Curious about critical illness statistics in Singapore? Or maybe you’re wondering about the odds of contracting one?

Look no further.

We’ve gathered the most important facts and statistics on critical illness in Singapore, and we’ll keep this page updated regularly.

Our goal is to give you a clear picture of just how real the risk is, and why protecting your income and covering treatment costs with the right insurance coverage matters more than most people realise.

Critical Illness Statistics in Singapore (Summary)

- Cancer is the leading cause of death in Singapore, accounting for 26.5% of all deaths

- 1 in every 4 Singaporeans may develop a critical illness in their lifetime

- Treating a critical illness can cost $100,000 to $200,000 per year

- CI claims account for 49.68% of all life insurance claims

- Over 90% of CI claims come from just 5 conditions, with cancer making up 73.17% of those

- Most CI claims happen between the ages of 51 and 55

- The average CI claim payout is only $52,343, which for many people is not enough

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

A Primer on Critical Illness

The term “critical illness” or “CI” has different meanings depending on what you’re searching for.

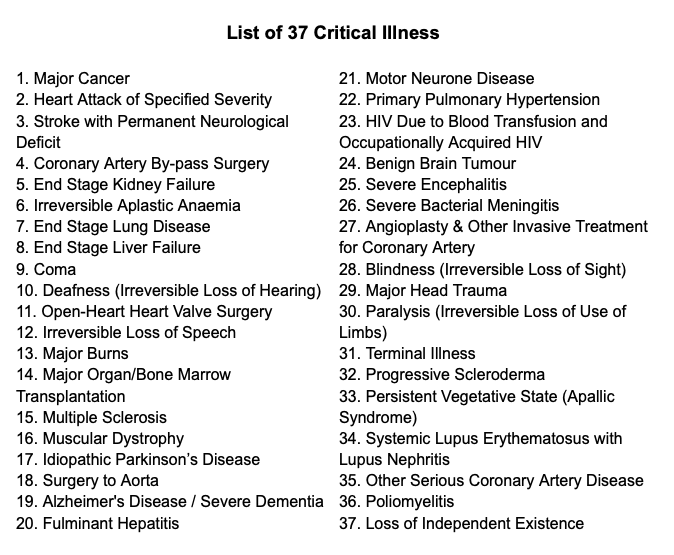

In this article, we’re not looking at other illnesses or chronic diseases such as high cholesterol, high blood pressure, and diabetes, but instead at the 37 critical illnesses defined by the Life Insurance Association Singapore (LIA).

The definitions of these critical illnesses are standardised across the industry to provide greater assurance, and cover conditions at their later stages.

Here’s the list of critical illnesses:

The definitions of these critical illnesses may change from time to time. The most recent change was in 2024, which took effect on 1 October 2025. Seven definitions were updated to reflect modern medical advances, and two condition names were reworded for clarity.

With that out of the way, let’s look at some statistics on critical illness.

1) Illnesses Are the Reason for a Huge Percentage of Deaths

Beyond LIA’s CI definitions, it helps to understand how illnesses and diseases actually contribute to death in Singapore.

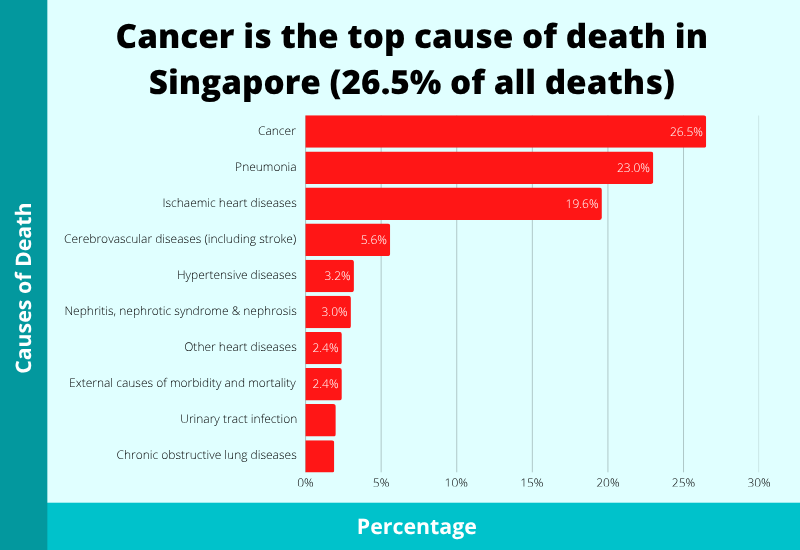

According to the Ministry of Health’s principal causes of death data, here are the leading causes of death in Singapore in 2024:

| Cause | Percentage of Deaths (2024) |

|---|---|

| Cancer | 26.5 |

| Pneumonia | 23.0 |

| Ischaemic heart diseases | 19.6 |

| Cerebrovascular diseases (including stroke) | 5.6 |

| Hypertensive diseases | 3.2 |

| Nephritis, nephrotic syndrome & nephrosis | 3.0 |

| Other heart diseases | 2.4 |

| External causes of morbidity and mortality | 2.4 |

| Urinary tract infection | 2.0 |

| Chronic obstructive lung diseases | 1.9 |

As you can see, cancer is the leading cause of death in Singapore, accounting for 26.5% of all deaths. Together with pneumonia and ischaemic heart diseases, the top three causes account for 69.1% of all deaths.

External causes such as accidents and intentional self-harm make up just 2.4% of all deaths.

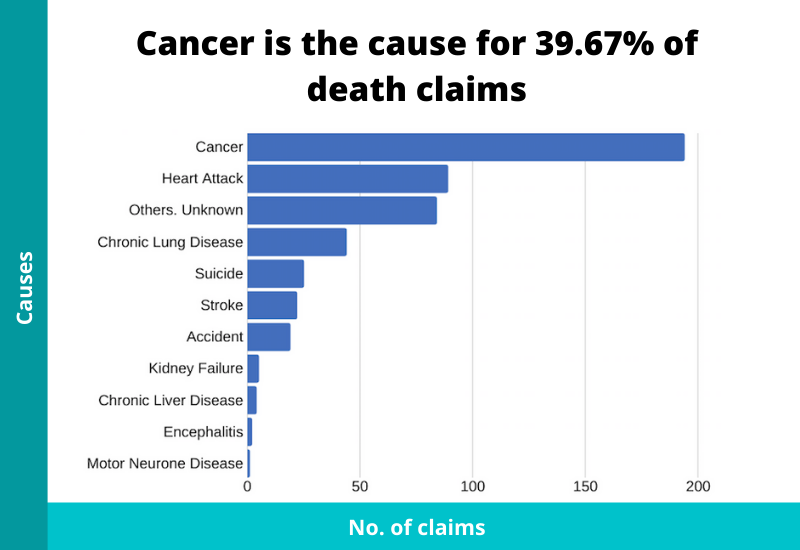

And when we look at the causes of death claims (life insurance), cancer is also at the top, accounting for 39.67% of all claims.

As the leading cause of both death and CI claims in Singapore, cancer is clearly the condition that deserves the most attention when planning your coverage.

2) 1 in Every 4 Singaporeans May Get A Critical Illness (Any Stage)

What’s the probability of getting a critical illness in Singapore?

Because it’s difficult to come up with one number to sum up all the probabilities of different critical illnesses, let’s just zoom into cancer for now.

Looking at the statistics on cancer, around 50 Singaporeans are diagnosed with it each day. And every day, around 17 Singaporeans die from it.

That being said, regardless of stage, the lifetime risk of developing cancer by the age of 75 is approximately 1 in 4 Singaporeans. To be precise, it is 26.8% for men and 26.2% for women.

Take note: cancer is just one of the many critical illnesses out there. If you factor others in, your overall chances of getting a critical illness will be higher.

3) The Cost of Treating a Critical Illness Can Amount to $100,000 to $200,000 per Year

Contracting a critical illness is not the end of your worries.

The next biggest worry is whether you’re able to pay for the treatments.

With high medical inflation, the cost of medical treatments continues to rise, and these treatments can last for a prolonged period.

Zooming into cancer again, there are various ways to treat it. Surgery, chemotherapy, and radiotherapy are the most common ones.

Even so, there’s no true cure for cancer as it can still come back. And so, there’s a constant need for diagnostic tests every year.

For late-stage cancer, the costs of treatment can be $100,000 to $200,000 per year.

But there’s also another type of cost, the cost of not being able to work.

Your income covers many things beyond treatment: daily expenses, future commitments, and financial goals.

If you’re unable to work because of an illness, who’s going to pay these expenses? Can your family cope while taking care of you and making up for your loss of income?

So, that’s why it’s crucial to replace your income if a CI happens.

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

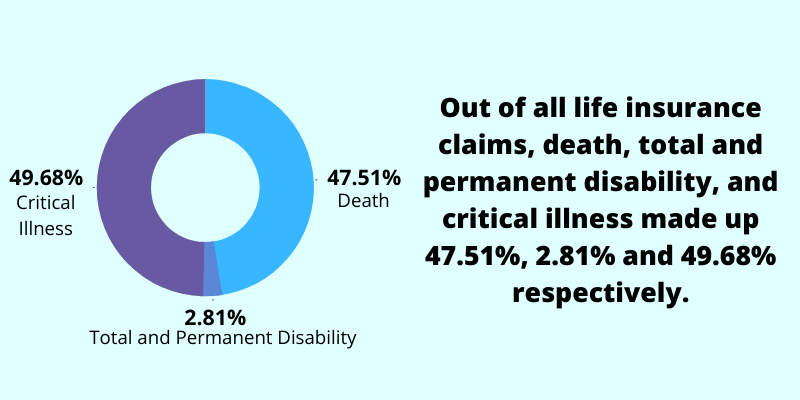

4) Critical Illness Claims Account for 49.68% of All Life Insurance Claims

In life insurance, there are 3 main types of coverage: death, total and permanent disability (TPD), and critical illness.

In an analysis we did, critical illness accounted for 49.68% of life insurance claims. 47.51% were death claims and only 2.81% were TPD claims.

CI claims exceeded death claims by a small margin.

However, if you factor in the causes of these death claims (a majority are caused by critical illnesses too), you’ll realise that CI plays a huge role in both CI and death claims.

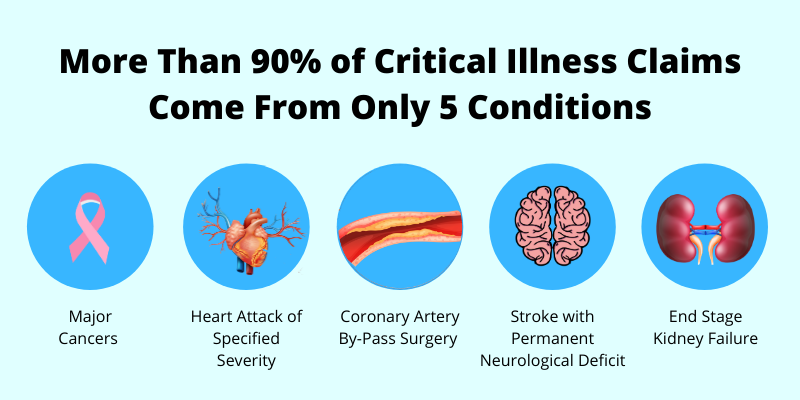

5) More than 90% of Critical Illness Claims Come From Only 5 Conditions

While there are 37 critical illnesses in the LIA framework, are they all important?

Turns out that only a few matter.

These are the 5 CIs that make up most of the CI claims (more than 90%):

- Major Cancers

- Heart Attack of Specified Severity

- Coronary Artery By-Pass Surgery

- Stroke with Permanent Neurological Deficit

- End Stage Kidney Failure

But it’s even more disproportionate than that.

From the analysis we did on 36 months of life insurance claims, we made a few interesting findings.

Firstly, the 5 conditions above indeed represented more than 90% of all CI claims, 93.45% to be precise.

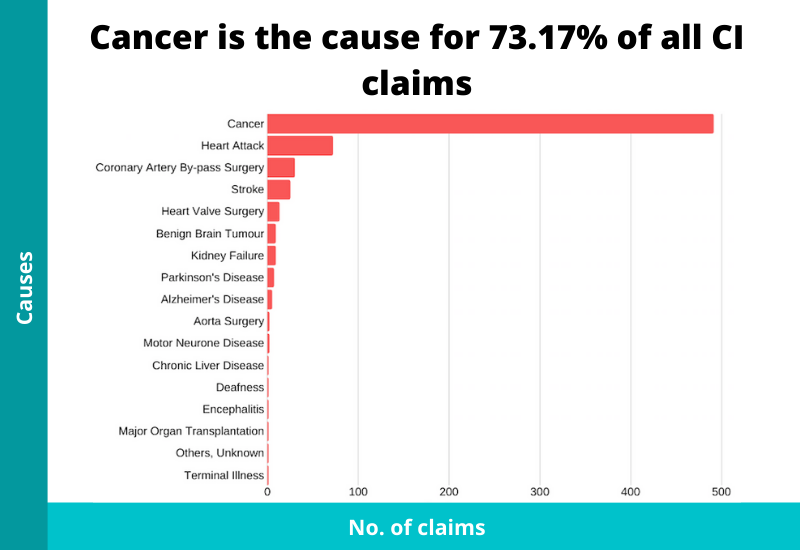

Secondly, of all the CI claims, cancer accounted for a huge majority, standing at 73.17%. This supports the fact that cancer is the top critical illness in Singapore.

This is why cancer-related benefits from early critical illness plans are important, given how much more likely it is to happen compared to other conditions.

Therefore, although it’s good to have a policy that covers 100+ conditions, only a few truly matter.

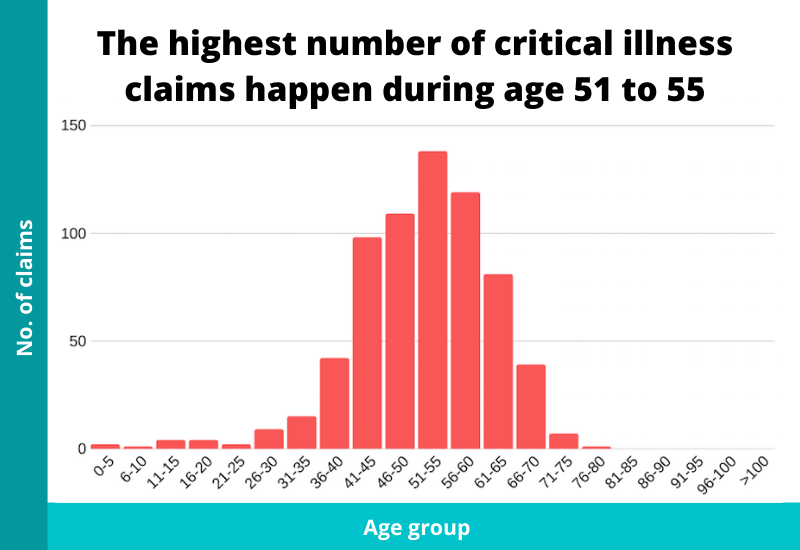

6) Most CI Claims Happen From Ages 51 to 55

Death claims tend to happen at an older age.

How about critical illness claims then?

From our analysis, most critical illness claims happen from age 51 to 55. And the bulk of claims happen from age 41 to 65.

So although this could indicate a period when CI coverage comes in handy, do take note that the data only includes in-force policies.

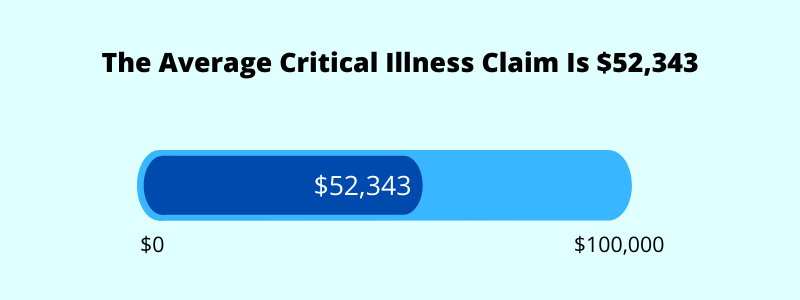

7) The Average Critical Illness Claim Is $52,343.37

We now know that the chances of contracting a CI are high.

And the costs to treat it are correspondingly high too.

While hospitalisation plans (when upgraded) pay out a substantial amount to cover medical bills, the cost of not being able to work remains.

That’s when critical illness coverage comes in.

It can come in the form of a rider that you can attach to term insurance or whole life insurance. And there are also standalone early critical illness plans that primarily cover CI of all stages.

These insurance plans pay out a lump sum when a CI happens. This money can then be used to replace your income during recovery, helping you continue to pay for family expenses and financial commitments while you’re unable to work.

Unfortunately, many Singaporeans face a significant protection gap.

According to the LIA Protection Gap Study, the recommended amount of critical illness coverage is 3.9 times your annual income, designed to cover living expenses and financial commitments over a typical 5-year recovery period.

Yet from the study we did, the average CI claim payout is only $52,343.37. For someone earning $5,000 a month, that amount would not even replace a single year of lost income, let alone five.

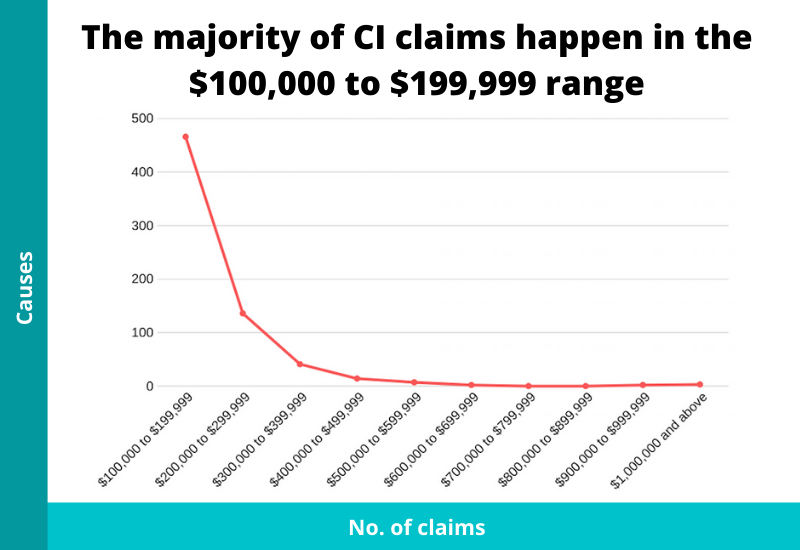

And even for those with more than $100,000 in CI coverage, a majority of claims fall in the $100,000 to $199,999 range, which still falls short of the LIA benchmark for many Singaporeans.

So the question worth asking is: do you have enough coverage to sustain yourself and your family if a CI were to happen today.

Wrapping Up

Knowing the importance of critical illnesses is one thing.

What are you going to do about it? Do you think you’re sufficiently covered right now?

Use our calculator to estimate how much critical illness coverage you need.

And if you wish to know more, check out the different insurance plans that can cover critical illness: term life insurance, whole life insurance, and early critical illness insurance.

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.