What will a degree cost by the time your newborn is ready for university?

A local degree that costs about $81,890 today, including living expenses, is on track to cost more than $130,000 in 20 years, when a baby born in 2026 would be at university. That’s because the cost of education in Singapore has outpaced general inflation for two decades.

The good news: with enough lead time, this is one of the most plannable goals in personal finance. You know roughly when the money is needed and roughly how much.

This guide walks you through the full numbers, from preschool to degree, and every major way to fund them.

Key Statistics Summary

- SmartWealth’s projections put the full education journey of a Singapore citizen child born in 2026, from infant care to a local university degree including living expenses, at around $170,000.

- In today’s dollars, that same journey costs about $120,840, of which $77,739 is fees and $43,100 is university living costs.

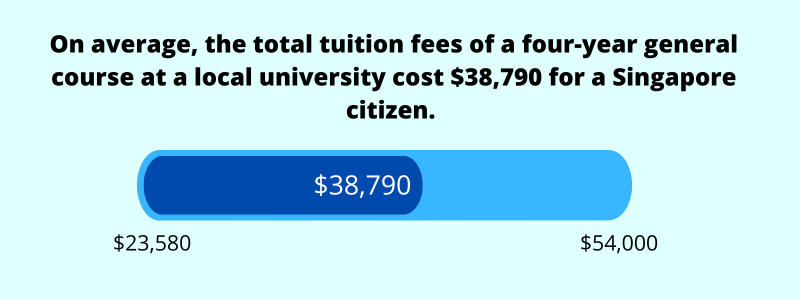

- The average cost of a four-year local university degree is $38,790 in tuition fees for Singapore citizens in 2026, or $81,890 once living expenses are included.

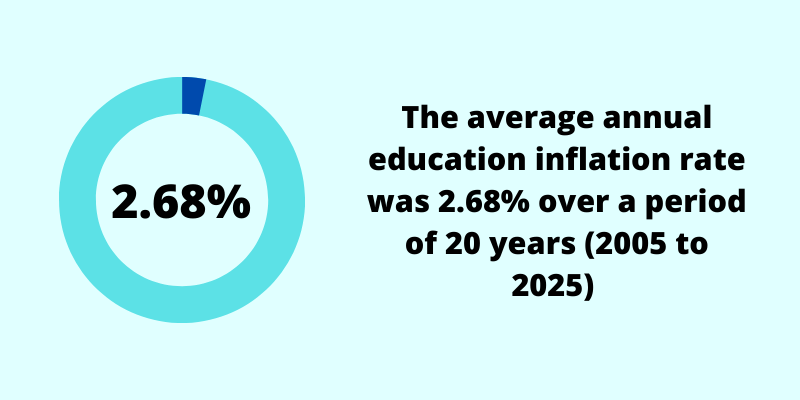

- Education costs in Singapore rose 69.6% from 2005 to 2025, an average education inflation rate of 2.68% per year, versus 2.14% for headline inflation.

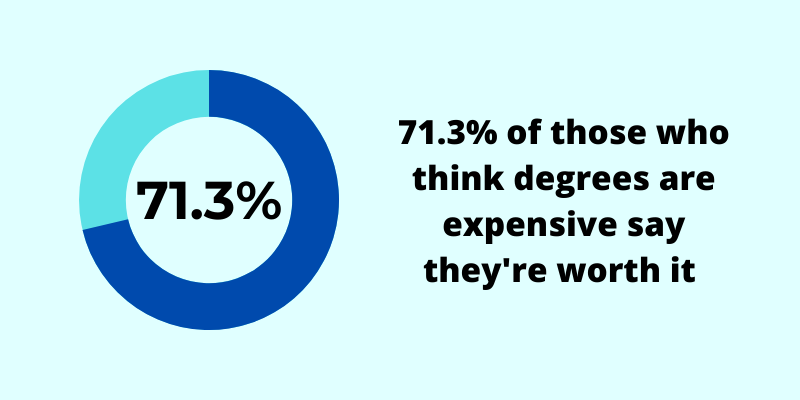

- 2 in 3 adults in Singapore say a university education is expensive, yet 71.3% of them still believe it’s worth the cost (SmartWealth survey).

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

What Does a Child’s Education Cost in Singapore? (Preschool to Degree)

For a Singapore citizen child attending government schools and a local university, the full journey costs about $77,739 in today’s dollars before living expenses, or roughly $120,840 once you add four years of university living costs. Here’s how that breaks down, stage by stage.

School fees from primary to JC

Formal schooling is the affordable part. Thanks to heavy government subsidies, a citizen child pays $13 a month in primary school, $25 in secondary school, and $33 at junior college. Over 12 years, that’s under $3,000 in total.

The expensive stages sit at either end: preschool and university.

| Stage | Duration | Estimated cost for a Singapore citizen |

|---|---|---|

| Infant care (after subsidies) | 16 months | $11,938 |

| Child care (after subsidies) | 66 months | $24,083 |

| Primary school | 6 years | $936 |

| Secondary school | 4 years | $1,200 |

| Junior college | 2 years | $792 |

| University (local, tuition only) | 4 years | $38,790 |

| Total | $77,739 |

Source: SmartWealth, school fees from primary to JC. Preschool figures assume a median-income household with a working mother at an ECDA-licensed centre.

Two caveats. These are today’s prices, not what you’ll actually pay over the next two decades. And permanent residents and international students pay many multiples of these figures, since the subsidies are tiered by citizenship.

Tuition and enrichment on top

The table above stops at school gates, but many Singaporean households don’t. Private tuition has become a near-standard part of the journey here, and what parents spend on tuition can rival the cost of the degree itself.

At 2026 one-to-one rates, a single subject taken weekly from Primary 1 to the O-levels comes to around $38,400, and families taking several subjects through the exam years can reach degree-level sums. Across all households, average spending on tuition was about $104.80 a month in 2023, and families here spent an estimated $1.8 billion on it that year, according to the latest Household Expenditure Survey.

Tuition is optional, and these figures are not included in any of the tables or totals in this guide. They are here to show the scale, so that if you intend to provide tuition, you budget for it deliberately rather than absorbing it month by month.

The total from preschool to degree

For a Singapore citizen child born in 2026, we estimate the full education journey will cost around $170,000, including four years of university living expenses.

No published local estimate combines every stage into one number, so we computed it ourselves. The logic is simple. Preschool and school fees start now and are paid at close to today’s prices, so we don’t inflate them. University is the one stage that sits 20 years away, so it’s the only figure we future-value.

| Component | When it’s paid | Estimated cost |

|---|---|---|

| Preschool to JC (today’s prices) | Over the next 18 years | $38,950 |

| University tuition (in 20 years) | Around 2046 | $65,832 |

| University living expenses (in 20 years) | Around 2046 | $65,826 |

| Total | $170,608 |

Source: SmartWealth calculations. Tuition is projected at our computed education inflation average of 2.68% per year, and living expenses at the 20-year headline inflation average of 2.14% (both 2005 to 2025).

If education inflation runs closer to 4% per year, a more conservative planning assumption, the total climbs to roughly $190,000.

These are projections, not promises. Actual costs will depend on inflation, subsidies, and the path your child takes. For the full data behind each stage, see our education cost statistics.

Education Inflation: The Reason to Start Early

Education costs in Singapore have grown faster than almost everything else you buy. From 2005 to 2025, the cost of education rose 69.6%, while the overall consumer price index rose 52.8%.

That works out to an education inflation average of 2.68% a year over the past 20 years. Over the same period, headline inflation averaged 2.14% and core inflation just 1.88%.

The gap looks small on paper. Compounded over the roughly 20 years between birth and university, it isn’t. A degree that cost $50,000 in 2005 would have cost around $84,800 by 2025 on education inflation alone.

One caution before you plug numbers into a spreadsheet: historical averages describe the past, not the future. Education inflation was just 0.7% in 2025, well below its long-run average, and future rates may be higher or lower. When we project for clients, we prefer to add a buffer and assume 4% rather than risk a shortfall.

The practical takeaway doesn’t change either way. Every year you delay, the target grows and you have less time to reach it.

The Big One: Planning for University

University is where child education planning gets serious. It’s the most expensive stage by far, it arrives at a fixed and predictable time, and unlike primary school, nobody subsidises it down to $13 a month.

Local university costs

Four years of tuition at a local autonomous university costs a Singapore citizen an average of $38,790 in 2026, after the MOE Tuition Grant. The range runs from $23,580 at SIT to $54,000 at SUTD.

Professional degrees cost considerably more. A law degree runs about $51,000 over four years, while medicine at NUS costs $166,000 over five.

Citizenship matters enormously here. A permanent resident pays an average of $61,900 for the same general degree, and a non-subsidised student pays around $162,200, more than four times the citizen rate.

Overseas: UK, US, and Australia

If your child is studying in the UK, US, or Australia, expect a bill several times larger. Our benchmark comparison, using an engineering degree at 2026/27 fees, puts the full total including living costs at roughly $257,000 in the UK, $325,000 in Australia, and $479,000 in the US.

Universities typically raise their fees each year, so treat those totals as a minimum. Even the affordable end of that range is roughly three times the cost of the local route, and the US figure is closer to six times.

Living expenses, at home and abroad

Tuition is only part of the university bill. A student at a local university spends an estimated $10,775 per year on hostel accommodation, food, transport, and personal expenses, or about $43,100 over four years.

Living at home cuts that substantially, since accommodation is the largest component. Without it, annual expenses drop to around $6,450.

Overseas, living costs alone can rival local tuition. US universities’ own estimates put housing and food at roughly US$20,000 to US$23,000 a year, and the UK student visa benchmark for London works out to 1,529 pounds a month, before flights home.

Is a degree still worth it?

Most Singaporeans think so, even those who find it expensive. In a survey we conducted of 1,088 adults, 2 in 3 said a university education is expensive, yet 71.3% of that group still believed a degree is worth the cost.

The labour market data leans the same way, with degree holders earning higher median salaries. That said, the conversation has shifted since our fieldwork, with skills-based hiring and alternative pathways gaining ground.

In my opinion, the planning conclusion is unchanged. Saving for a degree keeps the option open. If your child ends up not needing the fund, the money can flow into their first home, a wedding, or your own retirement instead. The reverse, needing the fund and not having it, is a much harder position.

How Much Do You Need to Save?

For a local degree including living expenses, a typical target works out to a few hundred dollars a month, started early. The exact figure depends on your child’s age and the returns your savings earn, so let’s make it concrete.

Take Sarah, whose daughter is 2 years old. Her daughter would enter a local university in 17 years, at 19.

A local degree costs $81,890 today, including living expenses. Projecting tuition at 2.68% education inflation and living costs at 2.14% headline inflation, Sarah’s target in 17 years is about $123,000.

Saved as plain cash, that’s roughly $600 a month for 17 years. If her savings earn a modest 3% per year, the monthly figure drops to around $460. At 4%, it’s about $420.

The lesson in Sarah’s numbers: returns help, but time helps more. If she had started at her daughter’s birth, the same 3% plan would need meaningfully less each month.

Your own target will differ with your child’s age, the path you’re planning for, and whether they’ll live at home. To run your own numbers, use our education fund calculator.

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

Before You Save: Get the Foundation Right

An education fund runs for up to 20 years, and a plan that long fails when a short-term shock hits. Before committing money to a 20-year goal, make sure three basics are in place.

First, an emergency fund of six to 12 months of expenses, so a retrenchment or a big repair bill doesn’t force you to raid your child’s fund.

Second, adequate life cover on the parents. The education fund only works if you’re around to keep filling it, or if enough insurance pays out when you’re not. You can check how much life cover you need in a few minutes. For most parents, term life insurance is the affordable way to close that gap, while some prefer whole life insurance for cover that lasts beyond the child-raising years.

Third, proper hospitalisation coverage for the whole family, since a single large hospital bill can undo years of disciplined saving.

None of this is exciting, but it’s what keeps the plan on track when something goes wrong.

7 Ways to Fund Your Child’s Education

There’s no single right answer here. Each route trades off risk, returns, flexibility, and discipline differently, and most families end up combining several.

1) Cash savings

The simplest route: a dedicated savings account, topped up monthly. It’s safe, liquid, and hard to get wrong. The catch is that bank interest has historically trailed education inflation, so cash alone tends to lose purchasing power against your target over 20 years. Best for near-term needs, like preschool fees, and as the stable core of a longer plan.

2) Investments

Investing in shares, ETFs, or unit trusts offers the best odds of outpacing education inflation over a long runway. The trade-off is volatility: markets can fall exactly when the fees are due. A common approach is to invest aggressively while the child is young, then shift progressively into safer assets in the final five or so years. It demands discipline, and returns are never guaranteed.

3) Endowment and education savings plans

Education endowment plans are insurance-based savings plans that mature around university age, usually with capital guaranteed at maturity and modest projected returns. Their strength is forced discipline and certainty of timing. Their weaknesses are real too: returns are typically lower than investing, surrendering early often means losses, and the plans are rigid if your child’s path changes. In my opinion, they suit savers who value certainty over maximum returns, but they’re one option among several, not the default answer.

4) Government schemes: CDA, Edusave, and PSEA

Singapore quietly co-funds a meaningful slice of your child’s education, and many parents don’t max it out. The Child Development Account comes with a $5,000 First Step Grant for a first or second child, and the government matches your deposits dollar for dollar, up to $4,000 for a first child and more for later birth orders (as of 2026). CDA funds pay for approved childcare, preschool, and healthcare until the year your child turns 12.

Edusave then receives annual government contributions ($230 for primary, $290 for secondary students in 2026) for school and enrichment fees. Unused CDA money flows into the Post-Secondary Education Account at 13, where it can later pay for polytechnic or university fees, and you can keep topping it up with co-matching until the cap is reached. These schemes won’t fund a degree on their own, but they’re free money, so claim them first.

5) CPF Education Loan Scheme

The CPF Education Loan Scheme lets you use your own Ordinary Account savings to pay your child’s subsidised tuition fees at approved local institutions. It solves a cash-flow problem without touching your take-home pay. But it’s a loan, not a withdrawal: your child must repay the amount plus accrued interest, in cash, starting one year after graduation. Every dollar out of your OA also stops compounding for your own retirement, so use this route with your eyes open.

6) Government student loans (HESL)

From 1 July 2026, the Higher Education Student Loan replaced the old Tuition Fee Loan and Study Loan at the local universities, polytechnics, and other institutions. It covers up to 90% of subsidised tuition fees, with an optional means-tested living allowance, and stays interest-free until your child graduates, after which repayment runs up to 10 years. A loan shifts the burden from parent to graduate, which some families consider fair and others prefer to avoid. We compare this and the other routes in detail in our guide to the six ways to fund a university education.

7) Scholarships and bursaries

The best-value route of all, when it’s available. Scholarships reward merit and bursaries support lower- and middle-income households, and both can cut the bill dramatically. One caveat: neither is guaranteed, so they belong in your plan as a bonus, not as the foundation.

Common Mistakes Parents Make

Starting late. The maths is unforgiving. The same target costs far more per month at age 10 than at age 1, because you’ve lost both time and compounding.

Raiding the fund. A renovation, a car, a market dip that “will recover”. Education funds get spent on other things unless they’re kept strictly separate.

Funding education before retirement. Student loans exist for degrees, but nothing similar exists for your own retirement.

Ignoring inflation. Saving towards today’s $81,890 leaves you roughly 40% short of the projected bill in 20 years.

Over-committing to rigid plans. Locking your entire education budget into instruments with heavy surrender penalties leaves no room for life to change. Keep part of the fund flexible.

Your Child Education Planning Checklist

- Secure the foundation: emergency fund, life cover, and hospitalisation plans in place.

- Claim the government schemes: open and top up the CDA to the co-matching cap if you can.

- Decide the path you’re planning for: local or overseas, and whether your child will live at home.

- Set the target in future dollars, using education inflation (2.68% historically, 4% to be prudent), or use our calculator.

- Choose your mix of funding routes, matching risk to the years remaining.

- Automate the monthly amount so the plan doesn’t depend on willpower.

- Review yearly, and de-risk the fund as university approaches.

A Final Word

An education fund can look daunting when you stare at the 20-year total. Broken into a monthly sum from your child’s early years, it rarely is.

You don’t need to get everything perfect. Claim the schemes you’re entitled to, protect the plan with the right insurance, start the monthly habit, and adjust as your child’s path becomes clearer.

And if you’d rather not piece this together alone, our FullCircle comprehensive financial planning session looks at your child’s education fund alongside your protection, retirement, and estate plans, so one goal isn’t quietly funded at the expense of another.

Your child’s future is worth planning for. Start now, and let time do most of the work for you and your loved ones.

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.