If your income stopped tomorrow, how long could your family keep up with the mortgage, the school fees, and the everyday bills?

For most households in Singapore, the honest answer is measured in months, not years.

The Life Insurance Association’s latest Protection Gap Study found that working adults here face a S$373 billion mortality protection gap and a S$579 billion critical illness protection gap, as of 2022. In percentage terms, 21% of what families would need after a death, and 74% of what they’d need after a critical illness, simply isn’t there.

This guide walks through the planning process in order: what you already have through national schemes, where that cover falls short, what closes each gap, how much you actually need, and what to buy first.

Key statistics at a glance:

- The average working adult holds life cover of about 3.6 times annual income, well short of the roughly 9 times LIA suggests

- Average critical illness cover is about 2.1 times annual income, versus the roughly 4 times recommended

- The average critical illness claim payout is only $52,343, while late-stage cancer treatment can cost $100,000 to $200,000 a year

- From 2026, CareShield Life pays $689 a month for severe disability, against nursing home costs of around $4,900 a month before subsidies

- About 69% of Singapore residents hold an Integrated Shield Plan on top of MediShield Life, as of 2026

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

What Is Insurance Planning (& Why It Comes Before Investing)

Insurance planning is the process of identifying the financial risks that could derail your life (death, illness, disability, losing your home), checking what cover you already have, and closing the gaps in a sensible order and at a sensible cost.

It comes before investing for one simple reason: your income funds every other goal. The retirement portfolio, the children’s education fund, the property upgrade, all of it assumes you keep earning. Insurance is what keeps those plans alive when you can’t.

Picture a total permanent disability at 40. The salary stops, but the mortgage, school fees, and daily expenses don’t. Savings start draining from day one, right when medical and care costs are climbing. Without cover, everything you were building gets used up covering daily costs.

Insurance is the base of a financial plan. It protects everything you build on top of it.

The good news is that in this day and age in Singapore, you don’t start from zero. Every citizen and Permanent Resident already has a base layer of cover through national schemes. So that’s where the planning starts: knowing what you already have.

What You Already Have: Singapore’s National Schemes

Singapore’s national insurance schemes form the compulsory base layer of your protection. Some of them you were enrolled in automatically.

A quick note for non-citizens: these schemes cover Singapore citizens and PRs only. If you’re a foreigner working here, you’ll need private cover for all of the risks below.

MediShield Life

MediShield Life is the compulsory national health insurance scheme, covering all citizens and PRs for life, regardless of age or pre-existing conditions. It’s designed to cover large hospital bills at the subsidised B2 or C ward level in public hospitals.

The scheme was upgraded in its 2024 review, with changes rolling out from April 2025. Claim limits rose across the board so that the scheme once again fully covers nine in ten subsidised bills, and coverage extended to newer treatments and more outpatient care, per the Ministry of Health.

The trade-off: with healthcare costs still climbing, premiums are rising by an average of 22% per policyholder, phased in between April 2025 and March 2028, and deductibles are increasing too, which keeps the scheme focused on larger bills.

The key thing to understand: MediShield Life is sized for subsidised public hospital care. If you’re treated in a B1 or A class ward, or a private hospital, the payout is pro-rated downwards and covers only a small fraction of the bill.

CareShield Life and ElderShield

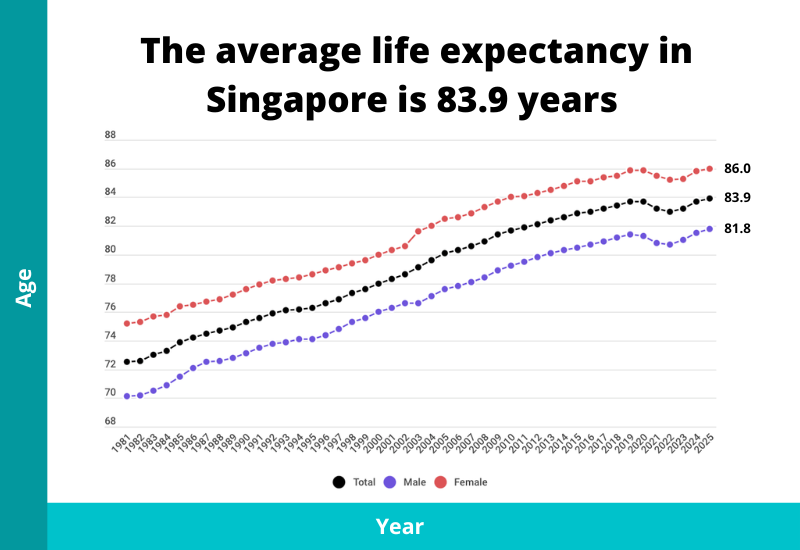

CareShield Life is the national long-term care insurance scheme. It pays a monthly cash benefit for life if you become severely disabled, defined as being unable to perform at least three of six activities of daily living, such as washing, dressing, or feeding yourself. With life expectancy in Singapore at 83.9 years, more of us will spend part of our later years needing some form of care.

It’s compulsory for citizens and PRs born in 1980 or later, and optional for older cohorts. Premiums are payable entirely from MediSave until age 67.

Payouts got better in the 2025 review. From January 2026, they grow at 4% a year instead of 2%, so a claim made in 2026 pays $689 a month, rising to $806 a month for claims made in 2030, according to MOH’s announcement. Your eligible payout keeps growing each year until you turn 67 or make a claim, whichever comes first.

ElderShield is the older, now-closed predecessor scheme, which paid a fixed $300 or $400 a month for up to five or six years. If you were born in 1979 or earlier, it’s worth understanding how CareShield Life works, how it compares with ElderShield, and whether upgrading makes sense.

Dependants’ Protection Scheme

The Dependants’ Protection Scheme is a basic term life policy that most working citizens and PRs are automatically enrolled in when their first CPF working contribution is made, between the ages of 21 and 65.

DPS pays out $70,000 if you die, suffer total permanent disability, or are diagnosed with a terminal illness before age 60. From 60 to 65, the sum assured drops to $55,000, and cover ends at 65. The scheme is administered solely by Great Eastern, and the age-banded annual premiums are deducted from your CPF Ordinary or Special Account, per the CPF Board.

Is $70,000 meaningful? Yes. Is it enough to replace a breadwinner’s income for a family with young children? Not remotely, and we’ll put numbers on that shortly.

Home Protection Scheme

The Home Protection Scheme is mortgage-reducing term insurance for HDB flat owners who use CPF savings to service their housing loan. If you die or suffer total permanent disability or terminal illness before age 65, HPS pays off the outstanding loan (up to your insured share), so your family keeps the flat.

HPS is compulsory for HDB owners paying with CPF, unless you obtain an exemption by showing you have adequate private cover, such as a mortgage insurance policy or term insurance of your own. It insures you until age 65 or until the loan is paid up, whichever is earlier. Note what it doesn’t do: HPS doesn’t cover private property, and it pays the bank, not your family’s living expenses.

The Protection Gap: What National Schemes Don’t Cover

The national schemes are a good base. The problem is the distance between what they pay and what things actually cost.

Here’s how the national schemes compare against real, current cost data for the risks they do cover:

| The event | What the national scheme pays | What it can actually cost |

|---|---|---|

| Hospitalisation (e.g. knee replacement) | MediShield Life, sized for C/B2 wards (payouts pro-rated sharply for private care) | Median $6,993 in a public C ward vs $48,746 in a private hospital (MOH bill data) |

| Critical illness | Nothing. No national scheme pays out on diagnosis | Late-stage cancer treatment can run $100,000 to $200,000 a year |

| Severe disability | CareShield Life: $689 a month for claims in 2026 | Around $4,900 a month for a higher-care nursing home before subsidies, or about $2,700 a month for care at home (MOH) |

| Death of a breadwinner | DPS: $70,000 before age 60 | Roughly nine times annual income under LIA guidance. For someone earning $5,000 a month, that’s about $540,000 |

The critical illness row deserves a second look. There is no national scheme that pays you a lump sum when you’re diagnosed with cancer, suffer a heart attack, or have a stroke. Whatever cover you hold privately is all there is.

The catch is that most people simply hold less of it than they need. SmartWealth’s analysis of 36 months of published insurer claims data found an average critical illness claim payout of just $52,343. The full breakdown is in our study of average claim payouts. For someone earning $5,000 a month, that wouldn’t replace even one year of lost income. LIA’s recommended CI cover of around four times annual income exists precisely because recovery typically takes years, not months.

The odds aren’t comfortable either: roughly 1 in 4 Singaporeans may develop a critical illness in their lifetime, with cancer accounting for 73% of CI claims.

The disability numbers are hard to ignore too. CareShield Life pays $689 a month, while a higher-care nursing home costs around $4,900 a month before subsidies. Subsidies cover a large part of that for lower- and middle-income households, but the rest still has to come from somewhere.

None of this means the national schemes have failed. They were designed to be a floor, and the gap between the floor and your family’s actual needs is what private insurance exists to cover.

The rest of this guide is about closing these gaps: the cover that does each job, how much of it you need, and the order to buy it in.

The Core Cover: Protecting Your Income & Life

These are the policies that replace your income when death, disability, or serious illness takes it away. In my opinion, they matter more than everything else in this guide combined.

Term life insurance

Term life insurance covers you for a fixed period, say until age 65, and pays a lump sum if you die or suffer total permanent disability during that time. There’s no savings component, which is exactly why it’s the most affordable way to buy a large amount of cover.

For most working adults with dependants, term life provides most of the cover. A healthy 35-year-old can typically secure $1 million of cover for a modest monthly premium. Most term plans also let you attach riders, such as critical illness or early CI cover, so one policy can carry several layers of protection. If you’re weighing up providers, you can compare term life plans here.

Whole life insurance

Whole life insurance covers you for life and builds cash value over time, which you can access by surrendering the policy. Premiums are substantially higher than term for the same coverage, because part of what you pay is being invested.

Whether whole life is worth the extra cost depends on your situation. It suits people who want guaranteed lifelong cover or a forced-savings discipline. It’s less suitable when the higher premium leaves too little for adequate cover elsewhere. The term vs whole life question deserves its own read, and if you land on the whole life side, here’s our whole life comparison.

Critical illness cover

Critical illness cover pays a lump sum on diagnosis of a covered condition, such as cancer, heart attack, or stroke. Unlike hospitalisation insurance, which pays the hospital, a CI payout is yours to use however you need: replacing income during recovery, paying for treatments not covered elsewhere, or hiring help at home.

Standard CI plans pay out at the later stages of an illness. Early CI plans cost more but pay out at earlier stages, when treatment has the best odds and income disruption starts. Given that cancer is caught earlier and survived more often than ever, early-stage cover has become the more relevant choice.

There’s also a treatment funding gap that CI plans quietly fill. MediShield Life and Integrated Shield Plans pay for outpatient cancer drug treatments within Cancer Drug List limits, and there are monthly caps even for drugs on the list. If your prescribed drug sits outside the list or beyond the caps, a CI lump sum is one of the few resources that can pay for it. Here’s our early CI comparison if you’re exploring options.

Disability income insurance

Disability income insurance pays a monthly benefit, typically up to 75% of your salary, if illness or injury leaves you unable to work in your occupation. It keeps paying until you recover, return to work, or reach the policy’s end age.

It’s one of the least talked about covers in Singapore, with only a handful of insurers offering standalone plans. That’s a pity, because it protects against a scenario the other policies handle poorly: being too unwell to work for years without ever meeting the strict definition of total permanent disability.

The claim definition matters more here than anywhere else. Some plans pay when you can’t perform your own occupation, which makes them especially valuable for specialised professionals. Think of a surgeon whose hand injury ends surgical work, even though desk work remains possible. Other plans only pay if you can’t do any occupation suited to your training, a much higher bar. Check which definition you’re buying.

Health & Long-Term Care Cover

MediShield Life and CareShield Life give you the base. This layer is about topping both up.

Integrated Shield Plans

An Integrated Shield Plan (IP) is private health insurance built on top of MediShield Life, extending your cover to B1 or A class wards in public hospitals, or to private hospitals. Seven insurers offer IPs, and about 69% of residents hold one, as of 2026.

IPs come in two parts: the main plan, payable with MediSave up to Additional Withdrawal Limits, and optional riders paid in cash that reduce your out-of-pocket share. Rider rules changed in late 2025: riders sold from April 2026 no longer cover the deductible, and the annual co-payment cap doubled to $6,000, though premiums for the new riders are expected to be around 30% lower. Our guide to Integrated Shield Plans explains how the plans are structured.

In my opinion, a hospitalisation plan sized to the ward class you’d actually choose is the single most important private policy you can hold. A large hospital bill is the fastest way to undo years of savings.

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

CareShield supplements

CareShield Life’s monthly payout is a floor, not a care budget. CareShield supplements are private plans that increase the monthly disability payout, and some may pay out at lower disability thresholds, though terms vary from plan to plan. Premiums can be paid partly with MediSave, up to $600 per year.

Cover if you have pre-existing conditions

A diagnosis doesn’t automatically shut you out of insurance. MediShield Life and CareShield Life cover pre-existing conditions by design, and depending on the condition, some private insurers may still offer cover, sometimes with exclusions, extra premiums, or waiting periods. Our guide on insurance for pre-existing conditions covers the options.

Protecting Your Home & Family Milestones

Beyond your income and health, two of the biggest financial commitments you’ll ever take on are a home and a child. Both have cover built for them. Insurance is only one part of planning for a home, though. Our guide to property planning covers the rest, from buying to passing it on.

Mortgage insurance (vs HPS)

Mortgage insurance pays off your outstanding home loan if you die or become totally and permanently disabled. For HDB owners, HPS already does this, though as covered earlier, adequate private cover of your own can exempt you from HPS altogether.

The private version matters in two cases: you own private property (where HPS doesn’t apply), or you want features HPS doesn’t offer, such as level cover, portability (the policy follows you rather than being tied to one property), or cover beyond age 65.

Private plans are frequently more affordable than people expect, and for some people they beat HPS on both price and flexibility. Our mortgage insurance comparison walks through when switching makes sense.

Maternity insurance

Maternity insurance covers pregnancy complications, congenital conditions in the newborn, and usually hospital care for both mother and child. It’s bought during pregnancy, with each insurer setting its own eligibility window. Some plans also let you lock in the child’s future insurability, including guaranteed acceptance for selected plans such as an Integrated Shield Plan, regardless of conditions discovered at birth. That last feature is, in my opinion, the most underrated reason to consider it. Here are the maternity insurance options currently on the market.

Home and fire insurance

Fire insurance covers the building structure, and it’s compulsory if you’re servicing an HDB loan. Home insurance goes further, covering renovations, contents, and personal liability. The two are often confused, and the difference matters: HDB fire insurance alone won’t replace your furniture, your renovation, or anything you own inside the flat.

Insurance That Builds Wealth (A Brief Map)

Some insurance products are less about protection and more about accumulation. They can play a role in a plan, but they should never come before the protection layers above. A brief, honest map:

Endowment savings plans

Endowment plans combine a small insurance element with disciplined saving towards a fixed date, such as a child’s university enrolment, often as part of a wider child education plan. Returns are typically modest, part guaranteed and part not, and surrendering early usually means losses. They suit savers who value certainty and discipline over maximum returns.

Retirement annuities

Retirement annuity plans convert a lump sum or years of premiums into a stream of income later in life, supplementing CPF LIFE as part of your broader retirement planning. Some can be funded with SRS money, which adds a tax angle worth understanding, and we’ve covered funding one with SRS separately.

Legacy insurance

A cluster of products exists mainly to pass wealth on: term insurance till 99, legacy whole life plans, universal life (including the newer indexed universal life), and lifetime income plans. We’ve covered all of them in our guide to legacy planning with insurance. These are estate tools as much as insurance, and they work best as part of a deliberate estate planning strategy rather than as standalone purchases.

Everything Else: General Insurance in Two Minutes

For completeness, the covers that protect things rather than income.

Car insurance is required by law before you can drive.

If you employ a helper, you’re required to buy both medical and personal accident insurance for her, with minimums set by MOM.

Personal accident insurance for yourself pays for injuries, medical expenses, and accidental death, and is worth a look for those in physical jobs or with active lifestyles.

Travel insurance is optional but inexpensive relative to the medical evacuation bills it can cover.

And if you’re serving NS or are MINDEF/MHA-linked personnel, the group insurance available to you is worth considering.

How Much Coverage Do You Need?

As a starting point, LIA suggests cover of roughly 9 times your annual income for death and total permanent disability, and roughly 4 times your annual income for critical illness.

Most people are far from those marks. The average policyholder’s mortality cover works out to about 3.6 times annual income, and CI cover about 2.1 times, per the Protection Gap Study 2022.

Here’s what the multiples look like in practice. Sarah is 35, married with a young son, and earns $6,000 a month, or $72,000 a year:

- Death and TPD cover: 9 x $72,000 = $648,000

- Critical illness cover: 4 x $72,000 = $288,000

She wouldn’t be starting from zero. DPS gives her $70,000, HPS covers her share of the flat, and her employer provides some group cover.

But group cover doesn’t follow you. If Sarah leaves the job, the cover ends with it. And if she developed a health condition while employed, she may find new cover hard to get at exactly the moment she needs it most. Her own term and CI policies, each sized to close its own gap, don’t carry that risk.

Rules of thumb only get you started. Your number moves with your debts, your dependants, and your existing assets. The cover also has to fit your budget: settle on premiums you’re comfortable paying, and it’s perfectly fine to carry a shortfall knowingly, as long as you understand the risk you’re keeping. Our life insurance calculator lets you work through your own figures.

In What Order Should You Buy? (A Priority List on a Budget)

If the budget only stretches so far, buy in this order: hospitalisation first, then income protection, then critical illness, then everything else.

- Hospitalisation cover. Decide whether MediShield Life alone is enough or whether you want an IP for higher ward classes. One large hospital bill can wipe out years of savings, so this comes first.

- Death and TPD cover. Term life sized to your income and dependants. This is affordable protection for the largest financial risk your family faces.

- Critical illness cover. The base layer here is zero, and a serious diagnosis both raises your expenses and stops your income. Early CI if the budget allows, standard CI if not.

- Disability income. Fills the long-recovery gap the others miss.

- The rest. Mortgage cover top-ups, maternity, personal accident, and the accumulation products, once the four layers above are solid.

On budget: the MoneySense Basic Financial Planning Guide suggests spending at most 15% of your income on insurance protection, alongside investing at least 10% for the future. In my opinion, most families can secure all four core layers well within that 15%, provided they lean on term rather than whole-of-life products for the big sums.

If you’re wondering whether the risks justify the premiums at your age, the probability of death within one year at each age is sobering but useful context.

One caveat that applies to everything above: private insurance applications are subject to underwriting and full health disclosure. Cover is cheapest and easiest to get when you’re healthy, which is itself an argument for not waiting. That’s the paradox of insurance: the moment you need it most is often the moment you can no longer buy it.

Common Insurance Planning Mistakes

Buying accumulation before protection. The classic error: a savings plan bought before hospitalisation and life cover are properly in place. Protection first, always.

Duplicate cover. You can’t hold two Integrated Shield Plans, but overlap still happens, most commonly between your IP and the group medical cover your employer provides. The same bill can’t be paid twice, so know what your group plan covers before adding more.

Lapsing policies mid-life. Money gets tight and the term policy gets cut, usually in the policyholder’s 40s or 50s, exactly when claims become more likely. If affordability is the issue, reducing the sum assured beats cancelling outright.

Ignoring underwriting and disclosure. The claim rejection stories that make the news are very often non-disclosure cases. Declare everything, even what seems minor, and let the insurer decide what matters. And if the insurer postpones your application, adds exclusions, or rejects you outright, that’s fine. It’s the reality of where you stand, and only when you know it can you plan around it properly.

Your Insurance Planning Checklist

Work through this in order:

- List what you already have: MediShield Life, CareShield Life or ElderShield, DPS, HPS, plus any group cover from work and existing private policies. An insurance policy summary puts all of this on one page.

- Decide your hospitalisation level: MediShield Life alone, or an IP for the ward class you’d genuinely choose.

- Calculate your death/TPD and CI numbers using the LIA multiples as a starting point.

- Close the biggest gap first, usually with term life, then CI.

- Check the household, not just yourself: a non-working spouse’s illness has financial consequences too.

- Review at every life event: marriage, each child, a property purchase, a job change.

- Keep your beneficiaries and insurance policy nominations up to date.

A Final Word

Insurance planning in Singapore comes down to knowing what the national schemes already give you, seeing where they stop, and closing the gaps that would hurt your family most, at a cost that leaves room for everything else you’re building.

You don’t need to solve it all in one sitting. Start with the checklist above, fix the biggest gap first, and build from there. And if you’d rather not work through it alone, you can compare your options, or have insurance looked at alongside everything else you’re building through comprehensive financial planning.

For you and your loved ones, it might be the most valuable afternoon of admin you’ll ever do.

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.