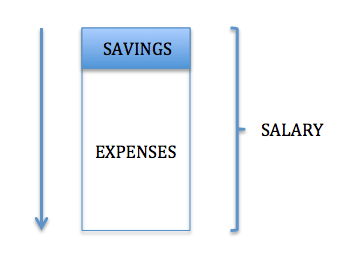

To fund the plan, you’ll have to commit to a regular premium (the amount you’re “saving”) for a specific number of years.

In summary, here’s a simple illustration of how an endowment works:

Such savings plans are often capital guaranteed upon maturity, and provide both guaranteed and non-guaranteed returns.

Below, we’ll look at the education savings plan in greater detail.

5 Reasons to Build an Education Fund With an Endowment Plan

There’s no lack of financial products to help you save and invest. All of them have their pros and cons.

So, here are five reasons why an endowment plan is useful for building an education fund.

1) It enforces discipline

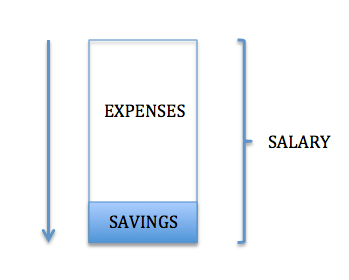

Without the correct spending and saving habits, we tend to spend first, then save whatever is left.

Because of emotional spending, we may buy things that we don’t need, leading to overspending.

The proper way to save, in my opinion, is to save first and then spend later.

We can do this by transferring the amount we intend to save into another bank account when our monthly income comes in. This account should be made inaccessible so we don’t withdraw money from it whenever we feel like it.

Endowment plans embody this concept. Money is transferred via GIRO from your savings account on a regular basis, ensuring that you’re always contributing to your goals.

2) It provides guarantees

Most education savings plans are capital guaranteed upon maturity.

This is important because you don’t want to be caught in a situation where you get back less than what you’ve put in (which can happen with investments).

You’ll know that the money will be there when it’s time for your child to enter university.

3) It also provides potentially higher returns

Investing in stocks and shares can give you the highest potential gains.

If you know what you’re doing, you can DIY. If not, you can always transfer that function to a financial adviser.

Having said that, investments come with a higher degree of risk in the form of volatility (where the value can fluctuate) and a potential loss of principal (you get back less than what you’ve invested).

Furthermore, as your time horizon is fixed (the child’s university entry age doesn’t typically change), timing matters a great deal. If it’s time for your child to enter university and your investments aren’t performing well, what will you do? Will you be willing to cash out at a loss? If you want to wait for your investments to recover, can you wait for an extended period? What if they never recover?

Depending on various factors, you can expect the total illustrated yield from a savings plan to be about 2% to 3% per year. The expected return (which is made up of guarantees and non-guarantees) isn’t fantastic, but it doesn’t need to be.

That’s likely to be higher than leaving the money in a regular bank account or fixed deposit.

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

4) It is flexible and can suit your specific needs

Everyone’s situation is unique.

Your specific needs, such as your time horizon, monthly savings amount, and premium term, will differ from someone else’s.

Fortunately, there’s always something for everyone. Plans can be tweaked.

5) Your child’s education fund can still be provided for, rain or shine

The main objective of an endowment plan is simply to save (and enhance your savings), so that it can be used to pay for school fees in the future.

But it doesn’t end there. Unfortunate events such as death could happen, and when they do, there might not be funds coming in anymore to support the premiums.

This is why such plans come with riders: to pay out the sum assured (or the cost of education) if death, disability, or critical illness happens.

Collectively, they provide greater assurance and peace of mind.

The Main Downside of Endowment Plans

The picture isn’t entirely rosy.

Once you’ve decided on the premium amount, premium term, and policy term, the endowment plan becomes rigid. It might not provide you with any liquidity if you need money along the way.

If you decide to stop paying the premiums or cash out early (surrender), what you get back may be less than what you’ve put in.

But in exchange for this long-term commitment from you, insurance companies can take away the risk of capital loss at maturity while still providing some upside.

This rigidity also ensures that you keep saving. Any lapse means your child’s fund may fall short.

3 Things Parents Should Also Take Note Of

I know, saving and investing are important. But there are equally (or more) important aspects you should be aware of.

Here are some of them:

1) Having emergency funds

First and foremost, having an emergency fund, money set aside and rarely touched, is always a good financial habit.

If a retrenchment or a sudden drop in income happens, these funds can help you cover living expenses until the situation improves.

You can set aside six to 12 months of expenses.

This safety net shouldn’t be drawn on as and when you like. It should only be used in dire situations.

2) Having adequate healthcare coverage

The cost of healthcare keeps rising. Singapore’s medical inflation rate was estimated at 15.5% in 2025, and this trend is likely to continue.

One way to protect yourself from increasing healthcare costs is to have adequate hospitalisation coverage, which is the foundation of a proper financial plan. Coverage for both parents and children is essential. Without it, medical bills will eat into your hard-earned savings, and huge bills can drive you into debt.

3) Protecting the income of both parents

As the monthly cost of living has increased over the decades, a dual-income family has become the norm.

Expenses (and savings) come from the income you earn. Without it, daily living can’t function.

Therefore, it’s vital to protect your income.

While retrenchments can happen (which is why you should have an emergency fund), unfortunate events such as death, disability, or critical illness will cripple your ability to earn an income.

Who’s going to pay for the daily expenses as well as provide for long-term goals then?

With sufficient life insurance, your family will not be burdened by financial woes.

For most parents, term life insurance is an affordable way to get enough cover during the child-raising years, while some prefer whole life insurance for protection that continues beyond them.

Other than these three things, there are other factors to take into account too.

Is a Child Education Savings Plan Right for Your Family?

A child education savings plan gives you certainty, and it forces you to save. What it won’t give you is the highest possible return.

It’s also just one option. Cash savings, investments, government schemes, and loans can all play a part, and most families end up using a combination.

Which combination? That depends on how old your child is, how stable your income is, and what other goals are competing for the same dollar. Your insurance coverage and your own retirement matter here too, and in my opinion, retirement should never be the trade-off.

This is why we prefer to look at an education fund as part of a complete financial plan, not as a product decision on its own.

If you’d like help thinking it through, find out more about our FullCircle comprehensive financial planning today.

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.