Do you know how much you spend each month?

If you’re serious about growing your net worth and achieving your financial goals, the first step is understanding your numbers — your income, expenses, and savings. From there, you can tap into the wide range of personal finance tools available to help you manage and optimise your money.

Curious about how well Singaporeans track their spending, we surveyed 984 adults aged 18 and above to learn more about their habits.

Here’s what we discovered.

Key Findings

- 1 in 2 adults in Singapore have no idea how much they spend every month

- Those aged 18 to 24 are the least likely to know how much they spend

- 71.9% of those who track their monthly spending don’t usually overspend

These are some of the interesting statistics on spending habits in Singapore we’ve found. From the study, we’re also able to extract some insights that can help you make better financial decisions.

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

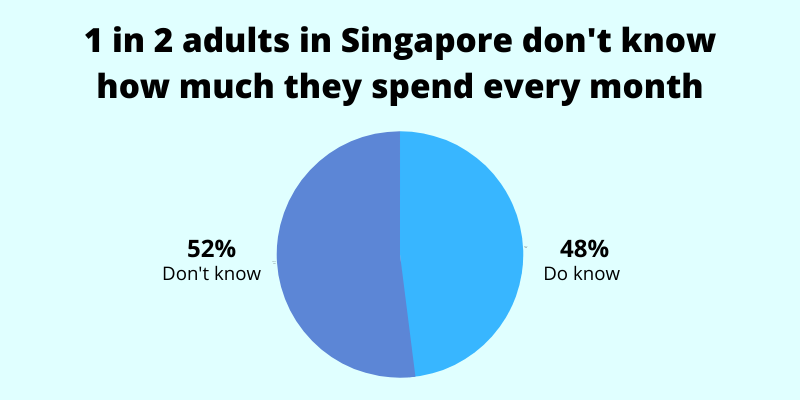

1 in 2 Adults in Singapore Have No Idea How Much They Spend Every Month

Less than half of the respondents (48%) say they know how much they spend every month, leaving a slight majority (52%) not knowing.

Note: Men and women are equally likely to not know how much they spend (51.6% vs 52.4%).

Why are people not paying attention to their spending?

Here are some possible reasons:

- It can be a hassle to track expenses

- They don’t see a need for it

- Fear of what they would find

- Creates additional stress

If you’re part of the half that’s not tracking your monthly spending, you may be exposing yourself to even bigger problems such as living from paycheck to paycheck, or having a low savings rate.

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

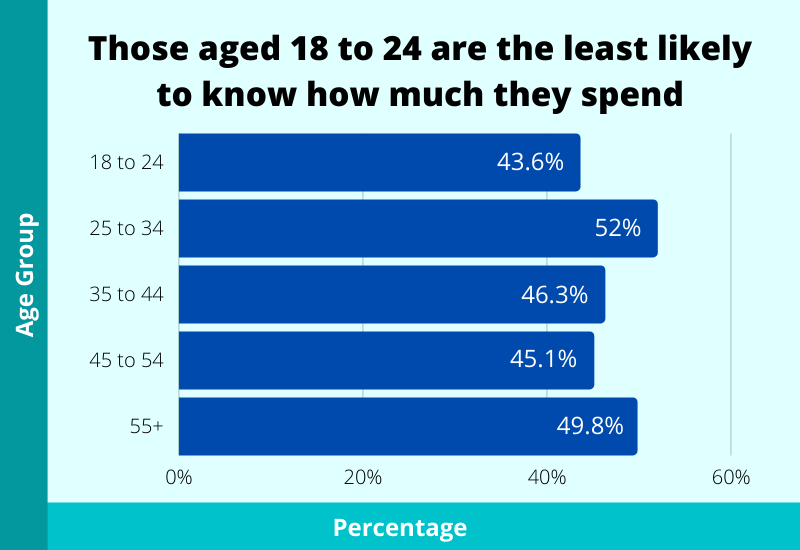

Those Aged 18 to 24 Are the Least Likely to Know How Much They Spend

How are the spending habits of youths and millennials in Singapore?

We found that among the respondents aged 18-24 years, only 43.6% know how much they spend every month. This is the lowest percentage among all our respondents.

The younger generation might not be taking full advantage of having the longest runway. By being more attentive to how much they spend, the odds of having more savings increase, thus leading to greater returns over the long run (if they make better use of their money).

On the flip side, those aged 25 to 34 have the highest percentage (52%) of respondents who knew their monthly spending. This could be likely due to having multiple financial commitments during that period such as a wedding, getting their first property and having kids.

The next highest (49.8%) are those aged 55 and above. This is possibly due to retirement looming around the corner.

These findings suggest that when one is closer to major financial goals and commitments, they’re more likely to take note of their finances.

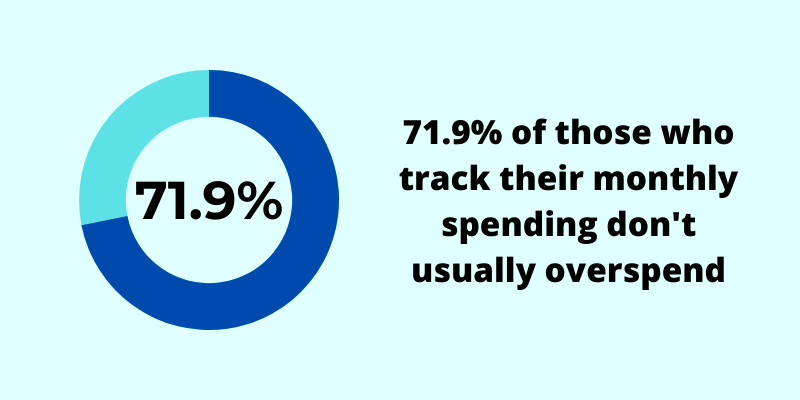

71.9% of Those Who Track Their Monthly Spending Don’t Usually Overspend

We take the view that if you know how much you spend every month, you’ve done some form of tracking (whether it’s knowing every single expense item or just your monthly numbers).

Of those who do know their monthly spending, around one-quarter (28.1%) of respondents say they usually overspend.

One likely reason for consumers who track their expenses yet still overspend is emotional spending (e.g., spending more because you’re feeling happy or sad). In those moments, emotions can overrule logic.

However, nearly three-quarters (71.9%) of those who track their monthly spending don’t usually overspend. And that also means that if you do track, you are 2.6 times more likely to stick within a spending limit.

By monitoring your spending, you would know whether you’re going to overspend (or have already overspent). With that knowledge, you can adjust accordingly. Keeping your financial goals and budget in mind will motivate you to stay within your budget so that you can achieve your goals.

When the “pain” of overspending or not saving enough is greater than the immediate “pleasure” you can get from frivolous spending (e.g., delayed gratification vs immediate gratification), you’re more likely to stick to your budget.

Wrapping Up

From the survey findings, we’ve come up with 4 tips to help you achieve your financial goals:

- Create a budgeting plan.

(Hey, even the government does it!). Decide how much of your income should be allocated to needs, wants and savings. If you have no idea where to start, take a look at the 50/30/20 budgeting rule. - Save first, spend later.

Once you receive your monthly income, transfer the amount you intend to save to a separate account (and make it difficult to withdraw or spend it). - Track your expenses.

The remaining amount is what you can use for expenses, such as insurance (e.g., term plans or whole life plans), food, and allowances. You can track your expenses for free using a mobile app (e.g., Seedly), an online expense calculator or an excel template. - Optimise your expenses.

For each expense item, decide whether to leave it as it is, find a cheaper/better alternative, or eliminate it. For example, checking multiple delivery apps before ordering helps you reduce costs.

Taking charge of your finances can be a tough one, but it goes a long way.

By taking small steps, you’re able to build habits that once seemed impossible, and save more money in the process.

To learn more about how to budget effectively, check out this guide. It includes a useful infographic too.

Methodology

This survey was conducted online using Google Surveys. The survey received 1,299 completed responses – 984 with known demographics (age and gender). Only those aged 18 and above in Singapore were surveyed. Post-stratification weighting is applied to ensure an accurate and reliable representation of the total population. Responses were collected from 17 Feb 2021 to 19 Mar 2021.

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.