…Compare and Save Precious Time & Money

1179+ Singaporeans have benefitted from our comparisons

- Avoid multiple agents yet be able to compare across 18 insurance companies

- Our DeepDive™ provides an in-depth comparison of the best SRS endowment/annuity plans in Singapore

- Tailored to your specific needs with personalised quotes and premiums

- Secure your retirement by receiving guaranteed (and non-guaranteed) income

(We’re pausing the comparisons for now.)

We’re Mentioned On

The Purpose of a SRS Annuity Plan

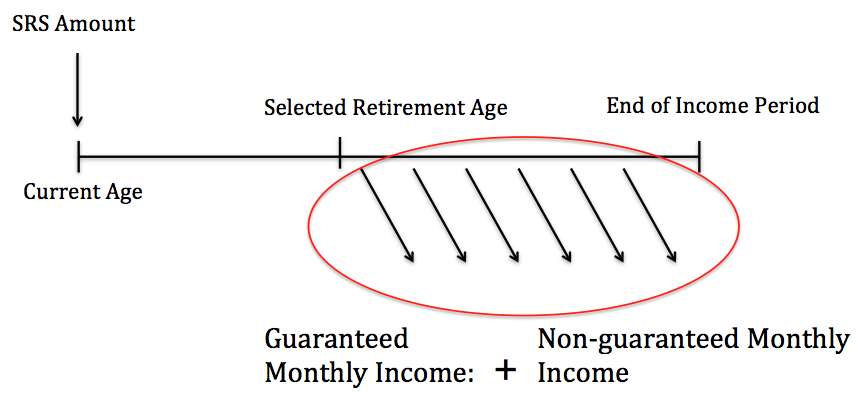

In a SRS endowment/annuity/retirement plan, you fund it by setting aside monies from your Supplementary Retirement Scheme (SRS) account, wait till your selected retirement age…

And then you can receive a monthly income (guaranteed + non-guaranteed) for a period of time (usually 10 years).

(If you’re new to SRS endowment plans and want to know more about it instead, read this guide first.)

Best SRS Endowment/Annuity Plans in Singapore (Comparison for 2024)

If you like the idea of a SRS endowment plan, what’s next?

Finding the best one of course!

You’re using your hard-earned money and you’ll definitely want to make the best decision (with no regrets in the future).

But SRS endowments come in all shapes and sizes… and one size doesn’t fit all.

The only way to find the best one for you is to do an in-depth comparison across the different plans offered by the different insurance companies.

And that’s what we’re good at.

Here’s a non-exhaustive list of SRS endowment plans that we can compare:

| Insurance Company | Plan Name |

| AIA | Retirement Saver (IV) Smart Wealth Builder (II) |

| Singlife with Aviva | Singlife Flexi Life Income (previously MyLifeIncome III) |

| Manulife | ReadyBuilder (II) RetireReady Plus (III) |

| Income Insurance (formerly NTUC Income) | Gro Retire Flex |

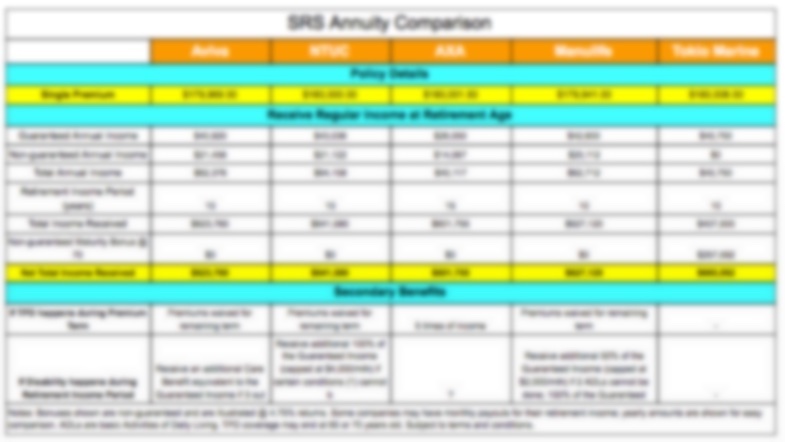

What’s in Our SRS Annuity Comparison DeepDive™

Unlike others, our DeepDive™ gives you the Good and the Bad…

So you will be equipped to make better decisions.

What we’ll cover in the comparison:

- How much is the single premium

- Guaranteed annual income

- Non-guaranteed annual income

- Number of years to receive the income

- Any additional non-guaranteed payouts

- Total potential payout

- Any secondary benefits

- Any available discounts or promotions

- Potential disadvantages

- Anything else you wish to know…

We spent hours scrutinising policy documents so that you don’t have to.

But, We Do Things Differently

Unlike others, we don’t publish these comparisons online (comparisons from other sites are usually generic in nature, may contain outdated information, and their quotes aren’t specific to your profile and your needs). Also, we don’t send these these personalised comparisons directly to your email.

We do this on an appointment basis (via zoom video call or a meet-up) to first understand your situation before going through the comparison with you. This ensures that we can provide appropriate advice there and then.

It may sound troublesome to you, but hear us out.

3 Reasons Why We Need to Meet

(Either through a zoom video call or a meet-up)

You just want to look at the numbers… you got no time… you don’t want to meet strangers.

Perhaps you’re here because you were doing research online or came looking for more information when someone – friend or agent – told you about this.

So you may thinking, “just email the comparison and quotes to me!“

As consumers ourselves, we understand the convenience of that.

But a mere comparison table will not help you make a concrete decision (one that you can set in stone).

Here are 3 reasons why there’s a need to meet:

1) Give Accurate Recommendations

Can you be absolutely sure of what you want? Could there be something that you may have missed?

A wrong decision might lead to a lifetime of regrets.

If you go to a doctor and without asking you anything, the doctor gives you medicine for this, this and this.

Would you have full confidence in the solution? No.

And that’s why there’s a need to understand your situation first before we give a recommendation – we’re not in the business of pushing products.

2) Requirement of MAS

In the Financial Advisers Act, it is stated that in order for a recommendation to be made, information on the client has to be gathered first.

Any inaccurate or incomplete information may affect the suitability of the recommendation.

Over the years, MAS has imposed stricter regulations to ultimately protect Singaporeans (and that includes you).

It is there for a reason and that is to ensure that you don’t end up with an unsuitable plan.

3) Touch on Fine Prints

What’s the purpose of a comparison table?

It’s to present information in an organised and simple way, so that you can make a decision based on it.

But can you really make an informed decision from it?

If you can easily do that, there wouldn’t be a need for two-digit pages of policy documents (for just one plan).

There are fine prints and clauses that might make or break your decision.

And that’s why we meet to not only show you the comparisons but to go through any critical pointers that you must be aware of.

We don’t want to overpromise and underdeliver.

(We’re pausing the comparisons for now.)

What Singaporeans Are Saying (Reviews & Testimonials)

(We’re pausing the comparisons for now.)

We Compare 18 Insurance Companies to Find the Best SRS Endowment Plan for Your Needs

This Is Great if You:

- Don’t know which plan is the best

- Don’t wish to waste precious time and money going to individual companies for quotes

- Don’t wish to tear your hair out looking through product documents

Our Trusted Providers

- AIA

- Singlife with Aviva

- Friends Provident

- China Life

- Generali Worldwide

- China Taiping

- Income Insurance (formerly NTUC Income)

- Manulife

- LIC

- Old Mutual

- Swiss Life

- HSBC Life

- AXA

- Tokio Marine

- Singlife

- Transamerica

- Etiqa

- FWD

Frequently Asked Questions

- What is a SRS endowment/annuity plan in Singapore?

It is a policy that is geared to provide regular income during your retirement years. It pays out an income, which consists of guaranteed and non-guaranteed amounts, once you hit the selected retirement age. The length of income being paid out depends on your selected payout duration. - Is a SRS endowment plan a good option?

There are many ways to invest your SRS funds, and the SRS endowment plan is just one of them. It can provide potential returns which are higher than inflation, and is typically capital-guaranteed upon maturity, so it’s meant for those who are more conservative. Having said that, it’s best to speak to a financial advisor first. - Is this service free?

Yes, there’s no fee involved. - How long does the appointment take?

It typically takes around 45 minutes. However, it can be longer for more complex situations or if you have further questions. - Are there any obligations?

Depending on your situation, we may or may not recommend solutions. If we do, it’s entirely up to you to go ahead with it. As consumers ourselves, we dislike high-pressure tactics. - Should I bring my existing policies?

Yes! If you do have them, do bring them along (or a policy summary) as we can provide more accurate feedback. - How is this appointment conducted?

This can be done over a zoom video call or a meet-up.

(We’re pausing the comparisons for now.)