Estate planning is almost always an afterthought.

Most of us spend our working lives focused on earning, saving, and growing what we have. We rarely stop to think about what happens to it all when we’re no longer around. But we don’t build wealth just for ourselves. We build it for the people we love.

And if the basics of estate planning aren’t done properly, your money may not reach the people you intended. It can be tied up for months, eaten into by avoidable costs, or distributed by a formula the law decides for you.

The good news is that this is more straightforward than most people think. A lot of it can now be done online, and several of the key tools are free or close to it. This guide walks you through the whole picture, from the simple nominations everyone should make to wills, trusts, and planning for the years when you may not be able to decide for yourself.

One quick note before we start. This guide covers estate planning under Singapore’s civil law, which applies to non-Muslims. If you’re Muslim, your estate is governed by Muslim law instead, and the rules around who inherits work quite differently, so parts of this guide won’t apply to your situation.

The Three Pillars: Financial, Estate & Advance Care Planning

At every stage of life, there are three areas of planning that work together. I think of them as a single framework.

Financial planning is for while you’re alive and well. It’s how you build and protect your wealth.

Estate planning is for after you’ve passed on. It decides who receives what, and how quickly.

Advance care planning is for the in-between, the situation where you’re still alive but no longer mentally able to make your own decisions.

When one of these is missing, gaps appear.

You need sound financial planning first, because estate planning is meaningless if there’s nothing to pass on. There’s no point deciding how to distribute an estate that doesn’t exist.

And here’s the part most people overlook. If you’ve done your financial and estate planning but skipped advance care planning, and you then lose mental capacity, your family isn’t automatically given access to your assets to pay your bills. The money is still yours, but if you’re, in effect, neither here nor there, who steps in?

That’s why all three pillars matter. For the rest of this guide, we’ll focus on estate planning, then come back to advance care planning towards the end.

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

What Is Estate Planning (& Is It the Same as Legacy Planning?)

Estate planning is the process of deciding, in advance, who inherits your assets when you die, how much they receive, and how smoothly it all reaches them.

You’ll sometimes see the term “legacy planning” used instead. People draw fine distinctions between the two, with legacy planning framed as the broader, more values-driven version. In my opinion, for most Singaporeans the two mean much the same thing in practice, so we’ll stick with “estate planning” throughout.

Done well, estate planning gives you a few clear benefits:

- You choose who gets what, rather than leaving it to the law.

- Your assets reach your family faster.

- The overall cost of unlocking and distributing your estate is lower.

- You reduce the risk of disputes and bad blood between family members.

It’s a broad topic with a lot of moving parts, so let’s start with who actually needs it, then with what’s at stake if you do nothing.

Who Needs Estate Planning & When to Start

There’s a common belief that estate planning is only for the wealthy or the elderly. It isn’t.

If you have any assets, any debt, or anyone who depends on you, you already have an estate worth planning. The question is simply how much planning makes sense for your stage of life.

A few moments when it is worth sitting down to sort this out:

- When you start working and saving. Even a simple CPF nomination matters once your CPF balance and first insurance policies start to build up.

- When you get married or have children. You now have dependants. A will lets you appoint a guardian for young children, and nominations make sure your family has quick access to cash.

- When you buy property. How you hold your home decides whether it goes automatically to a co-owner or forms part of your estate.

- When you build real wealth or run a business. This is where wills, trusts, and succession planning start to earn their keep.

- When your circumstances change. Divorce, remarriage, a new child, or the death of a beneficiary are all triggers to review what you have put in place.

The honest answer to “when should I start” is now, at whatever level fits your life today. Estate planning isn’t a one-off task. It’s something you set up early and revisit as things change.

What Happens If You Don’t Do Proper Estate Planning

One of the main reasons why you would want to do estate planning is to make sure your assets go to your intended beneficiaries, and to not let the law decide for you.

But how many people actually get the basics down?

The numbers on estate planning tell the story:

- $278 million in unclaimed monies is sitting with the Public Trustee, including $184 million of un-nominated CPF savings

- Nearly 2 in 3 working-age CPF members (only 36% of those aged 16 to 64 have nominated) haven’t made a CPF nomination

- Just 22% of Singapore residents have a legally drafted will, and only 12% have set up a trust

- Only 1 in 7 Singaporeans has made a Lasting Power of Attorney, and even among the over-65s, just 1 in 4 have

- More than half (51%) of older Singaporeans without an LPA wrongly believe their children could automatically act for them if they lost mental capacity

- Over 8,000 insurance payouts were last counted as unclaimed, and there’s now no public register left to track them

So what actually goes wrong when there’s no plan? Your assets are frozen on death and nobody can touch them until the courts appoint someone to step in. That person has to apply for a court order, gather and value everything, settle debts, and only then distribute what’s left, according to a fixed legal formula rather than your wishes. It’s slower, it costs more, and it leaves your family to untangle it all.

We’ll come to that formula shortly.

Is There Inheritance or Estate Tax in Singapore?

Here’s some good news before we go further. When you pass on, the government won’t tax your estate.

Singapore used to have an estate duty, a tax on the assets you left behind. It was abolished for all deaths on or after 15 February 2008, according to IRAS. There’s no inheritance tax either.

In practice, this means more of what you’ve built reaches your family, and you don’t need to structure your estate around avoiding death taxes the way people do in the United Kingdom or the United States.

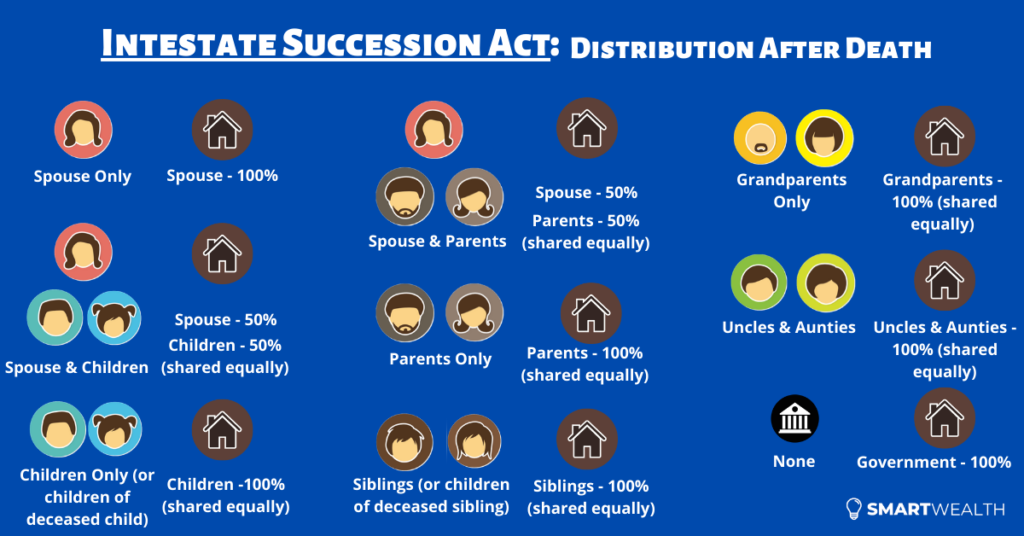

How Your Estate Is Distributed If You Die Without a Will

When someone dies without a valid will, they’re said to have died “intestate”. And when that happens, you don’t get a say in how it’s split. The law sets the formula instead.

For most non-Muslims who die without a will, someone, usually the next-of-kin such as a spouse or eldest child, has to be appointed as the administrator of the estate. To get that authority, they apply to the court for a Grant of Letters of Administration.

The administrator then has to:

- Track down all the deceased’s assets and debts.

- Open an estate bank account.

- Transfer money from the various banks into that account.

- Pay off all outstanding debts and liabilities.

- Distribute whatever’s left to the beneficiaries.

Who gets what is set by the Intestate Succession Act, which applies to non-Muslims. Here’s how those rules split an estate:

If you’re Muslim, these rules don’t apply to you. Your estate is distributed under Muslim law, mainly through the faraid system, which sets fixed shares for eligible heirs.

There’s an important catch, though, and it applies whether or not you’ve made a will. Not every asset is distributed this way. Things like jointly held property, joint bank accounts, CPF savings, and insurance proceeds can be treated very differently, depending on what you’ve set up beforehand.

That trips a lot of people up, so let’s look at it next.

Where Your Different Assets Actually Go

Here’s a myth worth clearing up early. Many people assume a will controls everything they own. It doesn’t.

Some of your biggest assets sit outside your will entirely. They go to whoever you’ve nominated, or to whoever co-owns them, no matter what your will says. Get this wrong and your careful instructions can be quietly overridden.

Here’s how the main asset types are treated.

Your property. Where your home goes depends on how you hold it. If you and another person own it as joint tenants, the right of survivorship applies. When one owner dies, the other automatically owns the whole property, and it never enters your estate or your will. If you own it as tenants-in-common, each of you holds a defined share (say 50% each), and your share does form part of your estate and can be left in your will. For many married couples, the family home is held as joint tenancy so it goes straight to the surviving spouse. This is one of the most important things to check, because it quietly decides what happens to your most valuable asset.

Your CPF savings. CPF monies don’t form part of your estate and can’t be given away in your will. They go only to whoever you’ve named in your CPF nomination. If you’ve made one, your CPF reaches the people you chose. If you haven’t, it’s handed to the Public Trustee to distribute under the intestacy rules, which costs your family time and a fee.

Your insurance payouts. A life insurance policy with a nomination usually pays out directly to your nominees, outside your estate. Without a nomination, the money normally falls into your estate and is distributed from there. There’s a catch around how a will interacts with this, which we’ll come to under insurance nominations shortly.

Joint bank accounts. Money in a joint account often goes to the surviving account holder, depending on how the account was set up. As with property, this can sit outside your will.

The takeaway is simple. A will is essential, but it’s only one piece. To make sure everything reaches the right hands, you need to line up your nominations and the way you hold your assets alongside it. That’s what the core estate planning tools are for.

The Core Estate Planning Tools

You don’t need every tool, and you certainly don’t need to do everything at once. But there are four that form the backbone of most plans. Here’s how they compare at a glance.

| Tool | What it covers | When it takes effect | Goes through probate? |

|---|---|---|---|

| CPF nomination | Your CPF savings | On death | No, paid out directly |

| Insurance nomination | Policy payouts with a death benefit | On death | No, paid out directly |

| Will | Everything else in your estate | On death | Yes |

| Trust | Specific assets you place into it | While alive or on death | No |

Let’s go through each one.

CPF nomination

For many Singaporeans, CPF is one of the largest sums they’ll leave behind, so this is the single most important box to tick. As we saw earlier, your CPF doesn’t go through your will. It goes only to the people you’ve nominated.

Make a CPF nomination and your savings reach your loved ones quickly and at no cost. Skip it, and your CPF is handed to the Public Trustee, who distributes it under the intestacy rules and charges a fee to do so.

There are three types of nomination, and most people only know about the first:

- Cash nomination. Your nominees receive your CPF savings in cash. This is the default and the most common choice.

- Enhanced Nomination Scheme (ENS). Your savings are transferred into your nominees’ own CPF accounts instead of paid out in cash, which can keep the money growing and protected within CPF.

- Special Needs Savings Scheme (SNSS). Designed for parents of children with special needs, this pays out your CPF in regular monthly amounts rather than a single lump sum.

The good news is that the standard cash nomination is far easier to make than it used to be. You can now do it online with your Singpass in a few minutes, instead of going down to a service centre in person. You’ll still need two witnesses, who can’t be your nominees, but they can take part online too. The ENS and SNSS options can’t be done online yet, so you’ll need to arrange an appointment with the CPF Board for those.

Insurance policy nomination

If you hold life insurance with a death benefit, you can decide who receives the payout, and in what shares, by making an insurance policy nomination. There are two kinds:

- Revocable nomination. You can name anyone, keep full control, and change the details at any time. Most nominations are revocable.

- Irrevocable (trust) nomination. This can only be made in favour of your spouse and/or children. The payout is locked in for them, you give up your own rights to the policy, and you can’t change it without their consent.

One thing worth knowing about wills. A later will can override a revocable nomination, but only if it specifically disposes of that policy’s death benefits and includes the details the law requires. A general will leaving everything to someone won’t do it. A trust nomination, on the other hand, can’t be undone by a will at all, only with your beneficiaries’ consent.

The big advantage is speed. Once a nomination is in place, the insurer pays your nominees directly after a successful claim, giving your family liquidity exactly when they need it, without waiting on probate.

Bear in mind that a nominated policy pays out as a lump sum, which may not suit a nominee who isn’t comfortable handling a large amount at once. If you want both liquidity and staggered payouts, you can nominate some policies for immediate cash and leave the rest to your will, where a testamentary trust can release the money gradually.

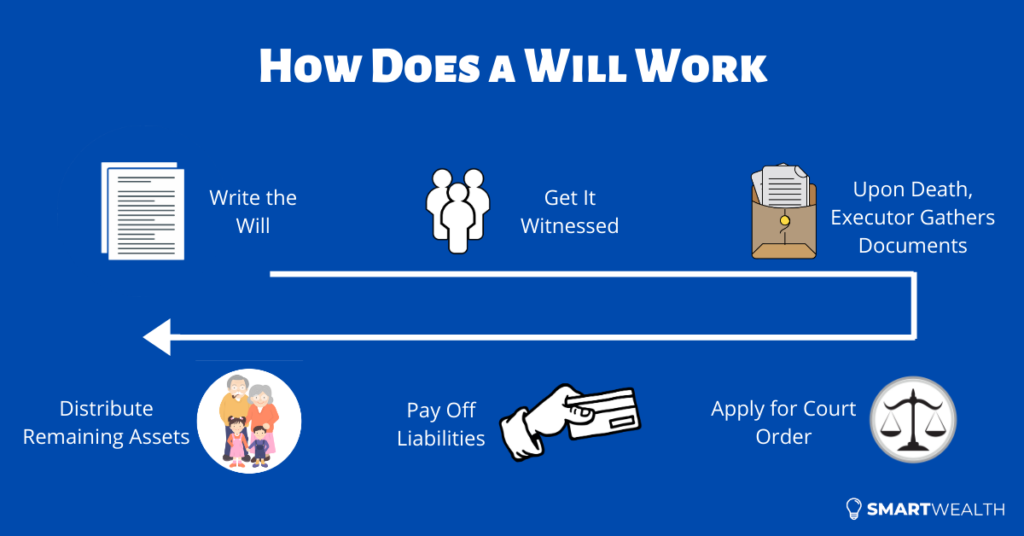

Making a will

A will lets you decide who receives everything else in your estate, the assets that don’t already go to someone through a nomination or joint ownership.

To be valid, your will has to be signed in front of two witnesses, who can’t be beneficiaries or married to one, and then kept somewhere safe and accessible. When you die, the executor you’ve named gathers your documents and applies to the court for a Grant of Probate. That gives them the authority to settle your debts and distribute your assets according to your wishes.

A will also does two things nominations can’t:

- Appoint a guardian for your children if they’re still young, which is often the real reason new parents finally sit down to write one.

- Set up a testamentary trust, also called a will trust, so money can be released in stages or as a monthly amount rather than handed over all at once.

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

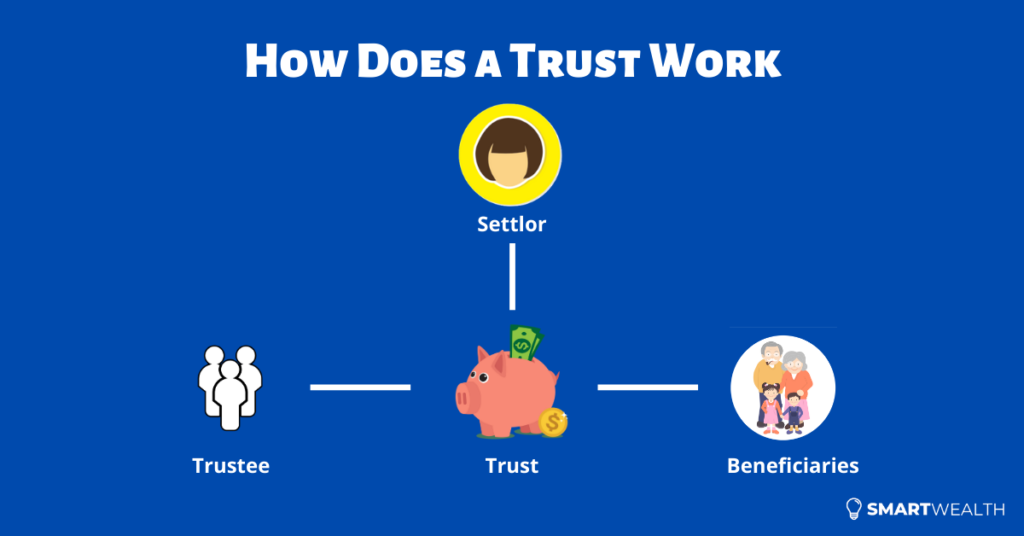

Setting up a trust

Setting up a trust isn’t only for the wealthy. It can make sense for ordinary individuals too, especially where you want more control over how and when your assets are used.

A trust involves three parties: the settlor (you, the person setting it up), the beneficiaries (who the assets are for), and the trustee (the person or company that manages and distributes the assets on your terms). A trustee doesn’t have to be a trust company. It can be someone you know and trust.

The appeal of a trust is control and flexibility that the basic tools can’t offer. You can decide that a child only receives their share at a certain age, or that funds are released over 20 years, or used only for education or medical needs.

There are several types to suit different situations, including:

- Trust (irrevocable) nomination

- Will trust (testamentary trust)

- Living trusts

- Standalone insurance trust

- Property trust

- Standby living trust

Planning for Incapacity

Everything so far deals with what happens when you die. But there’s another scenario worth planning for, the one where you’re still alive but no longer able to make your own decisions, perhaps through a stroke, dementia, or a serious accident.

Here, your will and your nominations are no help, because none of them have kicked in. You’re still alive and your assets are still yours, but if you can’t manage them and nobody has the authority to step in, your family is left stuck.

Three separate tools prepare for this, and all of them have to be set up while you’re still mentally capable: a Lasting Power of Attorney, an Advance Medical Directive, and an advance care plan. They each do something different, so it’s worth understanding all three.

Lasting Power of Attorney (LPA)

A Lasting Power of Attorney lets you appoint someone you trust, called a donee, to make decisions on your behalf if you lose mental capacity. You can give them authority over your property and finances, your personal welfare, or both.

This is arguably the most important incapacity tool, and the process has become much simpler. LPAs are now made and submitted online through the Office of the Public Guardian Online (OPGO) portal using your Singpass.

There’s a cost angle worth knowing too. As of 2026, the application fee for the standard LPA (Form 1) is free for Singapore Citizens. You’ll still pay a separate fee to a certificate issuer, an accredited doctor, a lawyer, or a psychiatrist, who confirms you understand what you’re signing. That typically runs from around $50 with a doctor to a few hundred dollars with a lawyer.

Advance Medical Directive (AMD)

An Advance Medical Directive is a legal document that tells your doctors you don’t want extraordinary life-sustaining treatment used to prolong your life, if you become terminally ill and are no longer conscious or able to make the decision yourself.

It’s entirely your choice to make one, and you can only do so while you’re mentally sound and at least 21 years old. The form needs to be signed in front of two witnesses, one of whom must be your doctor.

Advance care plan (ACP)

An advance care plan is where you set out your healthcare preferences and values, so your loved ones and medical team understand what matters to you if you can’t speak for yourself. It isn’t legally binding the way an LPA or AMD is, but it gives everyone valuable guidance at a difficult time.

What if you don’t have an LPA?

This is the situation to avoid. If you lose mental capacity without an LPA in place, your family can’t simply take over your affairs. They have to apply to court to be appointed as your deputy under the Mental Capacity Act.

That process takes time, costs money, and adds legal stress at an already painful moment, all of which a simple LPA made in advance would have spared them. It’s the clearest argument for sorting this out early.

What It Costs & Where to Do It

One of the biggest surprises for most people is how little the essentials cost. Your two most important moves, a CPF nomination and an insurance nomination, are completely free. The bigger costs only come in when you need a lawyer or a professional trustee.

Here’s a rough guide to what each tool costs, as of 2026. Treat these as ballpark figures, since fees vary by provider and by how complex your situation is.

| Tool | Indicative cost (2026) |

|---|---|

| CPF nomination | Free |

| Insurance policy nomination | Free |

| Advance Medical Directive | No registration fee, though the doctor who witnesses it usually charges a consultation fee |

| Lasting Power of Attorney | Application free for Singapore Citizens, plus a certificate issuer fee, typically $50 to $300 depending on whether you use a doctor or a lawyer |

| Will | From around $200 through a will-writing service, and more if you engage a lawyer or have a complex estate |

| Trust | Varies widely, often from a few thousand dollars to set up, plus ongoing trustee fees |

| Probate or Letters of Administration | Court fees plus legal fees, depending on the size and complexity of the estate |

The takeaway is that you can put the most important protections in place for your family without spending anything at all, then add the paid tools as your needs grow.

A useful starting point: MyLegacy@LifeSG

It’s worth knowing about MyLegacy@LifeSG, a government portal that pulls together information on end-of-life and incapacity planning in one place. You can use it to understand the landscape and access some of the basic services, such as your CPF nomination and LPA, and it guides families on what to do after a loved one passes away.

It’s a helpful way to get oriented and to handle the simpler tasks. That said, estate planning gets more involved once you have several assets, a business, dependants with particular needs, or you want everything coordinated rather than scattered. That’s where it pays to get proper guidance, which we’ll come to at the end.

How to Leave a Larger Estate for Your Loved Ones

So far we’ve focused on directing your assets to the right people. But many people also want to do the opposite of shrinking their estate, which is to grow what they leave behind. This is where estate planning shades into legacy planning.

The foundation comes first. Before thinking about leaving more, make sure the basics of insurance protection are covered, so your family is protected if something happens to you prematurely. That usually means adequate coverage through a term insurance or whole life insurance policy. It also means you have a plan in place to save for retirement and to set aside something for your children’s education.

Once that foundation is solid, there are a few tools designed specifically to enlarge what you pass on:

- Three-generation lifetime income plans, which can provide income for your own retirement and then continue for the next generation.

- Term insurance until 99, which stretches life cover deep into old age at a lower cost than whole life.

- Single premium (jumbo) whole life insurance, where a one-off lump sum creates a much larger payout for your beneficiaries.

- Universal life insurance, often used by higher-net-worth individuals to leave a sizeable legacy.

These are optional tools, not essentials, and the right mix depends entirely on your goals and circumstances. As with any insurance, cover is subject to underwriting and health disclosure, so it’s worth looking into these earlier rather than later.

Your Estate Planning Checklist

Estate planning can feel like a lot, so here’s a simple order to work through. Start at the top and work down as your life gets more complex.

- Make a list of what you own. Before anything else, write down your assets, debts, insurance policies, and important account details in one place. If this list doesn’t exist, your family may never know what you had. Our free FinSnap template gives you a ready-made way to capture it all.

- Make your CPF nomination. It’s free, it’s quick, and it covers one of your largest assets.

- Make your insurance nominations. Decide who receives your policy payouts, and how.

- Write a will. Cover everything else, name an executor, and appoint a guardian if you have young children.

- Consider a trust if you want more control over how and when your assets are used, for example for young children or a dependant with special needs.

- Set up a Lasting Power of Attorney. Protect yourself and your family in case you ever lose mental capacity.

- Look into an AMD and an advance care plan if you want a say in your future medical care.

- Review everything regularly, especially after marriage, a new child, divorce, or a death in the family.

Tick off the first few and you’ll already be ahead of most Singaporeans.

A Final Word

Estate planning isn’t about wealth, and it isn’t about age. It’s about making sure the people you love are looked after, with as little cost, delay, and stress as possible, at a time when they’ll already be coping with enough.

The encouraging part is how much of it is simple. A CPF nomination, an insurance nomination, and a will cover most people well, and the first two cost nothing. You add the more advanced tools only as your life calls for them.

The harder part is tying it all together, so your nominations, your will, the way you hold your property, and your insurance point in the same direction rather than working against each other. If you’d like a clear picture of where you stand and what to prioritise across protection, retirement, and estate planning, that’s what our FullCircle comprehensive financial planning session is for.

Whatever you do, do something. Even one nomination made today is a meaningful step for you and your loved ones.

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.