Most of us spend far more energy thinking about life than about what happens after it.

But even if you’ve built up savings, bought insurance, and paid down the mortgage for the people you love, there’s one piece that often gets left on the to-do list.

The will.

Without it, you don’t get the final say on who receives what. The law decides for you, and it may not decide the way you’d want.

In this guide, we’ll cover what a will does, the requirements to make yours valid, what it costs, and the things it quietly can’t cover.

Too Long; Didn’t Read

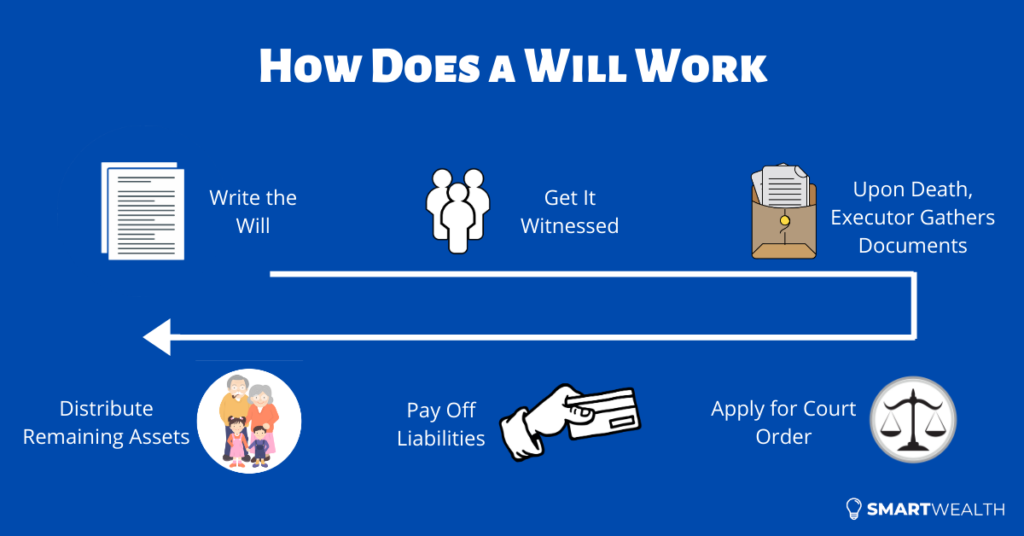

A will is a legal document that sets out how your assets are shared out after you die. You write it, sign it in front of two witnesses, and store it somewhere safe and findable.

When you pass away, the executor you named gathers your documents and applies to the court for a Grant of Probate. That’s the court order giving them the authority to act. Once granted, the executor settles your debts, then distributes what’s left according to your wishes.

Simple in theory. There’s more to get right than most people expect, so read on.

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

What Is a Will

A will is a legal document that spells out how your estate (everything you own) should be distributed after your death.

Its real value is control. You decide who inherits, how much they get, and on what terms. You can also name a guardian for your children and an executor to carry everything out.

In Singapore, wills are governed by the Wills Act.

A quick flag before we go on: if you hold assets in more than one country, it’s good practice to have a separate will for each. Estate laws differ across borders, and a single will can get tangled crossing them.

What Happens If You Die Without a Will

The usual question is whether you really need one. Single, married, kids or no kids, does it actually matter?

To answer that, it helps to compare dying without a will against dying with one.

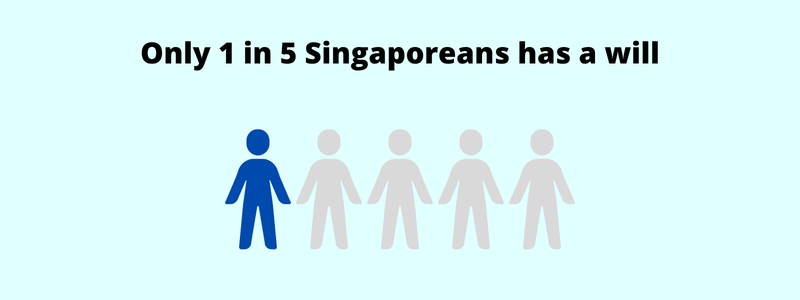

And most people don’t have one yet. Barely 1 in 5 Singapore residents (just 22%) have a will, as the latest figures show.

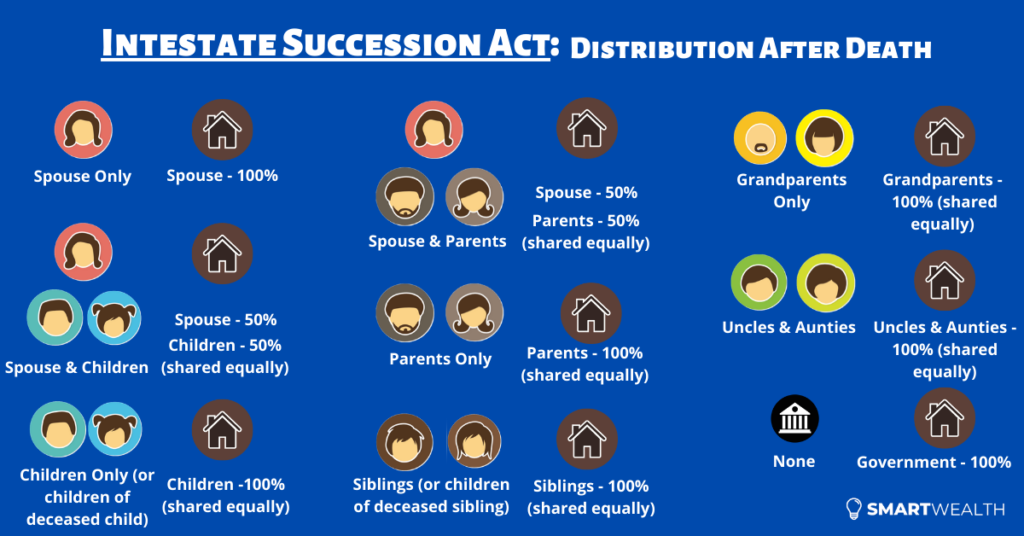

If you die without a valid will, you’re what the law calls “intestate”. Most of your assets are then shared out according to a fixed formula in the Intestate Succession Act. For Muslims, the rules under Muslim law and faraid apply instead.

Here’s the catch. Because you never put your wishes in writing, the formula decides everything. That can send assets to people you didn’t intend, while leaving out people you assumed would be looked after. An unmarried partner, for instance, receives nothing under the Act.

It usually costs more and takes longer too. Before anyone can touch the estate, someone has to apply to the court to be appointed administrator first.

A will removes most of that friction. And it does a fair bit more besides.

The Benefits of Having a Will

The headline benefit is control: you decide who receives what, and how much.

But a good will earns its keep in other ways:

- It spells out exactly who gets what, leaving less room for disputes among family members.

- It lets your beneficiaries receive their share faster.

- It lets you appoint a guardian for young children.

- It generally keeps costs lower than dying intestate.

- It lets you set up a trust to stagger payouts (say, a monthly sum, or a lump sum only once a child turns 25) instead of handing everything over at once.

In short, a will turns a default outcome you didn’t choose into a plan you did.

The Key People in a Will

A will brings together a handful of roles, and each one matters. Here’s who’s who.

Testator

The testator is simply the person making the will. That’s you.

To make a valid will, you need to be at least 21 years old and of sound mind.

Executor

After you’re gone, the executor is the most important figure of all.

This is the person you name to handle the admin: applying for the Grant of Probate, dealing with banks and other institutions, paying off debts, and distributing assets according to your wishes.

It’s not an easy job, so pick someone reliable. Bear in mind the person you name can also decline the role, so it’s wise to appoint a backup executor as well.

Your executor must be at least 21, of sound mind, and not an undischarged bankrupt. They can also be one of your beneficiaries, which is why spouses and adult children are common choices.

They hold a lot of authority, but they’re bound to act according to the will. Misusing estate money, for example, can amount to criminal breach of trust.

Trustee

The executor and the trustee can be the same person, but the roles differ.

The executor’s job is to carry out the instructions in the will. A trustee’s job is to manage the estate and make distributions to beneficiaries over time.

You might appoint a professional trust company as trustee if you want tighter control over how vulnerable beneficiaries, such as young children, receive their share.

Beneficiaries

Beneficiaries are the people or organisations you name to receive your assets. That can be a spouse, children, parents, a charity, or anyone else.

There’s no limit on how many you can have.

Witnesses

When you sign your will, two witnesses must watch you do it and then sign it themselves.

Those two witnesses must be at least 21, of sound mind, and crucially, they must not be beneficiaries or the spouses of beneficiaries. We’ll come back to why that matters in the next section.

Guardian

If you have young children, naming a guardian can be one of the most important things your will does.

It may not feel pressing if there’s a surviving spouse to step in. But if you’re a single parent, or if both parents were to die together, the question becomes urgent: who raises the children?

Name a guardian, and you decide. Leave it out, and the court appoints someone, who may not be the person you’d have chosen.

The Requirements for a Valid Will

Anyone can write their wishes on a piece of paper. Turning that paper into a will the court will honour takes a bit more.

Get the formalities wrong and your will can be invalid, or open to challenge later. According to MyLegacy@LifeSG, the Singapore government’s estate-planning portal, a valid will means you:

- are at least 21 years old

- are of sound mind

- made it voluntarily, without pressure from anyone

- put it in hardcopy, printed or handwritten on paper

- signed it in wet ink, at the end of the document, in front of two witnesses present at the same time

- had those same two witnesses sign it in your presence

A few of these trip people up, so they’re worth slowing down on.

Wet ink and hardcopy still matter. An oral will doesn’t count, and neither does a video or a will signed only on-screen. It has to be a physical document, signed by hand.

The two witnesses must be in the room together when you sign. You can’t sign in front of one today and the other tomorrow.

And your witnesses must not be beneficiaries, or married to a beneficiary. Here’s the part the rules don’t always spell out: if a beneficiary (or their spouse) does witness your will, the will stays valid, but the gift to that person is cancelled. So a well-meaning relative who signs as a witness can accidentally write themselves out of their own inheritance. Use independent witnesses, such as colleagues or neighbours, who don’t stand to gain anything.

What to Put in Your Will

Beyond the formalities, the substance of your will is about your assets, your debts, and who gets what.

Start with your debts. Spell out what you owe and how it should be settled, so your executor can simply follow your instructions rather than piece things together.

Then your assets. How specific you get is up to you. You might leave everything to two people in equal shares, or you might assign particular things to particular people, such as the flat to one child and the investments to another.

Two clauses catch a lot of home-made wills out, so don’t skip them.

The first is a residuary clause. This is the catch-all that says where “everything else” goes, anything you didn’t name specifically, or anything you acquire after writing the will. Without it, those leftover assets can fall into intestacy and be shared out by the legal formula, even though you have a will.

The second is naming backup beneficiaries. If someone you’ve named dies before you do, a line stating who inherits in their place keeps that share from defaulting to the law.

It also pays to keep an up-to-date list of your assets and debts alongside your will. It isn’t required, but it makes life far easier for your executor, who has to submit a list of everything you owned to the court. Without it, some assets can slip through the cracks entirely. Our FinSnap tool can help you keep that inventory in one place.

Don’t forget your digital life, either. Online logins, e-wallets, and crypto can be impossible for your family to reach if nobody knows they exist. Keep a separate, secure note of how to access them, and tell your executor. Don’t put passwords in the will itself, as it can become public once probate is granted.

What a Will Does Not Cover

Something many people don’t realise: a will doesn’t control everything you own. Several major assets pass outside it, by their own rules. Get this wrong and your will can quietly contradict where the money actually ends up.

These are the main ones to watch.

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

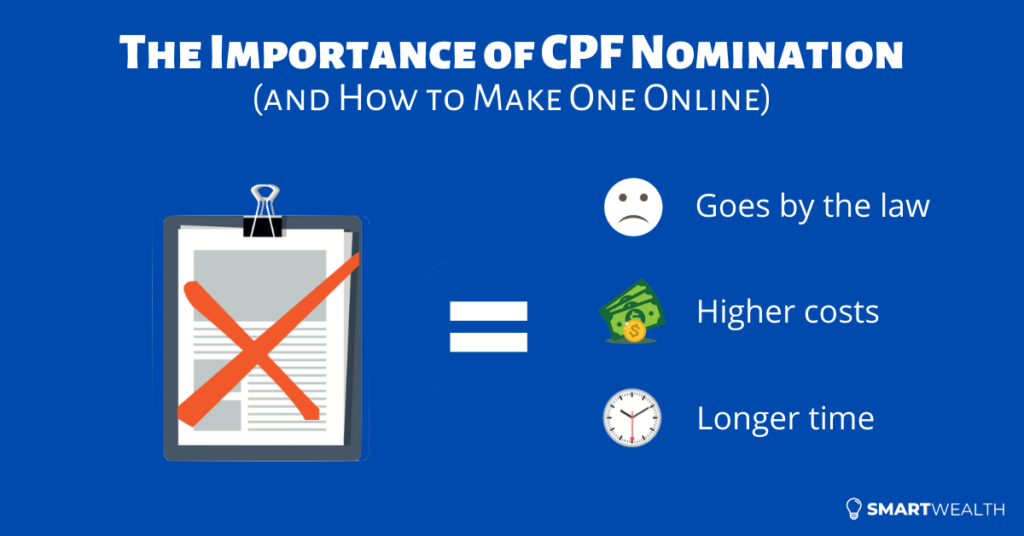

CPF savings

Your CPF money sits outside your will, full stop. That covers your Ordinary, Special, MediSave, and Retirement Accounts, plus any unused CPF LIFE premiums.

Instead, CPF is distributed by CPF nomination, a separate (and free) form you make with the CPF Board. Make one, and your CPF goes to the people you chose, paid out without waiting for probate.

Don’t make one, and your CPF is passed to the Public Trustee and shared out under the Intestate Succession Act (or Muslim law), which is slower and may not reflect your wishes.

Insurance payouts

For a policy with a death benefit, you can make an insurance nomination naming who receives the money.

Where a valid nomination exists, the insurer pays the nominees directly, without going through probate. That gets cash into your family’s hands quickly, which is often exactly what they need in the first few weeks.

There’s a trade-off, though. A nominated payout goes out as a full lump sum. So some people nominate just enough policies for quick liquidity, and leave the rest to the will, where payouts can be staggered through a trust.

Jointly owned property

How a jointly owned property passes depends on how it’s held.

Under a joint tenancy, the right of survivorship applies. If one owner dies, the other automatically takes full ownership, and the will has no say in it.

Under a tenancy-in-common, each owner holds a defined share (say 50/50 or 70/30). That share does form part of the estate, so it can be passed on through the will.

It’s worth checking which one applies to your home, because it decides whether your will controls the property at all.

Joint bank accounts

Money in a joint account usually passes straight to the surviving account holder rather than into the estate, though this can be challenged in some situations.

Assets held in trust

Anything you’ve placed in a trust generally sits outside your estate as well. The trust deed, not the will, governs how those assets are managed and distributed. That’s part of the appeal for people who want confidentiality, protection from creditors, or tighter control over how careful or vulnerable beneficiaries receive money.

Who Can Write Your Will, and What It Costs

Contrary to popular belief, you don’t need a lawyer to write a will. You can write one yourself.

Whoever writes it, it only becomes valid if it meets the requirements we covered earlier. Miss those, and it’s just a piece of paper.

You broadly have three routes, and the right one depends on how complex your estate is.

Do it yourself

Online templates and DIY will-writing tools can get a simple will done cheaply, sometimes for free. The government’s own MyLegacy@LifeSG portal has a free will learning tool that produces a Will Preparation Template you can work from.

This route works best for straightforward situations. The risk is that a poorly drafted will can be invalid or open to dispute, and you won’t be around to fix it.

A lawyer

A lawyer is often the first person people think of, though wills may not be every firm’s specialism.

Going through a law firm usually costs more than the other options, partly for the reassurance of the “drafted by a lawyer” stamp. For estates with property, business interests, foreign assets, or blended families, that expertise is well worth paying for.

A professional will-writing service

Because wills don’t have to be written by a lawyer, dedicated will-writing services often hit the sweet spot of affordability and expertise. Many are set up by lawyers or work alongside a law firm, so they can bring in heavier expertise when a case needs it.

They also tend to bundle the rest of estate planning, such as setting up an LPA or a trust, and can handle probate later. One point of contact for the lot is a real convenience.

What it costs in 2026

As a rough guide, this is what the market looks like. Treat the figures as indicative and confirm with the provider, since fees change.

| Route | Typical cost (2026) | Best for |

|---|---|---|

| DIY template or online tool | Free to around $250 | Simple, straightforward estates |

| Professional will-writing service | Around $250 to $500 for a basic will | Most people, an affordable middle ground |

| Lawyer (simple will) | Around $300 to $800 | Added legal advice and customisation |

| Lawyer (complex estate) | $1,500 to $5,000+ | Property, business, foreign assets, trusts |

| Mirror wills (a couple) | Around $400 to $1,500 for both | Couples leaving everything to each other |

Keep in mind there can be extra costs later, such as annual storage fees if a firm keeps your will, a charge to make changes, and the court fees for probate after you’re gone, which we’ll come to next.

After You’re Gone: The Probate Process

A will doesn’t take effect the moment you die. First, your executor has to apply to the court for a Grant of Probate, the order confirming the will is valid and giving them authority over your estate. Only then can they collect assets, settle debts, and distribute what’s left.

A few things to know, according to the Family Justice Courts:

- The application should be made within six months of the death.

- It usually takes around two to three months to come through.

- The main court filing fee is modest, around $240, with smaller charges on top.

A handy update since this guide first ran: a sole executor can now apply online through the courts’ Probate eService, instead of filing in person.

If there’s no will, it’s a different and slower route. Someone must apply for Letters of Administration instead, which we cover in our guide on dying without a will.

Where to Keep Your Will

Once your will is written and witnessed, it needs a home that’s both safe and findable. If it can’t be located when the time comes, it’s as good as lost.

A few sensible options:

- A fireproof safe at home, where it’s protected but still accessible.

- With your lawyer or will-writing service, many of which offer lifetime safekeeping in secure storage for a fee.

One place to avoid is a bank safe deposit box held in your sole name. The bank may not release the contents until probate is granted, which is the very thing your executor needs the will to start.

Wherever you keep it, tell your executor exactly where it is. You can also record its location with the Wills Registry, run by the Singapore Academy of Law. It doesn’t store the will itself, just a note of where it’s kept, which your family can search for later. A fee applies.

How to Update or Revoke a Will

A will isn’t a set-and-forget document. Life moves on, and your will should keep up.

It’s worth reviewing whenever something significant changes, for example:

- a beneficiary or your executor passes away

- a child or grandchild is born

- you acquire major assets

- you divorce

For small tweaks, you can add a codicil, a short supplement that updates the will. For anything substantial, it’s cleaner to write a new will and destroy the old copies. Either way, a codicil has to be signed and witnessed with the same formality as the original.

Two quirks catch people out. Getting married automatically revokes your existing will, unless that will was specifically made in contemplation of that marriage. Divorce, on the other hand, does not revoke your will, so an ex-spouse can stay a beneficiary unless you actively change it.

Creating a Testamentary Trust

A testamentary trust is a trust created through your will that only takes effect after you die. Instead of handing over a full inheritance at once, you set the terms: a monthly allowance, perhaps, or a lump sum released only when a child reaches a certain age.

It’s especially useful where beneficiaries are young, vulnerable, or not ready to manage a large sum. You can name a trust company as trustee to handle it, for a fee, rather than leaving the job to a family member.

If you want this kind of control while you’re still alive, a living trust is the other option worth exploring.

What’s Next

Whether your estate is simple or complex, a will is almost always worth having. A basic one is affordable, easy to change, and saves your loved ones a great deal of stress later.

It’s also just one piece of estate planning, the part of financial planning people most often put off until it’s too late. Alongside your will, the tools worth looking at are CPF nominations, insurance nominations, a Lasting Power of Attorney, and setting up a trust.

Sort them out together and you’ve done the hard part. What you’ve built ends up with the people you meant it for, and your family is spared a lot of stress at the worst possible time.

If you’d rather not piece it together alone, our FullCircle financial planning session looks at the whole picture with you, across protection, retirement, and estate planning, so you know what to prioritise and in what order.

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.