Most of us buy life insurance for the people we’d leave behind. Then we file the policy away and never think about it again.

But have you pictured what actually happens when a claim is made? Would your family get the money quickly, or would they be stuck filling in forms and waiting on a court order while they’re grieving?

That’s what an insurance nomination sorts out. It tells your insurer exactly who should receive the proceeds, and it can be the difference between a payout in weeks and a payout in many months.

In this guide we’ll cover what a nomination is, which policies it applies to, what happens if you skip it, the two types you can make, and the new online option that’s been available since 2024. It’s one of the simpler parts of estate planning in Singapore, and it’s free.

What Is an Insurance Nomination of Beneficiaries?

A nomination is your written instruction telling your insurer who should receive the proceeds of your policy when you die, and what share each person gets.

The framework comes from the Nomination of Beneficiaries (NOB) provisions introduced into the Insurance Act on 1 September 2009. Before that, getting insurance money to the right people could mean going through the courts. The 2009 rules gave policy owners a clear, affordable way to name beneficiaries directly.

A few ground rules apply to every nomination:

- You must be the policy owner, and the policy must be on your own life.

- You must be at least 18 years old.

- You can name one person or several, and you set the percentage each receives. The shares must add up to 100% of that policy’s proceeds.

You’re not required to make a nomination. But without one, the money can’t simply be handed over. Your family may need a Grant of Probate or Letters of Administration first, and that takes time. We’ll come back to that.

There are two types of nomination, revocable and trust (irrevocable), and the rest of this guide explains how each one works and when it makes sense.

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

Which Policies Can and Can’t Be Nominated?

Nomination applies to life policies and to accident and health policies that pay a death benefit. Your term and whole life plans usually qualify. But there are some exceptions, and a few policies where a nomination either isn’t allowed or wouldn’t achieve anything.

The Life Insurance Association’s nomination guide sets out which nomination types apply to each policy. Here’s a quick view of the common policy types:

| Policy type | Revocable nomination | Trust nomination |

|---|---|---|

| Term and whole life insurance | Yes | Yes |

| Accident and health plan with a death benefit | Yes | Yes |

| Policy paid for with CPF savings | Yes | No (you must keep full control while alive) |

| Integrated Shield Plan | Technically yes, but pointless | No |

| CPF Retirement Sum Scheme annuity | No | No |

| Employer group insurance | Not applicable | Not applicable |

A few quick points on the exceptions:

- Employer group insurance: your employer owns the policy, not you, so you can’t make a nomination on it. The proceeds follow the policy’s own terms. It’s one reason group cover shouldn’t be your only life insurance.

- Integrated Shield Plans: an Integrated Shield Plan pays your hospital bills rather than leaving money behind, so a trust nomination isn’t allowed and a revocable one achieves little.

- CPF-funded policies: you must keep full control while alive, so only a revocable nomination is allowed. CPF Retirement Sum Scheme annuities can’t be nominated at all, as any leftover returns to your CPF and follows your CPF nomination instead.

Muslim policy owners can make both types of nomination. Anything left outside a nomination follows the inheritance certificate from the Syariah Court rather than the usual intestacy rules.

Older policies bought before September 2009

Policies taken out before the nomination law began on 1 September 2009 sit in a separate category, and they can still cause headaches today.

Back then, the modern revocable nomination didn’t exist. If you took out a policy on your own life and stated it was for the benefit of your spouse and/or children, section 73 of the Conveyancing and Law of Property Act automatically created a trust in their favour. It was the only way to give the people you named a real, enforceable claim, and it worked much like today’s trust nomination: the proceeds sat outside your estate and beyond your creditors, but you gave up the freedom to change your mind.

That rigidity is where the problems came from. Once the trust existed, your beneficiaries had a fixed interest, so you couldn’t simply swap them out, surrender the policy, or deal with the proceeds on your own. A divorce, a fallout, or a named child passing away could all leave a policy stuck.

These old section 73 trusts are still recognised, and the 2009 framework doesn’t override them. If you’ve never made a nomination on a pre-2009 policy, you can make one now. But if you named your spouse or children back then, or your situation is anything but straightforward, it’s worth getting legal advice before you assume you can change it.

What Happens If You Don’t Make a Nomination?

You’re not obliged to nominate. But without one, your insurer can’t simply hand the money over. What happens next depends on whether you left a will.

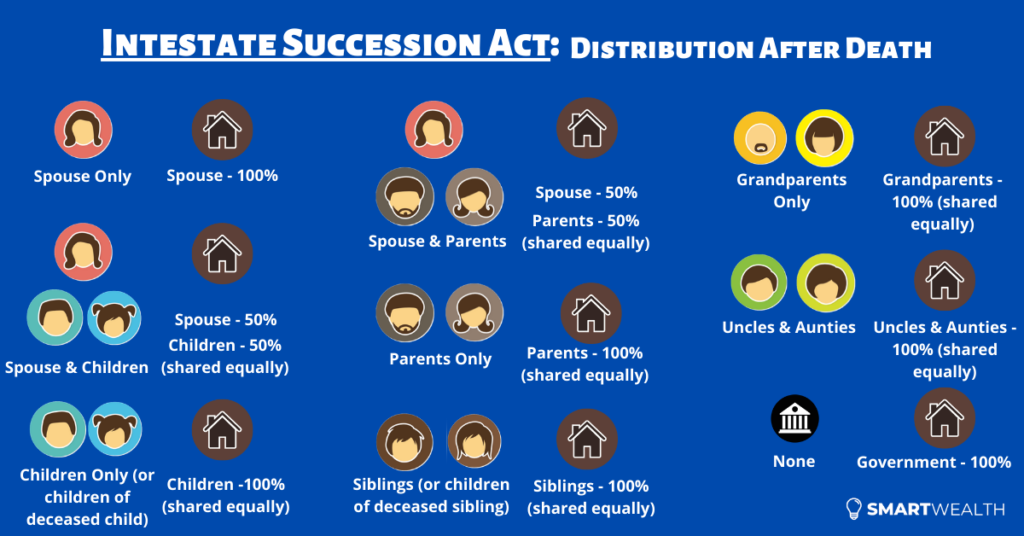

No nomination and no will

Your insurance proceeds, along with the rest of your estate, are distributed under Singapore’s intestacy laws. A spouse and children, for example, would typically split everything 50:50.

To give your family some immediate cash, the insurer can pay out up to $150,000 to a “proper claimant”, usually a close family member or the executor of the estate. Anything above that is held until someone obtains a Grant of Letters of Administration, the court order that lets an administrator collect and distribute the estate. That can take months, as we explain in our guide on dying without a will.

Receiving that $150,000 doesn’t make the person entitled to keep it. It still has to be shared out according to the law.

No nomination but a valid will

If you’ve written a will and notified your insurer of it, the proceeds can be distributed according to the will. The insurer releases the money to your executor, who shares it out.

That’s better than nothing, but still slower than a nomination. The insurer may only pay once a Grant of Probate is obtained, which again takes months.

Why a nomination helps

With a valid nomination in place and the claim documents in order, the full death benefit can be paid straight to your nominees, with no court order and no long wait. That speed, at the moment your family needs the money most, is the whole point.

Even so, payouts still go unclaimed when no one knows a policy exists. More than 8,000 were sitting unclaimed the last time the industry counted, and there’s no longer a public register to search. So tell your family which policies you hold.

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

Is Making a Nomination Always the Right Move?

Not always.

A nomination gets money to your beneficiaries fast, with no court process in the way. Usually that’s exactly what you want. But quick access isn’t always wise.

If your nominees are young children, a nomination could hand them a large sum the moment they come of age, with no one to manage it in the meantime. The same worry applies to a beneficiary who isn’t great with money. Where your nominees are independent adults, it’s rarely a problem.

So you have options. You might nominate some policies for fast liquidity and leave others to be paid through a will with a testamentary trust, which lets you release the money in stages rather than all at once. For even more say over how and when your money is shared out, a living trust gives you greater flexibility.

The right mix comes down to your family and what you’re trying to achieve.

The Two Types: Revocable vs Trust (Irrevocable)

Both types let you name who receives your proceeds and in what share. What differs is how much control you keep, and who you’re allowed to name. Most people choose the revocable type. Trust nominations are for specific situations where you’re certain.

Revocable nomination (Form 4)

This is the flexible, and far more common, option. You make it on Form 4, the revocable nomination form under the Insurance Act.

You keep full ownership of the policy and can change or cancel the nomination at any time, without asking your nominees. Only the death benefit goes to them. Any living benefits, such as a critical illness payout, are still paid to you.

You can name anyone, not just family, including a friend, a partner, or an organisation. Set each nominee’s share so they add up to 100%, and sign the form in front of two witnesses (the forms call them “appropriate signatories”) who are at least 21 and aren’t your nominees or their spouses.

If a nominee dies before you, the nomination doesn’t simply lapse. Where there’s more than one, the survivors share the deceased’s portion. Where the last remaining nominee dies, the nomination is revoked.

Trust nomination (Form 1)

A trust nomination is permanent in a way the revocable one isn’t. You make it on Form 1, the trust nomination form under the Insurance Act.

Here you give up all rights to the policy. Every benefit, living and death, now belongs to your nominees, even though you still pay the premiums. You can only nominate your spouse and/or children, and you can’t change your mind on your own afterwards. Revoking it needs the consent of all the nominees, or of a trustee who isn’t you.

You also name a trustee to hold the proceeds for your nominees. They must be at least 18 (an organisation can serve too), and can be one of your nominees. You can name yourself, but then you can’t receive the money or approve a revocation, only another trustee can.

The trade-off buys one useful protection. If you’re made bankrupt, the proceeds are generally beyond the reach of your creditors. That’s why a trust nomination suits someone who is completely sure they want the money to go to their spouse or children, whatever happens.

If a nominee dies before you, their share passes to that nominee’s estate, not to the other nominees.

Revocable vs Trust Nomination: Side by Side

Here are the two at a glance:

| Revocable nomination | Trust nomination | |

|---|---|---|

| Who you can name | Anyone, including organisations | Spouse and/or children only |

| Control of the policy | Stays fully with you | Passes to your nominees |

| Which benefits nominees get | Death benefit only | Living and death benefits |

| Can you change it later | Yes, any time, on your own | No, only with the nominees’ or a trustee’s consent |

| If a nominee dies before you | Surviving nominees share their portion (nomination ends if none survive) | Their share goes to the nominee’s estate |

| Protection from creditors in bankruptcy | Generally no | Generally yes |

| Can it be submitted online | Yes, where your insurer offers it | No, hardcopy with original signatures only |

For most people, the revocable nomination does the job. The trust version only makes sense when locking the money to your spouse or children, and the creditor protection that comes with it, matters more to you than staying in control.

Does a Will Override Your Nomination?

A trust nomination can’t be overridden by a will. Once it’s made, the policy sits outside your estate, so your will has no say over it.

A revocable nomination can be overridden by a will, but only if the will is made later and is drafted specifically to deal with that policy. A general will that simply leaves “everything to my children” won’t do it.

To keep things simple, pick one or the other. If you want the policy handled by a nomination, make the nomination and leave that policy out of your will. If you’d rather it follow your will, don’t make a nomination, or cancel any you’ve already made, so the will decides. Putting the same policy in both is where disputes start.

How to Make a Nomination

You can do this yourself, for free, straight with your insurer. No lawyer needed.

Since 2024, a growing number of insurers let you make a revocable nomination online, signing digitally with Singpass, with your witnesses confirming it digitally too. A trust nomination still has to be done on paper, with original signatures.

Either way, the steps are much the same:

- Get the right form from your insurer (Form 4 for a revocable nomination, Form 1 for a trust nomination).

- Name your beneficiaries and the share each receives, adding up to 100%.

- Sign it in front of two witnesses who are at least 21 and aren’t your nominees or their spouses.

- Submit it to your insurer. The nomination only counts once they’ve received and accepted it.

One thing to watch: the form has to be filled in fully and correctly. A blank field, a mistake, or a crossing-out can get the whole thing rejected. Take your time over it, and keep a copy.

A nomination applies only to the policy you make it on, so check that each policy you hold is covered. Once it’s in place it stays valid until you change or cancel it, with no need to redo it when the policy renews. A new policy, though, needs its own nomination, even with the same insurer.

If you’d rather not handle it alone, your financial adviser can help.

Don’t Forget the Rest of Your Estate Plan

An insurance nomination is one of the simplest things you can do for the people you love, and it costs nothing. If you’ve bought life insurance for their sake, it’s worth a few minutes to make sure the money reaches them without delay.

But a nomination only covers your insurance policies. It’s one piece of a bigger picture. The other pieces include making a CPF nomination, writing a will, and sometimes setting up a trust. Together they form a solid estate plan that gets the right things to the right people, with as little hassle as possible.

If you’d like to see how your insurance, savings and estate plans fit together, our FullCircle financial planning session gives you a clearer view of where you stand and what to prioritise.

This article is for general information and isn’t financial or legal advice. For help with your own circumstances, speak to a licensed adviser.

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.