Trusts have a reputation for being only for the ultra-rich.

It’s a fair assumption, but no longer true.

With more Singaporeans building up CPF, property, insurance, and investments, a trust can be relevant to ordinary families too, in the right situations.

A trust is powerful, but it isn’t free, and for most people the basics of estate planning do the job at a fraction of the cost. So the real question isn’t “what is a trust”, it’s “do I actually need one”. This guide will help you decide.

Too Long; Didn’t Read

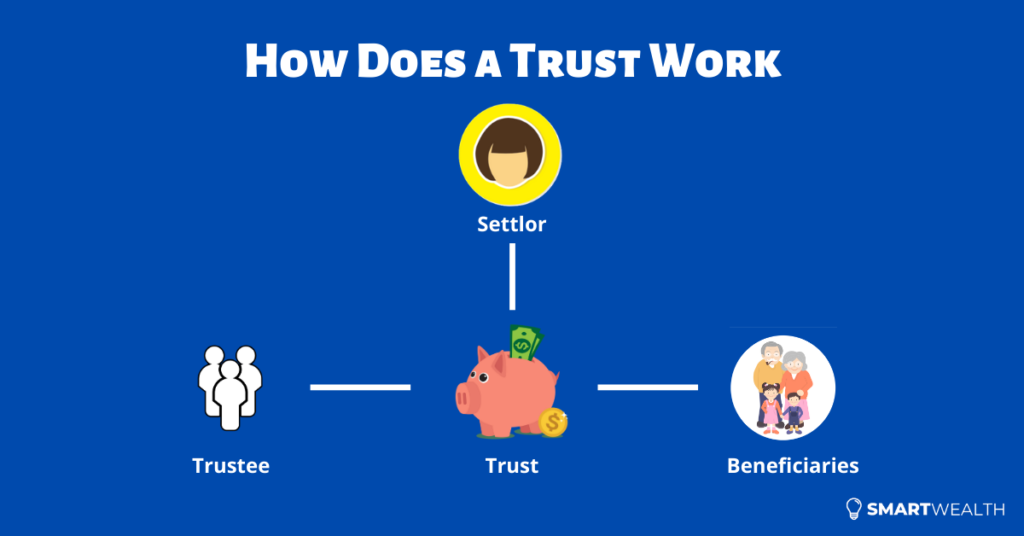

In a typical trust, the settlor (the person who creates it) sets aside assets into the trust. Those assets are held and managed by a trustee, who then distributes them to the beneficiaries the settlor has named.

That’s the whole idea in one sentence: you hand assets to someone you trust to manage and pass on, according to rules you set in advance.

Where it gets useful is in the detail, who controls what, when beneficiaries receive money, and what happens if you pass away or lose mental capacity. That’s what the rest of this guide unpacks.

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

What Is a Trust?

A trust is a legal arrangement where you (the settlor) hand assets to a trustee, who holds and manages them for the people you want to benefit (your beneficiaries).

You’ll sometimes hear the words “trust”, “trust fund”, and “trust account” used loosely. They’re broadly pointing at the same thing: assets set aside and managed for someone else under an agreed set of rules.

The trust can be funded by all sorts of assets, not just cash. Property, shares, and insurance policies can go in too.

The simplest way to picture it is a relay. You pass the baton (your assets) to the trustee, who runs the leg you can’t, and hands it on to your beneficiaries at the point and in the way you decided in advance. For a fuller picture of where a trust sits alongside wills and nominations, see our guide to estate planning in Singapore.

The Key Parts of a Trust

A trust can sound complicated, but it’s really just a few moving parts.

Settlor

The settlor is the person who creates the trust and puts assets into it.

You can set up a trust while you’re alive (a living trust) or have one created through your will after you pass away (a testamentary trust). Either way, you’re the one who decides the rules.

Trust property

Once a trust is created, it has to be funded with something. That can be cash, shares, residential or commercial property, or insurance policies, among other things.

A common reason to do this is to make delayed or staggered gifts, rather than handing everything over in one go.

Trustee

The trustee is the legal owner of the assets while they’re in the trust. Their job is to manage those assets and distribute them to your beneficiaries according to your instructions.

A trustee has a fiduciary duty, which means they must act in the beneficiaries’ best interests, not their own. Falling short can land them in legal trouble.

You can appoint a person you trust, or a professional trust company. A professional trustee costs money, but it spares your family the legal and financial responsibility, and the work gets done to a higher standard. One example is the Special Needs Trust Company (SNTC), which focuses on families with special-needs members.

Beneficiaries

Beneficiaries are the people or organisations the trust is set up to benefit. Most often that’s a spouse, children, or parents, but it can also be other relatives, friends, or a charity.

Trust deed

The trust deed is the legally binding document that sets out the rules: whether the trust is revocable or irrevocable, who the beneficiaries are, what the trustee can and can’t do, and how assets should be distributed.

Letter of wishes

The letter of wishes is a separate, more personal note from you to the trustee. It offers guidance on how you’d like things handled.

It isn’t legally binding the way the trust deed is, but a good trustee is expected to follow it, and it can carry weight if the trust is ever challenged.

Protector (optional)

A protector is someone appointed to keep an eye on the trustee. It’s optional, and most everyday trusts won’t need one.

Where it’s used, the protector can hold powers such as removing and replacing the trustee, or signing off on certain decisions. It tends to matter most for trusts meant to run for a very long time, across several generations.

Two Choices That Shape Every Trust

Beyond the parts above, two decisions do most of the work in defining how a trust behaves.

Revocable or irrevocable

A revocable trust can be changed or cancelled by you at any time. Most living trusts start out this way, which is handy when life keeps changing.

The trade-off is protection. Because you can still pull the assets back, the law generally treats them as still yours, so a revocable trust offers little shelter from creditors or a divorce claim.

An irrevocable trust is the opposite. Once it’s set up and funded, you generally can’t change it or take the assets back. In giving up that control, you also give up ownership, which is what allows this type of trust to offer some protection from creditors. That protection isn’t automatic or absolute, and timing matters, so it’s an area to work through with a professional rather than assume.

Fixed or discretionary

In a fixed trust, you spell out exactly who gets what, and the trustee simply follows the script. There’s no room to adapt.

In a discretionary trust, the trustee has some leeway over how much each beneficiary receives and when. They still have to act within the trust deed and your letter of wishes, and still owe that fiduciary duty, but they can respond to circumstances you couldn’t have predicted. Most trusts are discretionary for exactly this reason.

When a Trust Is Actually Worth It

A trust starts to make sense when it does something the simpler tools can’t. Just 12% of Singapore residents have set one up, as a recent survey found, and for most people that’s about right.

But some who genuinely would benefit, especially parents of young or vulnerable children, simply haven’t looked into it. Here are the situations where one is most often worth considering.

1) Providing for a special-needs child

If you have a child who may never be able to manage money on their own, the hardest question is what happens to them when you’re no longer around.

A trust can keep providing for that child long after you’re gone, releasing money steadily rather than in one lump sum, without putting the legal and financial burden on relatives. The SNTC was set up specifically for this, and is the most affordable route for most families.

2) Holding gifts for people who aren’t ready for them

Not everyone is equipped to handle a sudden windfall. We’ve all heard the stories: a payout meant to last years, gone within one.

A trust lets you stagger how money reaches your loved ones, a monthly sum, or amounts released at certain ages or milestones, rather than everything at once. That’s useful for young children or any beneficiary who might struggle with a large sum landing overnight.

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

3) Passing property to your children

Parents who are comfortable often start thinking about giving the next generation a head start, frequently through property.

One important update here. It used to be common to use a trust to buy property for a child and sidestep Additional Buyer’s Stamp Duty (ABSD). That door has largely closed. Since 2023, ABSD of 65% applies upfront when residential property is transferred into a living trust, according to IRAS. In other words, it is no longer the tax shortcut it once was.

So if you’re considering a property trust today, the reason should be control and timing (deciding when your child takes full ownership), not stamp-duty savings. Given the sums involved, this is very much one to plan with a professional.

4) Protecting hard-earned assets

Your assets are hard-earned, and you’d rather they reach the people you intend.

An irrevocable trust can offer a degree of protection from claims such as creditors or divorce, because the assets are no longer legally yours. That protection has limits, though. It generally won’t help if you move assets into a trust when you’re already in financial trouble, and it can be challenged in court. Treat it as a planning tool to set up well ahead of time, not an escape hatch.

5) Smoothing things for your family

When someone passes away, assets left through a will usually go through probate, the court process that confirms the will before anything can be distributed. That takes time.

Assets already sitting in a living trust can sidestep that wait, because they’re held by the trustee rather than locked in your estate. Worth knowing: a testamentary trust (one created by your will) doesn’t get this benefit, since it only comes into being through the will itself.

6) Keeping things private

A will eventually becomes part of the probate record, so its contents can be seen by others. A trust is private.

Who your beneficiaries are, what’s in the trust, and how it’s distributed can all stay confidential. For some families that privacy matters a great deal, and it’s a reason a trust is sometimes used alongside a will rather than instead of one.

What a Trust Won’t Do in Singapore

It’s just as useful to know what a trust isn’t for, because a few myths get carried over from overseas advice.

It won’t save you estate or inheritance tax. Singapore abolished estate duty for deaths on or after 15 February 2008, so there’s no “death tax” here for a trust to shield you from. If you’ve read that trusts cut inheritance tax, that advice is usually written for the UK or US.

It won’t save you ABSD on property anymore. As covered above, transferring residential property into a living trust now attracts ABSD upfront, so the old stamp-duty angle has largely gone.

It won’t undo financial trouble you’re already in. Moving assets into a trust once creditors are circling generally won’t protect them. The protection comes from planning early, while your affairs are in good order.

And it won’t replace the basics. A trust sits on top of good estate planning, it doesn’t stand in for a will, a CPF nomination, or an insurance nomination. More on that below.

Common Types of Trusts in Singapore

Trusts come in different shapes, mostly defined by when they’re created and how they’re funded. Here are the ones you’re most likely to come across.

Trust (irrevocable) nomination on an insurance policy

This is the closest thing to a trust that many ordinary policyholders already have access to, and it’s often confused with a full trust.

If you own a life insurance policy, you can make a nomination. A revocable nomination can be changed any time. A trust nomination is irrevocable: you give up your rights to the policy, it can only name your spouse and children, and the proceeds are ring-fenced for them. It’s free to make and can offer some protection, but the loss of control is the catch.

It isn’t a standalone trust so much as a nomination with trust-like effect. We cover the mechanics fully in our guide to insurance policy nominations.

Testamentary trust (will trust)

A testamentary trust is created through your will and only comes into effect after you pass away.

In your will, you name a trustee and set out how your assets should be managed and distributed. It’s useful when you don’t want beneficiaries to receive everything at once, for instance young children or relatives who’d struggle with a lump sum.

It’s the most affordable type to set up, since it’s written into your will. Do remember it only kicks in on death, so it does nothing if you lose mental capacity while you’re alive. For more on the will itself, see our guide to will writing in Singapore.

Living trust

A living trust is created and funded during your lifetime.

It gives you more control and flexibility than a will trust, and unlike a will trust it can keep working if you lose mental capacity. That flexibility costs more, both to set up and to run.

The next few types are really living trusts defined by what funds them.

Standalone insurance trust

Here a living trust is set up and then funded by nominating or assigning insurance policies into it, so a trustee manages the proceeds.

It’s handy when the rest of your estate planning is sorted and you simply want to keep this pot separate, while still controlling how the payout is distributed.

Property trust

A property trust is funded by placing property into it, often with the aim of holding it for children until they’re older.

As covered earlier, the ABSD changes have removed the old stamp-duty appeal, so the case for one now rests on control and timing. There are also practical catches, such as the property usually needing to be fully paid up, which makes professional advice important here.

Standby living trust

A standby trust is created small and left dormant, on standby. You set out the beneficiaries and the distribution plan in advance, but it’s barely funded.

What’s it standing by for? Mainly your death. Your will can be written to “pour over” assets into it when you pass away, at which point the trust springs to life and your instructions take over. And because it’s already a living trust, it can also help if you lose mental capacity, with the trustee stepping in to manage things, usually alongside a Lasting Power of Attorney. It tends to suit those who want the control and privacy of a living trust without funding it fully upfront.

How Much Does a Trust Cost?

Cost is the main reason a trust isn’t for everyone, and it varies widely with how complex your wishes are and who you appoint. Treat the figures below as rough guides as of 2026, not quotes.

A testamentary trust is the cheapest, because it’s simply written into your will. You’re mostly paying for the will itself.

A living trust costs more. Setting one up can run from a few thousand dollars into the tens of thousands, and there are usually ongoing fees on top, especially if you appoint a professional trust company to act as trustee. Those annual fees are often charged as a small percentage of the assets being managed.

The big exception is special-needs planning. The SNTC is a government-supported, non-profit trustee, and its fees are heavily subsidised by the Ministry of Social and Family Development. For families in that situation, it’s by far the most affordable option.

Because the numbers move with your situation and the provider, the only way to know your real cost is to get a quote from a trust company or estate planner.

Start With the Basics First

Before you think about a trust, make sure the foundations are in place. For most people, these cover the majority of what a trust would do, at little or no cost.

- A CPF nomination, so your CPF savings go to the people you choose without delay.

- An insurance policy nomination, so your policy payouts reach your loved ones directly.

- A will, so the rest of your estate is distributed the way you want, rather than by the default rules.

Once those are sorted, you’ll have a clear view of any gaps left over. That’s the point to ask whether a will trust or a living trust would genuinely add something, such as caring for a special-needs child, staggering gifts, or extra privacy.

How to Set Up a Trust in Singapore

The path depends on what you need.

The simplest is a trust nomination on an insurance policy. Your financial adviser can help you arrange it.

For anything more, a will trust or a living trust with a professional trustee, you’ll want to speak to an estate planner or lawyer. They can advise on the right structure, the costs, and how it fits with the rest of your plan.

The Bottom Line

A trust is a flexible tool, but it’s not a starting point, and it’s not for everyone. For most families, a CPF nomination, an insurance nomination, and a will are enough to do the job well.

It comes into its own in specific situations: caring for a vulnerable loved one, controlling when and how gifts are received, or keeping things private. If that sounds like you, it’s worth a proper conversation with a professional who can look at your full picture.

Trusts are one piece of the wider estate planning puzzle. Get the basics down first, and a trust becomes a much easier decision to make.

Not sure where you stand? Our FullCircle financial planning session walks through your protection, retirement, and estate planning together, so you can see what you actually need before spending on anything.

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.