Dying is hard enough to think about. Dying without a will is the part almost no one plans for, mostly because you will never be the one left dealing with it.

But your family will. And the version of events where you left no instructions is slower, costlier, and more stressful for them than it needs to be.

This article is about what actually happens in that situation. Not just who inherits, but the real-world process your loved ones have to go through to unlock your assets: whose job it becomes, how long it takes, what happens to your CPF, HDB flat, and savings, and what it ends up costing them.

Too Long; Didn’t Read

- When you die without a will, you die “intestate”, and your assets are frozen until someone is given legal authority to deal with them.

- That someone is an administrator, usually your closest family member, who has to apply to court for a Grant of Letters of Administration before anything can be distributed.

- For a small estate of $50,000 or less, the family may be able to use the Public Trustee instead, with no court application needed.

- Some assets skip this process entirely: nominated CPF savings, nominated insurance payouts, and property held in joint tenancy go straight to the people you named or the surviving owner.

- Debts and funeral costs are paid first. Only what’s left is shared out, according to the Intestate Succession Act (or Muslim law).

- The whole thing takes longer and costs more than if you’d left a will. A few simple steps while you’re alive spare your family most of it.

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

What “Dying Without a Will” Actually Means

The legal term for dying without a will is dying “intestate”. If you leave a valid will, you die “testate”, and your wishes are followed.

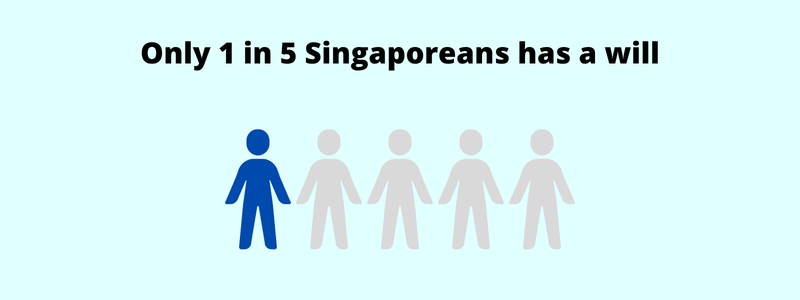

And this is the road most people are on. Only about a fifth of Singapore residents have made a will, roughly 22% at last count, going by recent estate planning data, so for the majority, the process below is the default.

There’s also a halfway version. If you have a will but it’s invalid, or it only deals with some of your assets, that’s partial intestacy. The parts your will covers are distributed as you wanted. Everything else falls to the law, as if you’d left no will at all for those assets.

One important point before we go further. If you’re Muslim, your estate is distributed under a separate set of inheritance rules known as faraid, not the Intestate Succession Act. The process side covered below, applying for authority to administer the estate, still broadly applies, but the shares each person receives are different.

The Moment You Die, Your Assets Are Frozen

Here’s the part that catches families off guard.

The instant you pass away, your assets are effectively frozen. Your bank accounts can’t be touched. Your property can’t be sold or transferred. Your shares, car, and other holdings sit untouched. No one, not even your spouse, has the automatic right to deal with any of it.

That stays the case until someone is given formal legal authority to step in. Until then, your family may be left covering funeral costs and daily expenses out of their own pockets, even though there may be plenty sitting in your accounts.

This is the single biggest reason a bit of planning matters. Not everything has to be frozen. As you’ll see, the assets you’ve nominated, like CPF and insurance, can reach your family quickly, while everything else waits for the legal process to run its course.

Someone Has to Take Charge: the Administrator

When there’s a will, the person named in it (the executor) handles everything. With no will, there’s no one appointed, so the court has to appoint someone instead. That person is called the administrator.

Being an administrator is a real job, and an unpaid one. They don’t get a bigger share for doing it. They simply take on the work of sorting out your entire estate on everyone’s behalf.

Who Can Apply to Be the Administrator

The right to apply follows roughly the same order as who inherits. The person with the largest entitlement to the estate has the highest priority, and for a non-Muslim estate the spouse usually comes first, according to the Singapore Courts.

Whoever applies has to be at least 21 and of sound mind. Someone lower down the order can still apply, but only by applying together with those who rank ahead of them, or after those people formally give up their right (a step called renunciation).

In practice, this is where friction can start. The “rightful” person may be too grief-stricken to take it on, so someone else steps up. Or one sibling wants to act and the others object. None of it is insurmountable, but it all takes time and goodwill at the worst possible moment.

What an Administrator Has to Do

Once appointed, the administrator is responsible for the whole estate from start to finish. The work usually includes:

- Tracking down all your assets and debts, and preparing a full list (the schedule of assets)

- Applying to court for the legal authority to act

- Opening an estate bank account to handle the money

- Settling funeral expenses, debts, and any taxes

- Distributing whatever is left to the right people in the right shares

This is far easier when you’ve kept a clear, up-to-date record of what you own and owe. Without one, your administrator may have to write to bank after bank just to find out where you held accounts. A simple list of what you own and owe saves them weeks of detective work.

When Two Administrators Are Needed

Usually one administrator is enough. But if any beneficiary is a minor (under 21), the court generally requires at least two administrators, and may ask for sureties (people who guarantee the estate is handled properly). Up to four can be appointed. Finding a second willing administrator and sureties is a common reason the process slows down.

The Two Routes to Getting Authority

How your family gets the legal authority to deal with your estate depends on how big and how complex it is. There are two routes.

The Public Trustee, for Smaller Estates

If your estate is worth $50,000 or less, your family may be able to ask the Public Trustee’s Office to administer it, with no need to go to court at all. The same office also handles CPF savings where no nomination was made. There’s a small fee taken from the estate, but it spares the family the court process. It’s only available if certain conditions are met, so it’s worth checking first.

The Grant of Letters of Administration, for Larger Estates

If the estate is worth more than $50,000, or is too complex for the Public Trustee, your family has to apply to court for a Grant of Letters of Administration. This is the court order that formally appoints the administrator and gives them control of your assets. They can apply on their own or through a lawyer, with the fees coming out of the estate.

This route takes several months, and your family may have little access to funds in the meantime. It’s where the contrast with having a will is sharpest. With a will, the equivalent step is a Grant of Probate, which is usually faster and cheaper because the court doesn’t first have to work out who should be in charge.

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

What Happens to Each of Your Assets

Not everything is treated the same way after death. Some assets pass to your family quickly and outside the whole process above. Others are stuck until the administrator has authority. Here’s how the main ones work when there’s no will.

CPF Savings

Your CPF money doesn’t form part of your estate, and it isn’t covered by a will even if you have one. What matters is whether you made a CPF nomination.

If you did, your CPF goes straight to the people you named, usually within weeks. If you didn’t, it’s passed to the Public Trustee, who distributes it according to the intestacy rules, which costs more and takes longer. Making a nomination is free and takes minutes, which is why it’s one of the first things we’d suggest.

Insurance Payouts

Life insurance works in a similar way. If you made an insurance nomination, the payout goes directly to your nominees without waiting on the legal process.

If you didn’t nominate, the insurer may release a limited sum to an immediate family member for urgent needs, but the rest is usually held until a grant is produced. Worth knowing: nominating isn’t always the right call for everyone. If your beneficiaries are young children or vulnerable, paying out a large sum directly to them can cause its own problems, which is where a will or trust can help structure things.

Bank Accounts

This depends on whether the account is joint or in your sole name.

For a joint account, the surviving account holder can usually access the balance once the bank is notified of the death. It’s not absolute and can sometimes be challenged, so it shouldn’t be your main plan for passing money on.

For an account in your sole name, the bank will freeze it. Nothing moves until the grant is shown, though some banks may, at their discretion, release a small balance to next-of-kin.

Property: HDB, Condo, or Landed

How your property passes depends on how it’s held.

If you own it in joint tenancy, your share passes automatically to the surviving co-owner, outside your estate and outside the Act. For most married couples, this is how the family home transfers without fuss.

If you own it as tenants-in-common, you each hold a defined share (say 50/50 or 70/30). Your share doesn’t pass to the co-owner. It falls into your estate and is distributed under the intestacy rules.

Other Assets

Anything else in your sole name, such as a car, shares, or investments, simply forms part of your estate. With no will, it’s all distributed according to the Intestate Succession Act once the administrator has authority and the debts are paid.

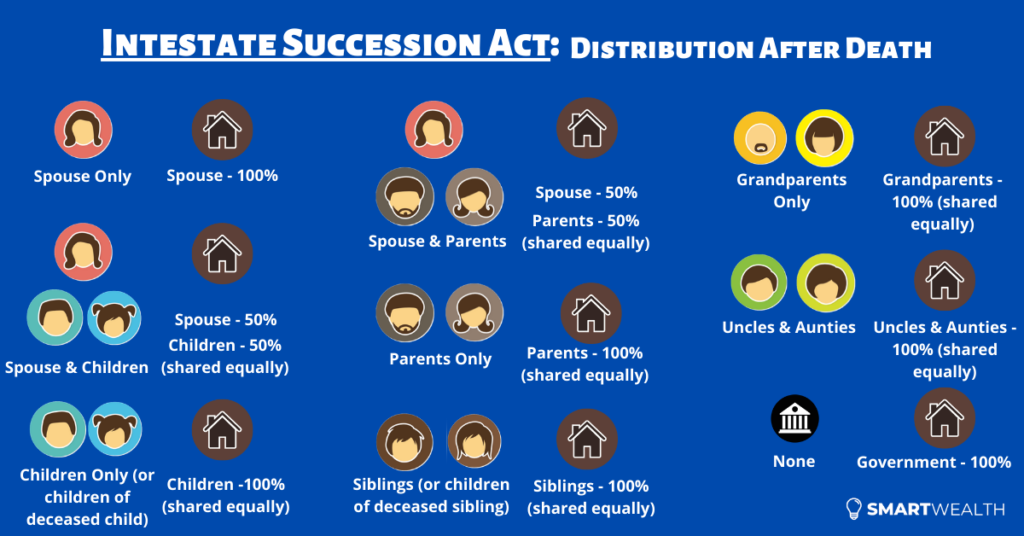

How What’s Left Is Finally Divided

Once the debts, funeral costs, and administration expenses are paid, whatever remains is shared out according to a fixed formula in the law. For non-Muslims that’s the Intestate Succession Act, and for Muslims it’s faraid.

The broad strokes: your spouse and children come first. As a rough guide, a spouse with children takes half, and the children share the other half. If there’s no spouse or children, the estate moves outward to parents, then siblings, and so on. If no relatives can be found at all, it goes to the government.

The exact shares for every family situation, who counts as a “child” or “spouse”, and the scenarios where the fixed split can even be challenged in court, are all set out in our full breakdown of who inherits and how much. The key takeaway here is simpler: the law decides, not you.

Three Less Obvious Situations Worth Knowing

Beyond the standard process, three situations come up often enough to be worth knowing, and most guides skip them.

Debts are paid before anyone inherits. Your loans, credit card balances, taxes, and funeral costs don’t vanish when you die. They’re settled out of the estate first, and only the remainder is distributed. Your family doesn’t personally inherit your debts, with one common exception: a jointly held mortgage, where the surviving co-owner takes on the loan. This is exactly what mortgage or term insurance is for.

A foreign beneficiary inheriting residential property faces a deadline. If someone entitled to your estate is a foreigner or Singapore PR, and they stand to inherit residential property such as a landed home, that interest must be sold or transferred within five years of your death, unless approval is obtained from the authorities. It’s a real trap for mixed-nationality families, and rarely flagged anywhere.

If a couple dies together, age decides the order. Where two people die in circumstances making it unclear who passed first, such as the same accident, the law presumes the younger person outlived the older. That assumption can change whose estate flows to whom, and it’s one more outcome you can’t control without a will.

What It Really Costs Your Family

None of this is a disaster on its own. Added together, though, it’s a heavier load than most people would want to leave behind.

It costs time. With no will naming someone to act, the court has to appoint an administrator before anything moves. Sorting out who that is, tracking down the assets, and getting the grant can stretch on for months, all while the estate sits frozen.

It costs money. More paperwork and legal fees come out of the estate, leaving less for the people you wanted to provide for.

And it can cost relationships. When no one knows what you would have wanted, money has a way of turning small disagreements into lasting rifts, just when a family can least bear it. The law treats every family by the same formula. It can’t know that you wanted to look after a long-term partner, a stepchild, or a close friend, none of whom inherit a cent under the rules.

How to Avoid All of This

The reassuring part is that sidestepping all this doesn’t take much. A few straightforward steps, part of basic estate planning, put you back in control.

- Write a will. This is the main one. A will lets you say who gets what, name the person you trust to carry it out, and appoint a guardian for young children.

- Make a CPF nomination. Your CPF can’t be left in a will, so a separate nomination is the only way to choose who receives it, and to get it to them quickly.

- Nominate on your insurance. A nomination on your life policies gets the payout to your loved ones without the wait.

- Consider a trust. For more control over how and when assets pass on, especially for young or vulnerable beneficiaries, setting up a trust gives you that flexibility.

None of it is permanent, and you can update any of it as life changes.

The Bottom Line

Dying without a will doesn’t mean your assets disappear. It means your family inherits the slow, expensive version of the process, and the people who end up with your estate are picked by a formula rather than by you.

An afternoon spent putting a few of these pieces in place spares them most of that.

If you’d like help fitting these decisions into the bigger picture of your finances, we can walk you through it.

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.