Thinking of buying an HDB flat? Chances are, someone has mentioned the Home Protection Scheme (HPS) to you.

If this is your first time purchasing a home, things are about to get serious.

Your finances need to be in order, and you might be wondering: is HPS the best option for you? What are its limitations? Are there better alternatives out there?

Let’s go through everything you need to know.

- What Is the Home Protection Scheme (HPS)?

- What Is It Not?

- Is the Home Protection Scheme Compulsory?

- What Exactly Does the Home Protection Scheme Cover?

- How Should You Allocate HPS Coverage?

- Paying the Premiums for HPS

- How Much Are HPS Premiums?

- How to Get an Exemption From HPS?

- The 5 Limitations of HPS

- Are There Better Alternatives?

What Is the Home Protection Scheme (HPS)?

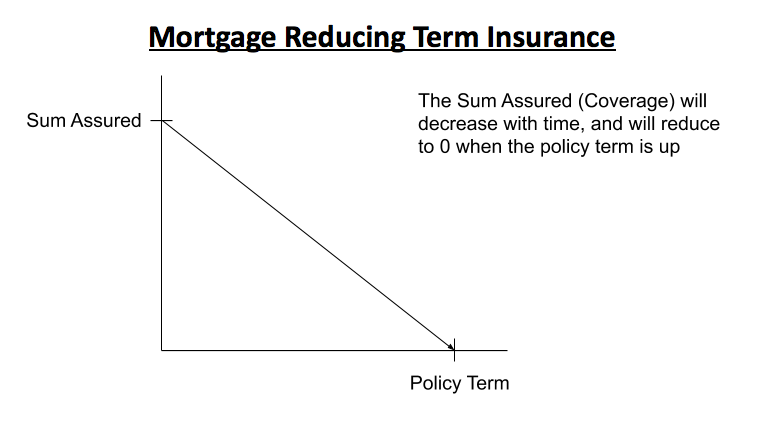

The Home Protection Scheme (HPS) is a mortgage-reducing term insurance managed by the Central Provident Fund Board (CPFB).

Its main goal is to safeguard HDB homeowners against unforeseen circumstances that might leave them unable to repay their housing loans.

But what exactly is mortgage-reducing term insurance?

Let me paint you a clearer picture:

As you make your monthly HDB loan payments, the outstanding loan amount falls over time.

If something unexpected happens to you or your co-owner, HPS can step in to cover part or even the entire remaining loan with its payout.

That way, your co-owner isn’t left shouldering the whole loan on their own if you’re no longer around.

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

What Is It Not?

As a new homeowner, it’s important to understand other types of insurance often confused with HPS:

Dependants’ Protection Scheme (DPS)

DPS pays out up to $70,000 in the event of death, terminal illness, or total and permanent disability, reducing to $55,000 between ages 60 and 65, when coverage ends. It’s designed to tide your dependants over, but the sum is typically insufficient for housing loans, which is what sets it apart from HPS.

Home and Fire Insurance

Fire insurance, mandatory for HDB loans, covers reinstating internal structures and fixtures provided by HDB but excludes home contents. Optional home insurance offers more comprehensive coverage, including renovations, furniture, and personal belongings. These policies are generally more affordable than HPS and serve a different purpose.

Is the Home Protection Scheme Compulsory?

If you’re using your CPF savings, partially or fully, to pay for your monthly HDB (BTO or resale) or DBSS flat repayments, you’re required to be covered under the HPS.

This applies regardless of whether your mortgage loan is from HDB itself or from a bank like DBS, OCBC, UOB, or others.

That said, there are exceptions:

- If you have private insurance that meets the necessary criteria (more on this later, as it could be a worthwhile alternative), you can apply for an exemption from HPS.

- If you’re repaying your HDB loan entirely with cash, HPS becomes optional.

- If you’re living in private residential property (condominiums or landed houses), Executive Condominiums (ECs), or privatised Housing and Urban Development Company (HUDC) flats, HPS is not required.

For those in the second or third category, it may be wise to consider private mortgage insurance or level term insurance offered by insurers to ensure comprehensive protection.

What Exactly Does the Home Protection Scheme Cover?

The HPS provides coverage for:

- Death

- Terminal illness

- Total and permanent disability

HPS coverage lasts until you reach the age of 65 or until your HDB loan is fully repaid, whichever comes first.

Like all insurance, your health will be subject to underwriting.

You’ll need to fully disclose any relevant health information, and you may be required to undergo a medical examination. The CPF Board may also request a medical report from your doctor to assess your eligibility for HPS.

As with most insurance policies, there may be exclusions, such as pre-existing conditions not being covered.

The worst-case scenario is that your application for HPS is rejected.

If you are rejected, you may still be able to secure coverage through private insurance. It’s a good idea to consult a qualified professional who can guide you towards an alternative solution.

How Should You Allocate HPS Coverage?

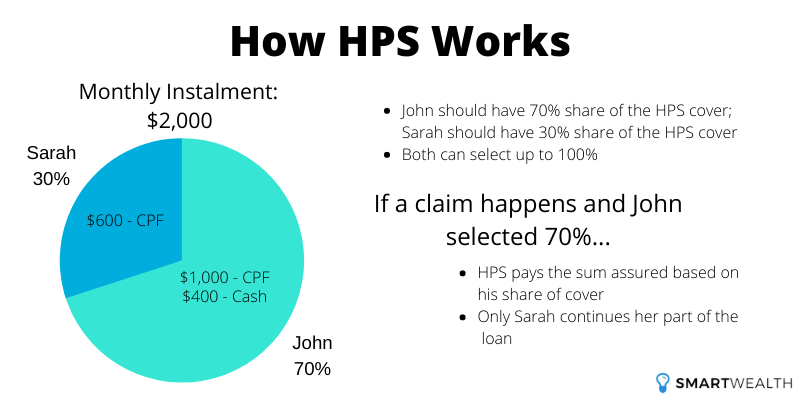

Here’s what the CPF Board says:

Your share of the HPS cover should at least match the proportion of the monthly housing instalment which is payable with your CPF savings and/or cash. The total share of cover per household should add up to at least 100%.

Also, you and your co-owner(s) can each choose to insure for a higher share of cover, for up to 100% per owner. In the event of a claim, HPS will settle the outstanding housing loan up to the insured sum, based on the share of cover applied.

What this means:

- If you’re the sole owner: You must have 100% coverage of the total loan amount. It cannot exceed that.

- If you’re a co-owner: Each co-owner’s share of the HPS coverage should reflect their contribution to the monthly housing loan payments.

Here’s an example to clarify:

If John covers 70% of the monthly housing instalments while Sarah covers the remaining 30%, their HPS coverage should ideally be split as 70% for John and 30% for Sarah.

Alternatively, they can each choose to insure themselves for up to 100% of the loan. This means both John and Sarah can opt for 100% coverage each.

By doing so, if either one passes away or becomes totally and permanently disabled, the entire loan will be repaid, ensuring financial security for the other party.

Paying the Premiums for HPS

One of the benefits of the HPS is that you can use your CPF Ordinary Account (OA) savings to pay the premiums. The premium is deducted automatically from your OA each year.

If there are insufficient funds in your OA, you’ll need to pay the premiums in cash. However, a family member who co-owns the flat with you (your spouse, parent, child, or sibling) can also authorise the CPF Board to use their OA savings to cover your premium shortfall.

As with any insurance, if you fail to pay the premiums on time, your coverage will lapse. If you decide to reapply later, your health will be reassessed, and your eligibility will be subject to approval.

Since HPS is a mortgage-reducing insurance, you’ll only need to pay premiums for 90% of your coverage period.

For example, if your coverage period is 30 years, you’ll only pay premiums for 27 years. This is because, over time, as your loan decreases, your coverage becomes less significant, making it unreasonable to continue paying the same premiums for minimal coverage in the later years.

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

How Much Are HPS Premiums?

The premiums you’ll need to pay for the HPS depend on four key factors:

| Factors | How it affects | |

|---|---|---|

| 1. | Outstanding housing loan on the flat | The higher your outstanding loan, the higher the coverage and subsequently the premiums you pay |

| 2. | Loan repayment period of the flat | The longer the coverage period, the higher the premiums |

| 3. | Type of loan (HDB concessionary or market rate) | The premiums for HPS may be higher for those with market rate loans |

| 4. | Age and gender of member | The older you are, the higher the premiums. Males generally have higher premiums than females |

To find out the exact premiums you’ll pay, you can use the CPF Home Protection Scheme (HPS) Premium Calculator. Your spouse should also enter their details for an accurate estimate.

Here’s an example:

John, who is 30 years old, took out a $500,000 HDB loan with a 25-year repayment period. He wants 100% coverage for the loan and will pay premiums for roughly the first 22 years. His annual premium comes to about $350, as of 2026.

How to Get an Exemption From HPS?

As mentioned earlier in the article, you can be exempted from HPS if you already have an existing private insurance policy. If you don’t have any current coverage but decide to take up private insurance later, you can still apply for an exemption from HPS at that time.

You can apply for an HPS exemption if you have one or more of the following insurance policies:

- Whole Life

- Term Life

- Endowment Plans

- Life Riders (must be attached to a basic policy)

- Mortgage Reducing Term Assurance (MRTA) / Decreasing Term Rider

Your insurance must cover the full loan repayment period or until you turn 65, whichever comes first. The coverage amount must also be enough to cover the outstanding loan balance.

If your insurance policies are terminated or lapse, your exemption may be revoked. In such cases, you may need to reapply for HPS coverage.

One practical tip from the CPF Board: apply for HPS first and seek the exemption after you’ve obtained legal ownership of the flat and the housing loan has been disbursed. This avoids any delay in using your CPF savings for your monthly instalments.

Steps to Apply for an HPS Exemption:

- Contact your insurance agent or provider to express your intention to apply for an HPS exemption.

- Complete the required form and provide all relevant documents, including your current housing loan details.

- Your insurance provider will verify that everything is in order before submitting the application to the CPF Board (applications are only processed through insurers).

- The Board will assess your application and notify you of the outcome.

Please note that HPS exemptions are subject to approval. If your exemption request reaches the CPF Board within one month of your HPS cover being issued, you’ll receive a full refund of the premium into your OA. After that, the refund is pro-rated upon termination of your cover.

The 5 Limitations of HPS

While HPS offers advantages such as the ability to use CPF OA to pay premiums, affordability, and core coverage, it does have its limitations.

Like most nationwide policies, HPS is designed to meet the basic needs of the general population, which means it may not fully address specific or more comprehensive coverage requirements.

1) Limited coverage options

HPS only covers death, terminal illness, and total and permanent disability (TPD), the basic forms of insurance.

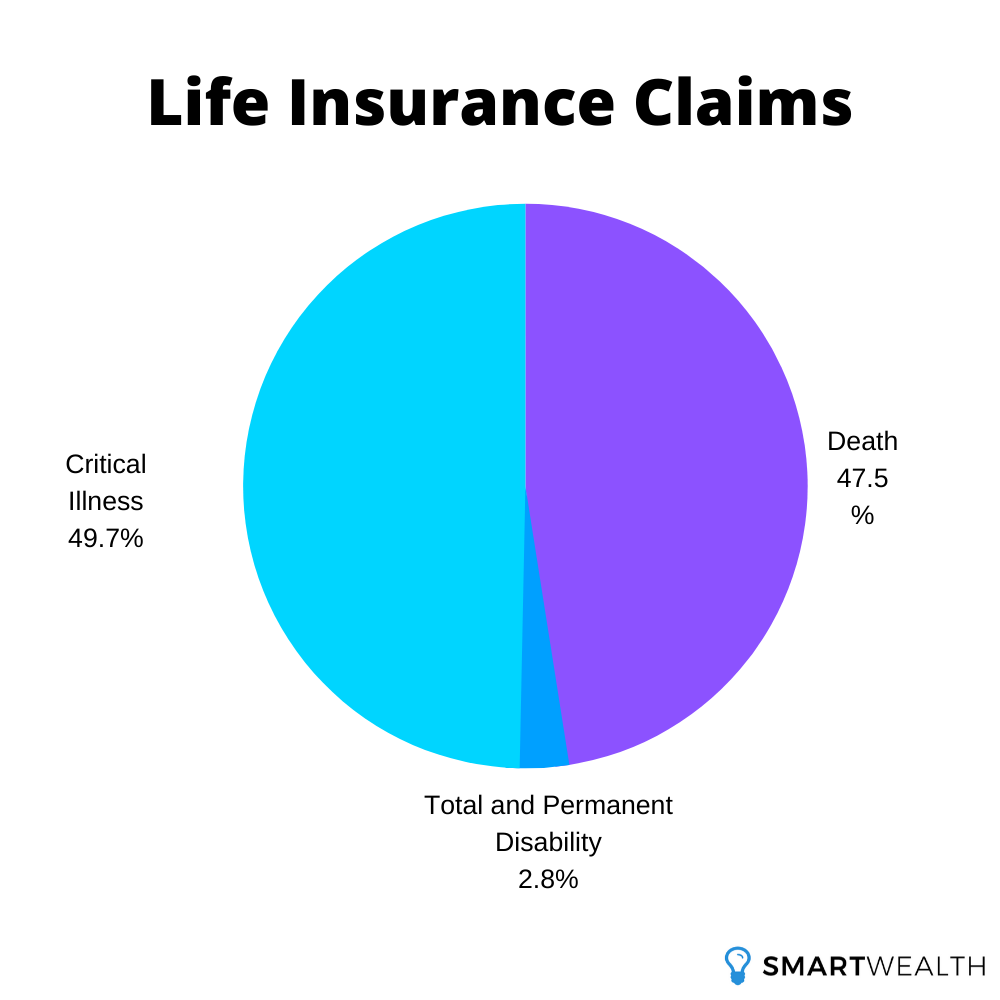

However, one critical area not covered by HPS (and which can’t be added on) is Critical Illness (CI).

Critical illness can be a significant risk, as its occurrence is more common than many think. From a study on life insurance claims, CI claims actually outnumbered claims for death and TPD.

If you were to be diagnosed with a major condition, such as cancer, the impact on your ability to work and earn an income could be devastating. How would you continue to make your mortgage payments?

A CI payout in that situation helps offset the HDB loan and eases the financial strain on your family.

While CI premiums are higher, if you’re seeking comprehensive protection, it’s worth considering additional coverage.

2) No option for higher coverage

As mentioned earlier, HPS covers up to 100% of your total loan amount, but no more.

Is that enough?

Consider this: if you’re a first-time homebuyer, you’re likely starting to plan for your family’s future. Beyond just your mortgage, you need to think about daily expenses, your children’s education, and retirement.

If your income stops due to a permanent disability, HPS may cover part or all of the HDB loan. But what about the other financial responsibilities and goals you have?

This is why, in the bigger picture, you may need more than just HPS. If you’re unsure about how much coverage you need, our life insurance coverage calculator can help you figure it out.

3) Coverage term is limited

There is a maximum coverage term under HPS.

HPS is designed specifically to cover your mortgage loan, but if you’re looking to protect your income until retirement or beyond, this coverage won’t be sufficient.

4) Coverage decreases over time

HPS is a mortgage-reducing term insurance, meaning your coverage decreases over time as you pay off your loan. This makes sense, as your loan balance reduces, so does the coverage.

However, imagine this: in 10 years, you may decide to upgrade or purchase another property. By that point, your remaining coverage will be much lower, and you’ll likely need significantly more coverage.

Unfortunately, HPS isn’t portable, so you can’t use it for your new property. You’ll either need to apply for a new HPS, or look into private mortgage insurance or term insurance, which can be more expensive, especially as you get older.

There’s also the risk of insurability. If you develop even minor health conditions over time (say, high cholesterol), you could be rejected for new insurance.

In the end, you might face a substantial liability without sufficient coverage to fall back on.

5) Premiums stay the same over time

While your coverage decreases over time, your HPS premiums remain the same.

In theory, your premiums should decrease as your coverage reduces, but unfortunately, this isn’t the case. So, you’re essentially paying the same premium for coverage that’s becoming less valuable as the years go by.

Are There Better Alternatives?

Yes, and that’s precisely why you can apply for an exemption from HPS.

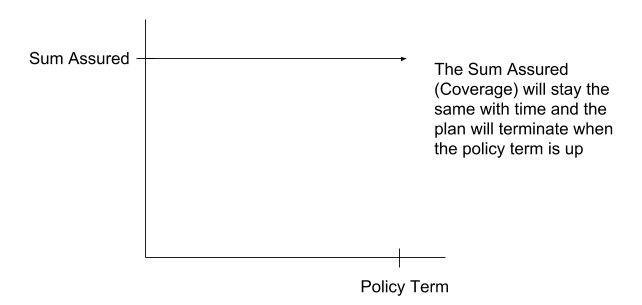

If you’re serious about long-term financial planning, one strong alternative is level term insurance. It offers several advantages that HPS doesn’t.

Here are a few key points about level term insurance:

- It can provide a much higher coverage amount

- It can include additional coverage, such as critical illness and early critical illness

- It can extend coverage up to age 99

- The coverage amount remains consistent throughout the term

- The premiums are competitive

So, what are your options?

First, remember that covering your mortgage is just one aspect of your overall financial plan. What about your other financial needs? Our guide to insurance planning in Singapore sets out what each layer of cover does and the order to buy it in. If you don’t have any existing life insurance or aren’t sure if you have enough coverage, take the first step and estimate how much you need.

Second, take some time to explore private mortgage insurance and level term insurance in Singapore. They could offer better alternatives, providing more comprehensive protection for you and your family.

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.