One in two Singapore residents is expected to develop severe disability at some point in their lifetime.

That’s the risk CareShield Life exists to cover. And from January 2026, the scheme has been through its biggest changes since it launched.

In this guide, I’ll cover what CareShield Life is, who’s covered, how much it pays out, what the 2026 changes mean for you, and what to do if you’re still on the older ElderShield scheme.

Key Takeaways

- CareShield Life is Singapore’s national long-term care insurance scheme. It pays a monthly cash payout for life if you become severely disabled, defined as being unable to perform at least 3 of the 6 Activities of Daily Living.

- A successful claim in 2026 pays $689 per month, for as long as the severe disability lasts.

- The scheme is compulsory for all Singapore Citizens and Permanent Residents born in 1980 or later, with automatic enrolment at age 30 and no opt-out. For those born in 1979 or earlier, joining is optional.

- Following the CareShield Life 2025 Review, payouts grow at 4% per year (up from 2%) from 2026 to 2030, reaching $806 per month by 2030.

- Premiums rise to fund the higher payouts, but government support of over $570 million caps the increase at no more than $75 per year for any policyholder up to 2030.

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

Why Long-Term Care Protection Matters

Three numbers frame the problem.

First, the big one: about 1 in 2 Singapore residents is expected to develop severe disability in their lifetime, based on the CPF Board’s figures. Severe disability can arrive suddenly through a stroke or accident, or gradually through conditions like dementia and diabetes.

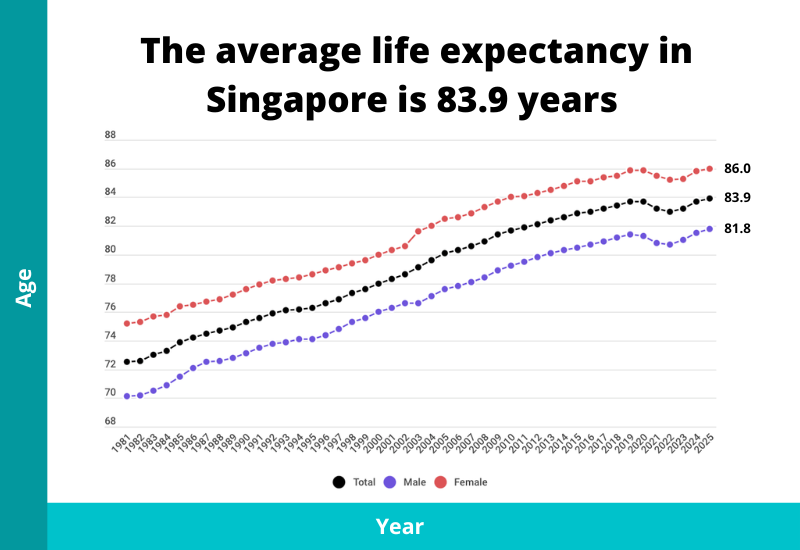

Second, we’re living longer than almost anyone else on Earth. Life expectancy in Singapore reached 83.9 years in 2025. A longer life means more years in which long-term care might be needed, and more years of paying for it.

Third, the care itself is expensive. Home-based care for someone with severe disability can run to around $2,700 a month based on Ministry of Health estimates, before subsidies. You can see how these costs fit into the wider picture in our healthcare cost statistics.

Long-term care is the kind of cost that can quietly drain a family’s savings for years. That’s the gap CareShield Life is designed to help with.

What Is CareShield Life?

CareShield Life is a severe disability insurance scheme run by the Government. It pays a monthly cash payout, for as long as you remain severely disabled, to help with the cost of long-term care. It was launched on 1 October 2020 as the successor to ElderShield.

The scheme is administered by the CPF Board, while the Agency for Integrated Care (AIC) handles disability assessments and claims.

It’s worth being clear on how CareShield Life differs from the other national schemes, because the names sound similar:

| Scheme | What it covers | How it pays |

|---|---|---|

| MediShield Life | Large hospital bills and selected outpatient treatments | Pays the hospital directly |

| Integrated Shield Plan | Private upgrade to MediShield Life for higher ward classes | Pays the hospital directly |

| CareShield Life | Long-term care during severe disability | Monthly cash to you |

The cash payout matters. Because it’s paid to you rather than to a hospital, you decide how to use it: a domestic helper, day care, home nursing, or topping up a family member’s time off work.

One more reassurance worth knowing: premiums collected stay in a dedicated insurance fund for the benefit of policyholders, and the Government doesn’t profit from the scheme.

Who Is Covered Under CareShield Life?

Coverage depends on the year you were born:

| Your situation | CareShield Life status |

|---|---|

| Born 1991 or later | Automatically enrolled when you turn 30 |

| Born 1980 to 1990 | Automatically enrolled on 1 October 2020 |

| Born 1970 to 1979, on ElderShield 400, not severely disabled | Automatically enrolled on 1 December 2021 |

| Born 1979 or earlier, all others | Optional. You can apply, now subject to underwriting |

| Became a Citizen or PR on or after 1 October 2020 | Compulsory regardless of birth year, unless you already had a disability when residency was granted |

For those born in 1980 or later, the scheme is compulsory and there’s no opt-out. Enrolment happens regardless of any pre-existing medical condition or disability. If you were born in 1990 or later, the CPF Board writes to you about two months before your 30th birthday.

For those born in 1979 or earlier, participation is optional, and this is where 2026 brought a significant change. When CareShield Life launched, older Singaporeans could join even with mild or moderate disability, as a time-limited concession. That grace period has ended. From 2026, applications from this cohort are subject to underwriting, so if you’ve been putting off the decision, you can still join, but on stricter terms. If you have health conditions, read our guide on insurance with pre-existing conditions before deciding your next step.

What Counts as Severe Disability?

You’re considered severely disabled when you’re unable to perform at least 3 of the 6 Activities of Daily Living (ADLs), as assessed by an MOH-accredited assessor:

- Washing: bathing or showering yourself, including getting in and out

- Dressing: putting on and taking off clothes, braces, or artificial limbs

- Feeding: feeding yourself once food is prepared and available

- Toileting: using the toilet, or managing bowel and bladder function with protective undergarments if needed

- Walking or moving around: moving from room to room on level surfaces indoors

- Transferring: moving between a bed and an upright chair or wheelchair

Note the strictness of the definition. Failing 1 or 2 ADLs, however life-changing, doesn’t qualify for a CareShield Life payout. I’ll come back to that gap later, because it’s the main reason supplements exist.

How Much Does CareShield Life Pay Out?

If a claim is approved in 2026, CareShield Life pays $689 per month in cash, for as long as you remain severely disabled. There’s no cap on the total amount or duration: if the disability lasts 20 years, the payouts last 20 years. Payouts stop only if you recover.

The payout amount you’re insured for increases each year until age 67 or until you make a successful claim, whichever comes first. Once you claim, the amount is locked at that year’s level for the duration of the disability.

Here’s how the payout has grown, and where it’s headed under the enhanced schedule:

| Year | Monthly payout |

|---|---|

| 2020 | $600 |

| 2021 | $612 |

| 2022 | $624 |

| 2023 | $637 |

| 2024 | $649 |

| 2025 | $662 |

| 2026 | $689 |

| 2027 | $717 |

| 2028 | $745 |

| 2029 | $775 |

| 2030 | $806 |

Figures from 2026 to 2030 follow the enhanced 4% growth schedule announced in the CareShield Life 2025 Review. Increases beyond 2030 will be reviewed then.

The claim-year lock is worth a concrete example. Take someone born in 1980. If they had claimed in 2022, they’d receive $624 per month for life. Claiming in 2026 instead locks in $689. The longer you go without claiming, the higher the amount you eventually lock in, up to age 67. After 67, your insured amount stays at the level it reached that year.

Two more features that often go unnoticed:

- Worldwide coverage. You stay covered, can make a claim, and receive payouts wherever in the world you live.

- No health-based pricing. Unlike private insurance, your premiums don’t depend on your health, only on your age at entry, gender, and cohort.

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

What Changed From 2026?

The Government accepted the CareShield Life Council’s recommendations in full on 27 August 2025, and the changes took effect progressively from January 2026.

Here’s what changed:

Payouts now grow at 4% per year, double the old rate. From 2026 to 2030, the insured payout amount rises 4% annually instead of 2%. Someone claiming in 2030 will receive $806 per month instead of the $731 it would have been under the old schedule. The effect compounds over a working lifetime: a 35-year-old in 2025 who claims at 67 would receive around $2,324 per month under the enhanced scheme, against $1,248 under the old one, based on the ministry’s illustrations. That projection assumes the 4% rate continues beyond 2030, which isn’t guaranteed.

Premiums rise, but the increase is capped. Higher payouts need higher premiums. Without support, annual premiums would have jumped by about $126 on average in 2026. Instead, the Government is providing over $570 million in additional premium support over five years, which moderates the increase to about $38 a year on average, and never more than $75, from 2026 to 2030. Lower and middle income policyholders see smaller increases still, thanks to means-tested subsidies.

Underwriting returned for the optional cohort. As covered earlier, those born in 1979 or earlier can no longer join with existing mild or moderate disability. Sign-up rates from this group had fallen by 90% since the scheme opened to them.

Claims are being streamlined. If you undergo a severe disability assessment for CareShield Life, you’ll soon be automatically assessed against the criteria for related schemes like the Home Caregiving Grant at the same time, without separate applications.

The enhanced payouts and premiums run to 2030 and will be reviewed again then, so nothing beyond 2030 is guaranteed.

CareShield Life Premiums and Subsidies

Premiums are fully payable by MediSave, so for most people there’s no cash outlay at all. Immediate family members can pay your premiums from their MediSave too, or vice versa.

You pay premiums from the year you join until age 67, or for 10 years, whichever is later. So someone enrolled at 30 pays until 67, while someone who joins at 62 pays until 72. Once premiums are done, coverage continues for life. Premiums also stop the moment you make a successful claim.

Your premium has up to two parts:

- Base premium. What everyone pays. It increases yearly alongside payouts until age 67.

- Catch-up component. A flat top-up paid over 10 years by those who joined later or paid less into the old system, such as former ElderShield 300 policyholders or those who had no ElderShield cover. It puts everyone in a cohort on an even footing.

Starting premiums vary by age, gender, and cohort, so the practical step is to check your own figure with the official premium checker using your Singpass.

If affordability is a concern, there are four forms of support:

- Means-tested premium subsidies of up to 30% of the base premium for lower and middle income households

- Transitional support from 2026 to 2030, applied automatically to phase in the premium increases for all affected policyholders

- Participation incentives of up to $4,000 spread over 10 years, for those born in 1979 or earlier who joined by 31 December 2024

- Additional Premium Support for those who can’t afford premiums even after subsidies and family help

The Ministry of Health has been consistent on this point: no one will lose CareShield Life coverage because they can’t pay their premiums.

Born in 1979 or Earlier? ElderShield vs CareShield Life

If you’re in the older cohort, your starting point is probably ElderShield, the scheme CareShield Life replaced.

ElderShield was launched in 2002 as severe disability insurance. It paid $300 a month for up to 60 months (ElderShield 300), later improved in 2007 to $400 a month for up to 72 months (ElderShield 400). The scheme is now closed to new applications, and the Government took over its administration from the private insurers on 1 November 2021.

Here’s how the two compare:

| Feature | ElderShield 300 / 400 | CareShield Life |

|---|---|---|

| Monthly payout | $300 / $400 | $689 in 2026, rising yearly |

| Payout duration | 5 years / 6 years | Lifetime of the disability |

| Payout increases | None | 4% per year until age 67 or claim (2026 to 2030) |

| Premiums | Fixed at entry, payable to 65 | Increase over time, payable to 67 |

| Government subsidies | None | Yes, means-tested and transitional |

| MediSave payable | Yes | Yes |

| Claim criteria | Unable to perform 3 of 6 ADLs | Unable to perform 3 of 6 ADLs |

The claim bar is identical. What CareShield Life buys you is a larger payout that lasts as long as the disability does, rather than running out after five or six years. Given that severe disability in old age can stretch well past six years, the lifetime duration is the single biggest difference.

So should you switch? It depends on where you stand:

If you were on ElderShield 400 and born between 1970 and 1979, the decision was likely made for you: you were automatically enrolled into CareShield Life on 1 December 2021, and the window to opt back out closed at the end of 2023. Your ElderShield premiums were taken into account in your CareShield Life premiums.

If you’re on basic ElderShield and weren’t auto-enrolled, you can still apply to join CareShield Life. Your ElderShield policy is replaced if the application succeeds, and past ElderShield premiums count towards your CareShield Life premiums. Two things have changed since the early years, though: applications are now underwritten, and the $4,000 participation incentive closed to new joiners after 31 December 2024. The case for switching is still the lifetime payout, but the entry terms are less generous than they were.

If you upgraded your ElderShield with a supplement, don’t rush. Your ElderShield supplement continues untouched, and in my opinion, replacing an established supplement may not be worth it: a new plan may exclude pre-existing conditions your old one covers. Compare the total benefits carefully before changing anything.

If you have no ElderShield at all, whether from opting out years ago or being over 40 when it launched in 2002, you can apply for CareShield Life directly, subject to underwriting. Check your premium first, since a catch-up component will apply.

How to Make a Claim

The claims process runs through three steps:

- Arrange a disability assessment. Find an MOH-accredited severe disability assessor through the AIC website. Your regular GP can’t certify severe disability unless they’re accredited.

- Attend the assessment. It costs $100 at a clinic or $250 for a house call. Your first assessment for CareShield Life is free. For later assessments, you pay the assessor, and the full fee is reimbursed with your first payout if the claim succeeds.

- Submit the claim. Log in with Singpass to AIC’s eFASS portal to apply.

If the assessor certifies that you can’t perform at least 3 of the 6 ADLs, the monthly payouts begin. Periodic reassessments may be required, which is where the reimbursed fee matters.

Is the CareShield Life Payout Enough?

For most families, no, not on its own. CareShield Life is deliberately a basic layer.

The Ministry of Health’s own worked examples make the arithmetic plain. Home-based care for severe disability costs about $2,700 a month. For a lower-income household with maximum subsidies and grants covering around $1,900, the CareShield Life payout closes most of the rest, leaving roughly $110 out of pocket. A Category IV nursing home costs about $4,900 a month, and even with a 75% subsidy, the same household still faces around $510 a month after the CareShield Life payout.

Those figures assume the highest tiers of means-tested support. A middle or higher income household receives smaller subsidies, so the gap between $689 and the real cost of care lands on savings and family.

Three things can close that gap:

- MediSave Care lets those aged 30 and above with severe disability withdraw a combined total of up to $200 a month from their own and/or their spouse’s MediSave.

- The Home Caregiving Grant rises to up to $600 a month from April 2026, for those caring for a loved one at home.

- A CareShield Life supplement from a private insurer raises the monthly payout by up to $5,000 depending on the plan, and some plans pay out from the inability to perform just 1 or 2 ADLs, a much lower claim bar than the national scheme. Premiums are payable by MediSave up to $600 a year, with any excess in cash. Applications are subject to underwriting and health disclosure.

There’s a strict-definition point hiding in that last bullet. CareShield Life pays nothing for mild or moderate disability, even if it stops you from working. If failing 1 or 2 ADLs would seriously strain your family’s finances, that risk sits entirely outside the national scheme, and a supplement is the only insurance answer to it.

In Closing

CareShield Life gives every Singaporean born in 1980 or later a base level of protection against the cost of severe disability: $689 a month in 2026, growing to $806 by 2030, paid for the full duration of the disability. The 2026 enhancements raised that protection meaningfully, and the premium support keeps it affordable while it rises.

But basic protection is all it is. The payout covers a fraction of what long-term care actually costs, the claim criteria are strict at 3 of 6 ADLs, and anything milder isn’t covered at all.

Two practical steps follow.

First, if you’re in the optional cohort and still undecided, check your premium and bear in mind that the entry terms tightened in 2026, so waiting has a real cost.

Second, whatever your age, work out what severe disability would actually cost your household and whether the basic payout covers a meaningful share of it.

Long-term care is just one layer of a complete insurance plan, so it helps to see where it sits against your other cover. Our guide to CareShield Life supplements walks through the upgrade options, and if you’d like a personal review, our Solutions page shows how we approach it.

For you and your loved ones, this is one of those schemes worth understanding before you ever need it..

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.