Why do some of us find it hard to save money?

Is it because of our saving and spending habits? It can very well be.

We must exert control over them and not let them control us.

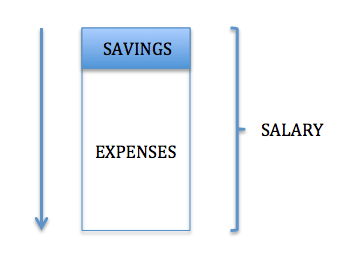

One way is to build a budgeting plan to manage your personal finances. It takes into consideration your monthly income, amount of savings/investments you intend to set aside and expenses – necessities and wants.

While it may seem like a chore (which it isn’t), its usefulness will go a long way.

Doing this will ensure you can save more and spend less.

So, let’s find out how to budget money effectively!

To help you budget better, you can use our free online budget and expenses calculator. If you prefer to use an excel spreadsheet for this, check out our template, FinSnap. It’s also free.

Too Long; Didn’t Read (Infographic)

This infographic just gives you a simple overview. There are more details that you need to know, so it’d be great to read further.

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

What Is a Budget

A budget (personal) is a plan to specify how your income should be allocated to savings and expenses for a given period, usually monthly.

The process of budgeting consists of tracking and reviewing these figures so that you can create a budget to stick to.

Although it seems like a daunting task, budgeting is one of the core components to proper financial planning, and shouldn’t be neglected as what can be measured can be improved.

3 Reasons Why Budgeting Is Important

When you sit down and relook into your personal finance matters, you’ll inevitably have to list down your net worth (assets and liabilities) together with your cash flow (income and expenses).

It’s not enough to just get a rough estimate – it needs to be broken down further.

Doing this will give you a very accurate assessment of your financial health. Unfortunately, many people skip this step.

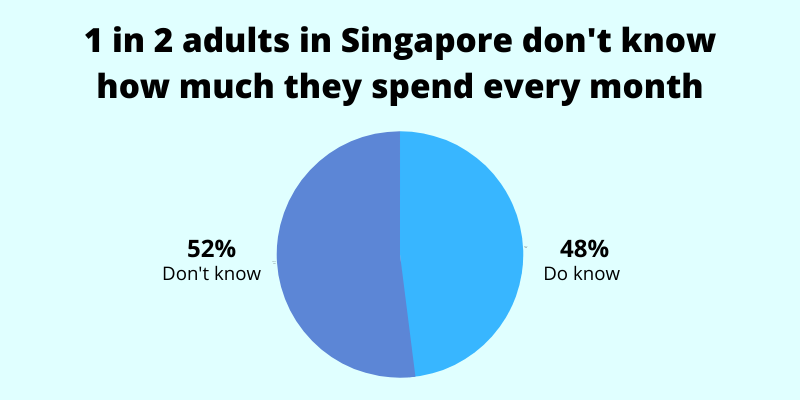

In fact, from a survey we’ve done on spending habits of Singaporeans, we’ve found out that one in two adults in Singapore don’t know how much they spend every month.

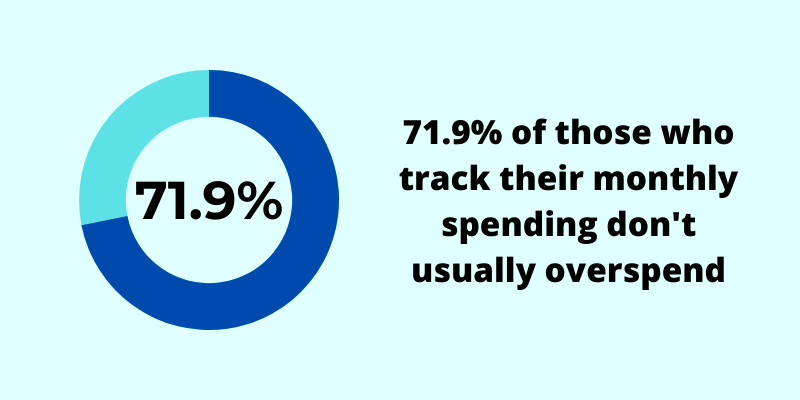

From that same survey, we’ve also found that 71.9% of those who do track their expenses don’t usually overspend.

Therefore, only when you have your figures on hand will you be able to perform proper budgeting.

Here are 3 reasons why budgeting is important:

1) Make better use of your money

The pre-requisite to budgeting is to track your expenses.

Tracking allows you to see where your money is going and gives you a lot more insights such as:

- Are you spending on necessities or wants?

- Are you overspending because of wants or are your needs too high?

- Are there items that you can reduce?

- and many more

Managing your expenses effectively will increase your savings at the end of the month.

2) It enforces discipline

Most of us are not taught the proper to save – schools don’t teach that.

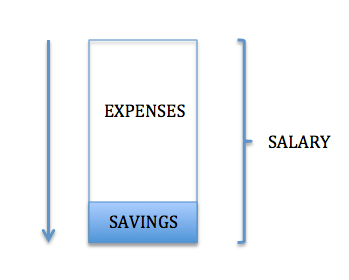

So we’ve been saving like this:

When income comes in, we tend to spend on whatever we want to (and whatever makes us happy), but at the end of the month, there isn’t much to show for.

That’s unlikely to be the right way to save.

One way you should be doing is the opposite:

When income comes in, we specify an amount to set aside as savings or investments. And only then, we’re allowed to spend the remainder.

And because the amount that’s allowed for expenses have been budgeted, if during the month you find yourself wanting to spend on an item that’s not in the budget, you’d know that you’re going to overspend.

This mental resistance together with the desire to save increase the chance of you to say “no” when such a situation like that comes up.

3) Achieve your long term financial goals

Hitting major financial goals requires not just time but commitment as well.

For example, if you plan to save for retirement, you must set aside a fixed sum regularly. Not doing so will only make the journey steeper and unattainable.

Therefore, a budgeting plan creates a structure for forced savings to happen.

Only when you take these small steps will your biggest financial goals can be achieved.

The Different Types of Budgeting Plans

Here are the main components in a budget:

- Income

- Savings or investments to set aside

- Expenses

- Necessities

- Wants

To make a budgeting plan, you’ll have to decide how much percentage of your monthly income will be allocated to these components.

To help you with this, here are some commonly used budgeting plans:

1) 50/30/20 rule

The 50/30/20 budgeting rule is to divide your take-home income into 3 categories:

- 50% for necessities

- 30% for wants

- 20% for savings or paying off liabilities

Sticking to such an allocation will allow you to know how your money should be spent.

As spending on necessities is important, a higher percentage of 50% is allocated to it.

Naturally, wants have a lower allocation of 30% so you will not overspend on comforts and under-save for the future.

With a 20% allocation for savings or paying off liabilities, you ensure that there will always be well-spent money.

It’d be better if you can reduce your necessities and wants so that you can save more.

2) 40/30/20/10 rule

The 40/30/20/10 strategy splits your income into 4 categories:

- 40% expenses

- 30% liabilities (mortgage repayment, rent, student loans, etc)

- 20% savings (short and long term)

- 10% insurance

By keeping your expenses lower than 40%, you’re able to put more into other areas.

With a 30% cap on liabilities, you’re limiting yourself to huge debts that can accumulate over time. This also means that you shouldn’t buy a bigger house that you can’t afford.

20% should be the minimum you’re saving. If you have excess from your expenses and liabilities, you can put more in here.

10% will be towards insurance. As insurance is a unique element, it’s not placed in the same category as expenses. This is because it becomes an asset when the undesirable happens allowing you to protect your future income and preserve the wealth you’ve accumulated.

3) Your own rule

Everyone is different.

You have your unique situation, financial commitments and future goals.

What works for someone else will not work for you.

Because of this, commonly used budgeting plans are at best just guidelines to follow.

You’d have to create your own rules by deciding a percentage you’re allocating for the main components:

- Savings/investments to set aside

- Necessities

- Wants

If you want comfort, allocate more into “wants”. If you want to have a high savings rate (e.g FIRE movement), allocate more into “savings to set aside”.

3 Tools to Help You Start Budgeting Your Money

If you want to start budgeting, one of the best ways is to use a tool.

Here are 3 types of budgeting tools:

1) Mobile app

The mobile app is a convenient way to key in daily expenses on the go. You can even sync with bank accounts to extract information.

Your progress is usually portrayed with fanciful charts and diagrams for easy data visualisation.

Entering daily expenses is great if you can commit to it. But in my opinion, it’s a hassle for me.

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

2) Calculator

A budget calculator can provide you with a list of important fields that can be auto-tabulated to give you an overview of your finances.

You just need to key in your expenses according to the fields provided. It’s simple and easy to use. Check out our free online budget calculator.

3) Excel spreadsheet/worksheet

The fields in a calculator are fixed and can’t be changed at all.

That’s why a budgeting excel spreadsheet can be useful if you wish to manipulate data.

If you want to add more expenses, you can do so easily. Furthermore, your data can be stored on the spreadsheet for further editing or reviewing in the future. For a free budgeting template, check out our FinSnap.

These budgeting tools help make your life easier. You can even use a note-taking app like Evernote. What’s important is to take note of your savings and expenses.

7-Step Budgeting Process to Save More Money

Here’s the 7-step process on how to budget money:

- Ensure your income is correctly reflected

- Decide on a budget allocation

- Create separate bank accounts

- List down your previous month’s expenses

- Review and improve on your numbers

- Repeat steps 4 and 5 every month

- Monitor your progress

And more details on each step..

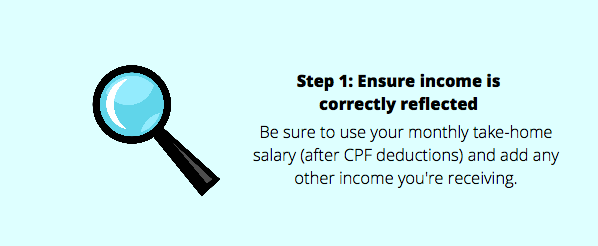

1) Ensure your income is correctly reflected

How much you can allocate to savings and expenses depend on how much you’re able to.

So the first step is to ensure you’re using your monthly take-home salary after CPF contributions and not your gross salary.

(Side note: learn how your CPF contributions affect retirement)

If you have any other income, be sure to include them in as well.

Examples of other income:

- Dividends

- Rental

- Businesses

- etc

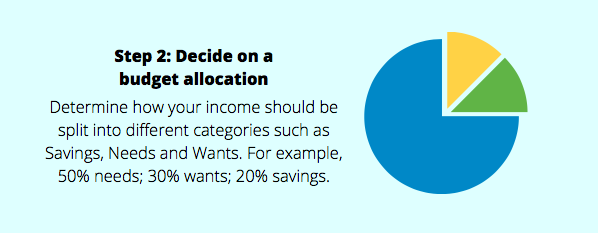

2) Decide on a budget allocation

The second step is to select a budgeting rule to follow.

Is it the 50/30/20, 40/30/20/10 or your own rule?

To make it simple, think about your situation and future goals you have, then allocate a percentage to these categories:

- Savings or investments to set aside

- Necessities

- Wants

This will then be the budget allocation you must follow when you receive your income.

(Sometimes, you need to get a feel of what expenses you’re currently incurring first. So, you can take a look at step 4.)

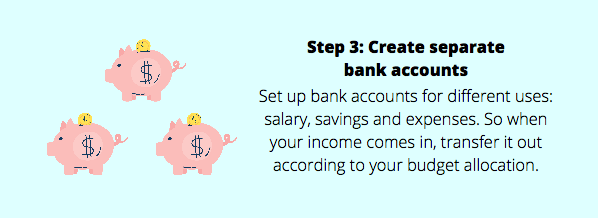

3) Create separate bank accounts

Even if you’ve created a budget plan, everything will be a mess if it’s all done in one bank account.

And that’s why it’s good to have multiple bank accounts for the different categories.

That way, when you receive your income, you can transfer to the other bank accounts according to the allocation.

While there are a few ways to do this, you can consider having 3 accounts:

A: Salary Account – all income will go into this

B: Savings Account – contains emergency funds, short term financial goals and money waiting to be invested

C: Spending Account – daily, monthly and annual expenses

So when you receive your income, you’ll transfer the amount you intend to save from A to B.

And the remaining amount (which is the amount you’ve budgeted for expenses) to be transferred to C.

You can also set up standing instructions with the bank to automate the transferring of funds.

Example: With a standing instruction in A, a fixed amount of money will be automatically transferred to B on a specific date every month.

Setting up standing instructions is incredibly easy and will streamline the process for you so that you can concentrate on other important tasks.

4) List down your previous month’s expenses

This step will take the most time as you’ll need to get more detailed figures.

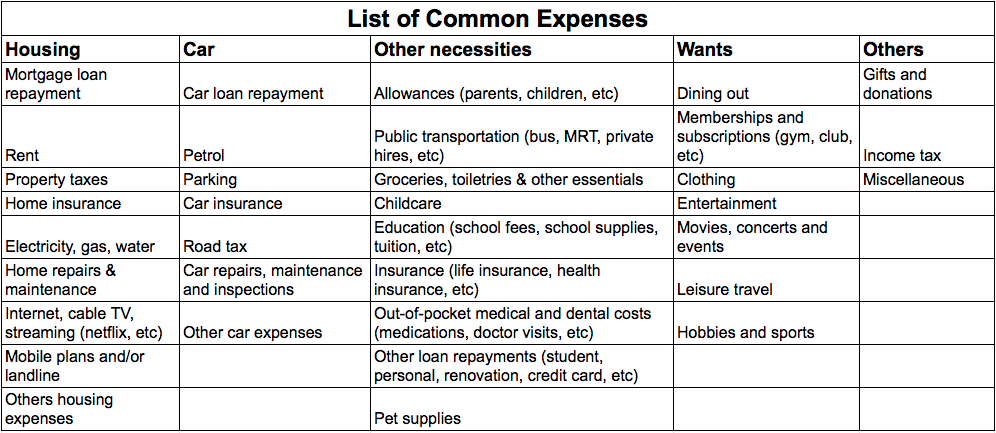

Most calculators and excel spreadsheets contain a list of common expenses, but here’s one if you need:

Personally, I don’t keep track of my daily (not monthly) spending as I find it a hassle to record these figures down even if I can use a mobile app.

But it’s still important to know what you’re spending on as accurately as possible.

So if you’re like me, here’s what you can do:

- try to use one card for all purchases (don’t need to get caught up with rebates and all)

- don’t use cash if possible

- if you use mostly cash for food, withdraw a fixed amount periodically say $400, and that’ll be under “food”.

To know what I’ve spent for that month, I just need to check my bank account statement which will capture the details of my expenses in one place (another reason for having separate bank accounts for different uses).

5) Review and improve on your numbers

How much you can save is totally dependent on how much you spend.

You spend less, you save more.

So when you have categorised your expenses into needs and wants, generally to save more, you’d want to reduce your wants.

But for each item, there are 3 decisions you can make to improve on it:

- Leave it

- Find a cheaper/better alternative

- Eliminate it

6) Repeat steps 4 and 5 every month

Once you’ve set up everything, it becomes a seamless process.

From here on out, you just need to track your expenses (which should all appear in a bank account statement), review the items and improve on them if necessary.

You just need to set some time – once a month. That’s all.

7) Monitor your progress

The end goal is to have more savings which will contribute to your future financial goals.

After some time, you may want to see how you’ve progressed.

This can be done by periodically calculating your total net worth (personal balance sheet).

Do you have more assets or lesser liabilities now? Are you closer to your financial goals?

Only when you know where you stand can you do something about it.

Other Aspects of Financial Planning

Having a budget plan helps you spend less and save more.

That’s just one aspect of financial planning. There are other areas too.

Firstly, one of the best investments you can make is in yourself, whether is it personal development, career and/or business. They’re likely to give the highest returns in the long run, which will bring more money in. And that will trickle down. So this area should be your main focus.

Secondly, as your income enables you to spend and save, it’s the most crucial financial resource you have. Once you lose it due to death, disabilities or critical illnesses, your financial situation will deteriorate drastically. One way to reduce this risk is to protect your future income with life insurance. Check whether you have sufficient life insurance coverage.

And lastly, if you stick to the budget, you’re likely to have more money saved. Aside from your emergency funds and short term goals, the excess savings sitting inside will be losing value due to inflation and the low-interest rate. So, ensure that you park this excess cash in alternatives that can give higher potential returns while still taking into account your risk tolerance.

What’s Next?

If this is your first time trying to budget money, don’t be overwhelmed.

It’s not as difficult as it seems and will get better with time.

Budgeting tools are available for you and they offer a huge convenience.

To start budgeting, check out our free resources – online budget and expenses calculator and a budgeting excel template, FinSnap.

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.