What happens to your money, your home, and even your medical decisions if you pass away or lose your mental capacity without the right paperwork in place?

For a lot of Singaporeans, the answer is “I’m not sure,” and that gap shows up in the numbers below.

The reassuring part is that the fixes are mostly simple, and several are free.

Here are the key statistics on inheritance and estate planning in Singapore. We’ve leaned on official government data wherever possible, and used survey data for the things no government agency tracks.

Getting these basics right, alongside the right protection for your family, is what stops your hard work from going to the wrong place.

Key Estate Planning Figures at a Glance (2026)

- $278 million in unclaimed monies was sitting with the Public Trustee’s Office as at 31 December 2024, including $184 million of un-nominated CPF savings

- Around $67 million of un-nominated CPF was added to that pool in 2024 alone

- About 8 in 10 CPF members who died in 2024 had made a nomination, but only 36% of living members aged 16 to 64 have

- Only 22% of Singapore residents have a legally drafted will, and just 12% have set up a trust

- About 1 in 7 Singapore citizens (404,000) have made a Lasting Power of Attorney as of February 2026, and even among over-65s only about 1 in 4 have

- More than half (51%) of older Singaporeans without an LPA wrongly believe their children could automatically act for them if they lost mental capacity

- There’s no longer a public tally of unclaimed life insurance, after the industry’s register was withdrawn over data-privacy concerns

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

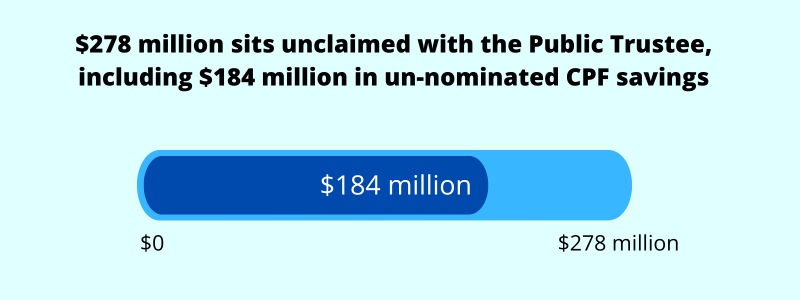

$278 Million Is Sitting Unclaimed With the Public Trustee

When someone dies in Singapore without naming who should receive their CPF, the money doesn’t vanish, but it doesn’t reach the family quickly either. It goes to the Public Trustee’s Office (PTO), which then has to trace and pay the rightful next-of-kin.

As at 31 December 2024, $278 million of unclaimed monies was sitting with the Public Trustee’s Office. Of that, $184 million was un-nominated CPF savings and the remaining $94 million was other estate monies. In 2024 alone, around $67 million of fresh un-nominated CPF was added to the pile.

It helps to see the bigger flow behind that number. Over the five years from 2020 to 2024, about $1.33 billion of CPF belonging to deceased members, roughly 16% of the total, was transferred to the PTO because there was no nomination. The office has since distributed about $1.13 billion of it, or 85%. So most of it does eventually reach families. The “unclaimed” pile is the residue left over, usually because the office simply can’t trace or contact the beneficiaries.

This is the part worth acting on. If you’ve made a CPF nomination, your nominees are paid directly by the CPF Board, free of charge, generally within about five weeks. If you haven’t, your savings take the long way round: distribution follows the Intestate Succession Act or Muslim inheritance law.

The Public Trustee charges a statutory fee on top, and the whole thing can take up to six months.

The same money, just slower and costlier, all because a form never got filled in.

Nearly 2 in 3 Working-Age Members Haven’t Made a CPF Nomination

Around 80% of CPF members who died in 2024 had made a nomination, according to the Ministry of Manpower. For most families, that means the savings are released quickly and split the way the member wanted.

The problem is the age gap. The same parliamentary reply put nomination rates at about 86% for members aged 65 and above, but just 36% for those aged 16 to 64. And most of that younger group who haven’t nominated are 44 or below.

It’s the classic “I’ll get to it later”.

Nomination rates climb steeply with age, so younger members are the least protected at exactly the point an early death would cause the most upheaval for those left behind. CPF Board figures show 2 in 5 members who died before 65 in 2023 had no nomination, and the median balance those younger members leave behind has been rising.

One encouraging shift: more than half of all nominations in 2023 were done online. Moving the process onto Singpass has clearly taken the friction out of it. You still need two witnesses, but you can sort it from your phone in a few minutes.

8,000+ Insurance Payouts Were Unclaimed, and Now No One Counts

CPF isn’t the only money that gets stuck. Life insurance payouts go unclaimed too, usually for a simple reason: the insurer is never told the policyholder has died, so it doesn’t know to pay anyone.

How big is the problem? We can’t really say any more. The last public figures are years old. When the Life Insurance Association (LIA) launched a public Register of Unclaimed Life Insurance Proceeds in 2016, more than 8,000 payouts were sitting unclaimed. By the register’s 2018 update, it had reunited 1,437 people with their money, including $9.87 million paid out in 2017.

That register has since been permanently withdrawn over data-privacy concerns. So today, if you suspect a relative had a policy, there’s no central list to search. You have to approach each insurer directly. The one tool that made unclaimed insurance visible is gone, which makes prevention matter more than the figures ever did.

The fix is low-tech but effective. A payout can only reach your family if they know the policy exists, so make sure someone you trust knows which insurers you’re with, ideally with a written list of your policies. Making a nomination still helps, directing who gets the money and speeding up the claim, but it can’t stop a payout going unclaimed if no one knows to claim in the first place.

The Hidden Assets No Register Will Find

Everything so far has a paper trail.

CPF, insurance, and bank accounts can eventually be traced, even if it takes the Public Trustee months to do it. But a growing share of what people own leaves no trail at all.

Think about cryptocurrency, e-wallets, overseas brokerage accounts, or a trading account opened online. If you’re the only one who knows these exist, that knowledge goes with you. There’s no register to comb and no agency that gets notified. Unlike CPF or insurance, nobody comes looking, because nobody knows there’s anything to look for.

There are no statistics on how much vanishes this way, for the obvious reason that untracked assets can’t be counted. But as more of our money moves into digital and overseas accounts, it’s a fair bet the problem is growing rather than shrinking.

There’s an easy safeguard. Keep an up-to-date list of what you own and where it sits, and make sure someone you trust can get to it. A will can legally leave these assets to someone, but it can’t help your executor claim an account they don’t know exists, or unlock a crypto wallet without the password. That’s the gap a record fills.

And if you haven’t got round to writing a will yet, our free FinSnap template is a good place to start keeping track of what you have, though a plain document works just as well.

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

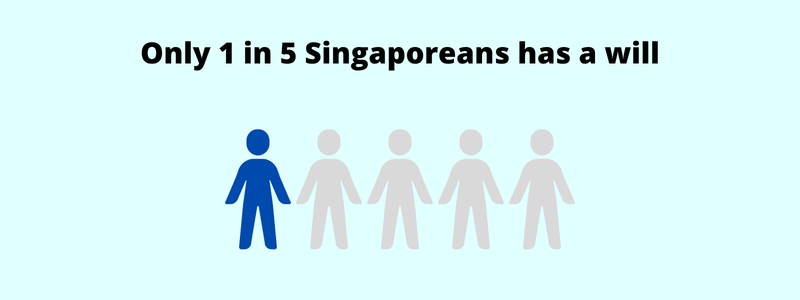

Barely 1 in 5 Singaporeans Has a Will

A will is the most basic estate planning document, and the one most people put off. Just 22% of Singapore residents have a legally drafted will, according to a YouGov survey from April 2024.

That’s a self-reported survey rather than an official count, so treat it as a guide rather than a precise figure, but the direction is clear: most of us don’t have one.

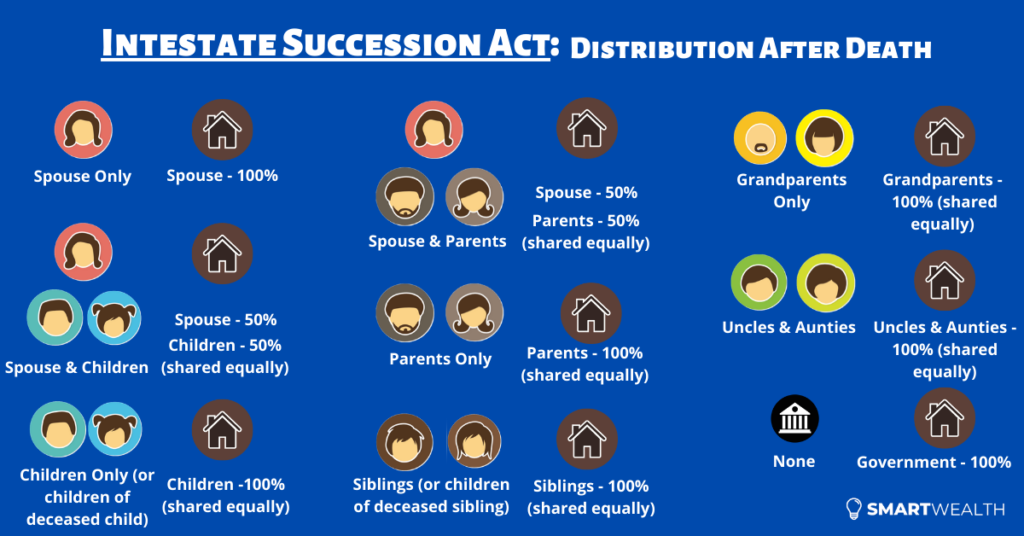

Anyone aged 21 and above can make one. Without it, you die intestate, and the Intestate Succession Act decides who gets what, in fixed proportions that may not match what you would have chosen. For Muslims, distribution follows inheritance law instead.

Here’s what surprises people most: a will doesn’t cover everything you own. Three big things usually sit outside it.

- Your CPF savings, which only go to the people named in your CPF nomination, not through a will

- Most insurance payouts, where you’ve named someone on the policy

- Jointly-owned property held in joint tenancy, which goes straight to the surviving owner

So your will and your nominations have to work together. One without the other leaves gaps. If you’ve written a will but never nominated your CPF, a sizeable chunk of your wealth still isn’t going where the will says.

Just 12% of Singaporeans Have Set Up a Trust

A trust is the next step up from a will, useful when you want more control over how and when your money reaches people.

Common reasons include providing for young children, a dependant with special needs, or releasing money to beneficiaries in stages rather than all at once. Even so, trusts remain uncommon. Only 12% of Singapore residents have set one up, according to the same YouGov survey.

That’s not surprising.

A trust costs more to set up and run than a will, and most people don’t need one. But the low figure hints that some who would genuinely benefit, especially parents of young or vulnerable children, haven’t looked into it. If that sounds like you, it’s worth understanding how setting up a trust works before you decide either way.

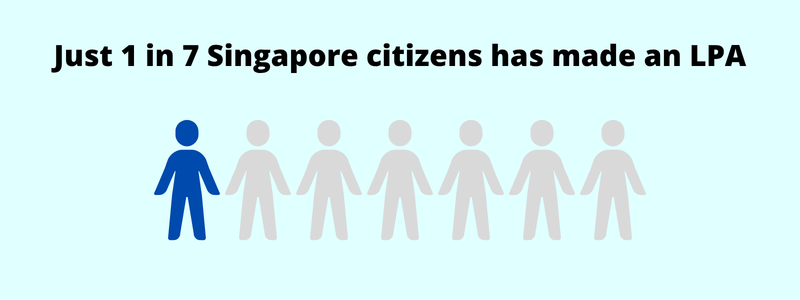

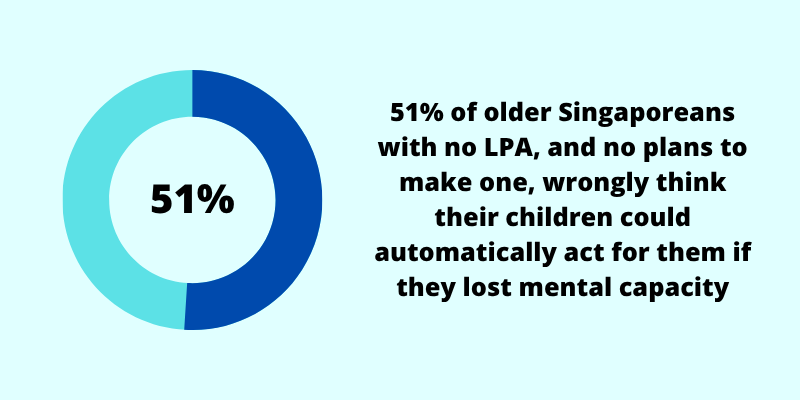

Only 1 in 7 Singaporeans Has Made an LPA

Everything above deals with what happens after you die.

But estate planning covers a second risk too: losing your mental capacity while you’re still alive, through dementia, a stroke, or an accident. That’s what a Lasting Power of Attorney (LPA) is for. It lets you appoint someone you trust to manage your money and make care decisions if you can no longer do so yourself.

Uptake is rising, but it’s still low. As of February 2026, 404,000 Singapore citizens, about 1 in 7, had made an LPA, according to the Ministry of Social and Family Development. Even among those over 65, the group most likely to need one, only 197,000 (roughly 1 in 4) have done so.

Registrations have climbed sharply since the process moved online and legacy-planning campaigns went island-wide, but many still haven’t. And if even over-65s sit at just 1 in 4, uptake among younger adults is lower still. It’s the same age gap we see with CPF nominations: the young assume there’s time.

There’s now one less excuse. From 1 April 2026, the LPA Form 1 application becomes permanently free for Singapore citizens, removing the fee that put some people off.

And awareness isn’t really the problem. A 2026 SMU study of older Singaporeans found close to 70% knew about the LPA, yet only about a third had made one. More tellingly, more than half of those without one, and with no plans to make one, wrongly assumed their children could automatically act for them if they lost capacity. They can’t, which is exactly what an LPA is for.

An LPA is also just one piece of the “while you’re alive” puzzle. If you want a say in your future medical care, two related tools sit alongside it: Advance Care Planning, where you record your care wishes and talk them through with your family, and the Advance Medical Directive, a legal form stating you don’t want extraordinary life-sustaining treatment if you’re terminally ill and unconscious.

More than 87,000 Singaporeans have completed an Advance Care Plan, according to the Ministry of Health, and here too 94% are aged 50 and above. Neither tool deals with money, but both spare your loved ones from having to guess.

How to Check for Unclaimed Money in Singapore

If you think a late relative left money behind, or you simply want to be sure none of yours is stuck, here’s where to look.

- Government agencies: the unclaimedmonies.gov.sg register lists money held across ministries, statutory boards, and other public bodies, including tax refunds and money due to beneficiaries of estates.

- CPF and estate monies: the Public Trustee’s Office holds un-nominated CPF and the estates of people who died without a nomination. Next-of-kin can apply online, and there’s no deadline to claim.

- Insurance: since the LIA register closed, there’s no central search. You’ll need to contact each insurer you think held a policy directly.

- Your own money: while you’re at it, log in to your CPF account with Singpass to confirm your nomination, and use MyLegacy@LifeSG to review your plans, so your own money never ends up on a list like these.

One thing to know: turning up in a register doesn’t automatically make the money yours. You’ll need documents proving you’re the rightful owner before any agency will release it.

What This All Means for You

Put the numbers together and a pattern shows up. Most of what goes unclaimed or ends up in the wrong hands isn’t down to bad luck. It’s down to paperwork that never got done.

Hundreds of millions in CPF sit with the Public Trustee, younger Singaporeans skip their nominations and wills, and a growing pile of digital assets leaves no trail at all.

The good news is how fixable this is. The core of estate planning comes down to a handful of steps, and most cost nothing.

- Make your CPF nomination, and review it after big life events like marriage or a new child

- Name beneficiaries on your insurance policies

- Write a will, and look over it every few years

- Consider a Lasting Power of Attorney so someone you trust can act for you if you lose capacity

- Record your healthcare wishes through Advance Care Planning and an Advance Medical Directive

- Keep a simple, up-to-date record of what you own and where it sits, such as our free FinSnap template

You don’t need to be wealthy or old to start, and none of it takes long. And if you’d like help putting it all together, our FullCircle financial planning session gives you a clearer picture of where you stand and what to prioritise, across protection, retirement, and estate planning.

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.