What happens to everything you own if you pass away without a will?

It is not something most of us want to sit with. But if you never get round to writing a will, the decision is made for you. A law called the Intestate Succession Act steps in and splits your estate according to a fixed formula, no matter what you might have wanted.

The good news is the rules are not complicated, and once you understand them you can decide whether you are happy to leave things as they are or take a bit of control. Here is how it all works.

Too Long; Didn’t Read

- If you die without a valid will in Singapore, the Intestate Succession Act 1967 decides who inherits your estate, and in what shares.

- Your spouse and children come first. As a rough guide, a spouse with children gets half, and the children share the other half.

- The Act does not apply to Muslims, whose estates follow a separate set of rules.

- It also does not override a CPF nomination, an insurance nomination, or property you own jointly with someone else. Those go straight to the people you nominated or the joint owner.

- The fixed shares are not always the final word. A dependant left without reasonable support can ask the court to adjust things.

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

What Is the Intestate Succession Act?

When someone dies without a will, they are said to have died “intestate”. The Intestate Succession Act 1967 is the law that decides who then inherits, and how much each person gets.

You can also die intestate even with a will. If the will is found to be invalid, or it only deals with some of your assets, then anything left over falls under the Act. The law fills in the gaps you did not cover.

One thing to be clear on: the Act applies to non-Muslims. If you are Muslim, your estate is distributed under a separate set of inheritance rules known as faraid, so the table further down does not apply to you.

When the Rules Apply (and When They Don’t)

It is easy to assume the Act controls everything you leave behind. It doesn’t. A few of your biggest assets may pass to someone else entirely, before the Act gets a look in.

Here is what the Act does not control:

- CPF savings with a nomination. If you have made a CPF nomination, your CPF money goes to the people you named. Without one, your CPF is paid out according to the same intestacy rules, but handled by the Public Trustee rather than through your estate.

- Insurance payouts with a nomination. If you made an insurance nomination on a life policy, your beneficiaries receive the payout directly.

- Jointly owned property. A home held in joint names (joint tenancy) passes automatically to the surviving owner. It does not form part of your estate, so the Act does not touch it. Property held as “tenants-in-common” is different, as your share does fall into your estate.

- Assets in a trust. Anything you have placed in a trust is distributed under the terms of that trust.

What the Act does cover is everything else that is in your sole name, such as bank accounts, investments, and any property that is yours alone.

One more point for those with ties abroad. For movable assets like bank accounts and shares, the country you were legally settled in (your “domicile”) decides which inheritance law applies. But any property you own in Singapore is always governed by Singapore law, wherever you happened to live.

How Your Estate Is Divided

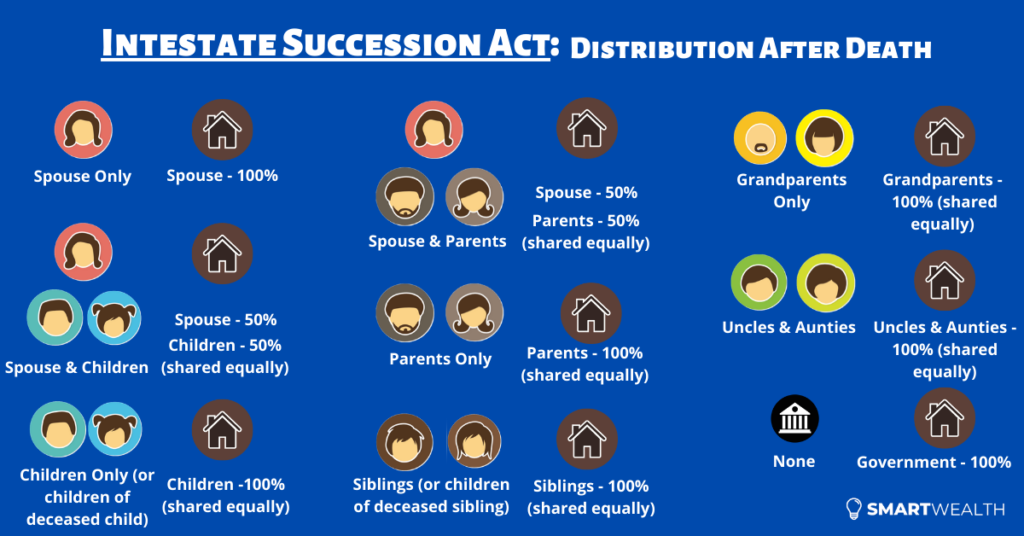

The law sets out nine rules for splitting an estate. They follow an order of priority, starting with the people closest to you. The table below sums them up.

| Who you leave behind | Who inherits, and how much |

|---|---|

| Spouse, no children, no parents | Spouse gets everything |

| Spouse and children | Spouse gets half. Children share the other half equally |

| Children, no spouse | Children share everything equally |

| Spouse and parents, no children | Spouse gets half. Parents share the other half equally |

| Parents, no spouse, no children | Parents share everything equally |

| Brothers and sisters (no spouse, children or parents) | Siblings share everything equally |

| Grandparents (none of the above) | Grandparents share everything equally |

| Uncles and aunts (none of the above) | Uncles and aunts share everything equally |

| No relatives at all | Everything goes to the government |

A few things worth knowing about how the shares work:

- Parents drop out once you have children. If you leave a spouse and children, your parents receive nothing, even if they are still alive.

- Grandchildren can step into their parent’s place. If one of your children has already passed away, that child’s own children (your grandchildren) split the share their parent would have received.

- The same applies to a sibling’s children. If a brother or sister has died, their children take that share between them.

Three quick examples

Say you are married with two children, and you pass away without a will. Your spouse receives half of your estate. Your two children split the remaining half, so a quarter each. Your parents, even if alive, receive nothing.

Now say you are married with no children, and both your parents are alive. Your spouse receives half, and your mother and father share the other half between them.

One more, to show how the order of priority works. Say you have no spouse and no children, but one parent is still alive along with two siblings. Your parent inherits everything. Your brothers and sisters receive nothing, because siblings only inherit when no parent survives.

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

Who Counts as Family Under the Act

The words “spouse” and “children” sound obvious, but the law is stricter than you might expect. This is where intestacy catches people out.

Your spouse has to be someone you are legally married to. A husband or wife you have separated from but not divorced still inherits. A former spouse you have divorced does not. And a partner you live with but never married has no claim at all, however long you were together.

Your children must be legitimate or legally adopted. An adopted child inherits from you exactly as a biological child would. Two groups miss out, though:

- Stepchildren you never legally adopted are not included.

- Children born outside marriage are not recognised under the Act unless they have been legitimated.

It is also worth knowing that adoption works in one direction only. Once a child is legally adopted, they inherit from their adoptive family, not from their birth parents.

If your closest relatives turn out to be brothers and sisters, there is one more wrinkle. Half-siblings, who share just one parent with you, rank just behind full siblings of the same closeness, rather than alongside them.

How the Estate Actually Gets Shared Out

Knowing who inherits is one thing. Someone still has to gather everything up and hand it out, and that part takes time.

When you die, your assets are effectively frozen. No one can touch your bank accounts or sell your property until the right person is given legal authority to act. Any debts, plus funeral and administration costs, are paid out of the estate first. Only what is left is divided up.

How your family gets that authority depends on the size of the estate.

For a smaller estate of $50,000 or less, your family can usually apply to the Public Trustee’s Office, which can administer it without going to court. The same office handles CPF money where no nomination was made. There is a small fee, charged on a sliding scale, taken out of the estate.

For a larger or more complicated estate, a family member has to apply to court to become the administrator. Once appointed, that person collects the assets, settles the debts, and distributes the rest according to the rules above. This route takes longer and usually means legal fees.

There is also a rare situation worth a mention. If two people die together, say a couple in the same accident, and it is unclear who died first, the law assumes the younger one outlived the older. That can change whose estate passes to whom.

The Fixed Shares Are Not Always Final

Most guides stop at the table, leaving the impression that the shares are set in stone. They usually are, but not always.

A close dependant who is left without enough to live on can ask the court to step in. Under a separate law, the Inheritance (Family Provision) Act, a spouse, a daughter who has not married or who cannot support herself, or a son under 21 or who cannot support himself, can apply for the distribution to be adjusted so they are properly provided for.

This is not automatic. The court only steps in where the standard split clearly leaves someone short, and the application has to be made within six months of the estate’s administration being granted. Still, it is worth knowing this option exists, in case the fixed shares leave a family member who depended on you without enough to get by.

Three Reasons Not to Leave It to the Law

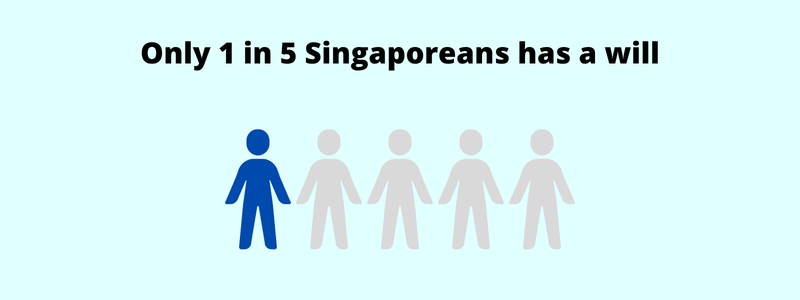

The rules are tidy on paper. In real life, letting them decide has some downsides. And this is the default for more people than you might think: barely 1 in 5 Singapore residents (just 22%) have a legally drafted will, going by the latest figures on wills and inheritance, so intestacy quietly decides where most estates end up.

It takes longer and costs more. Without a will naming someone to take charge, the court has to appoint an administrator first, and that can be slow. More paperwork and legal fees come out of the estate, and your family waits longer to get hold of what is theirs.

It can cause friction. Money has a way of straining even close families. When no one knows what you would have wanted, small disagreements can grow into lasting rifts at the worst possible time.

It may not reflect your wishes. The formula treats every family the same. It cannot know that you wanted to look after a long-term partner, a stepchild, or a good friend, none of whom inherit anything under the rules.

How to Stay in Control

The reassuring part is that avoiding all this does not take much. With a few simple steps, part of estate planning, you decide where your assets go instead of the law.

Four tools cover most people:

- Write a will. This is the main one. A will lets you say exactly who gets what, and name the person you trust to carry it out.

- Make a CPF nomination. Your CPF savings cannot be given away in a will, so a separate nomination is the only way to choose who receives them.

- Nominate beneficiaries on your insurance. A nomination on your life policies gets the payout to your loved ones quickly, without waiting on the legal process.

- Consider a trust. For more control over how and when your assets are passed on, setting up a trust gives you that flexibility.

You can keep track of all of this in one place through MyLegacy@LifeSG, the government portal for end-of-life planning. And none of it is permanent. As your life changes, you can update any of these arrangements.

The Bottom Line

Dying without a will does not mean your assets vanish or get lost. They are shared out, just on the law’s terms rather than yours, and not always in the way you would have hoped.

A short afternoon spent putting a few of these pieces in place spares your family the delay, the cost, and the uncertainty later on. It is one of the kinder things you can do for the people you leave behind.

If you would like help fitting these decisions into the bigger picture of your finances, we can walk you through it.

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.