Most of us plan for death with insurance and a will. Far fewer plan for the stretch in between: still alive, but too unwell to speak for ourselves.

A sudden illness or a bad fall can strip away your ability to make decisions, sometimes with no warning at all. If that day comes and you’ve left no instructions, your loved ones and your doctors are left guessing at what you’d have wanted, often during the hardest moment of their lives.

Advance Care Planning is how you spare them that guesswork. And a healthy Singaporean can now start one online, for free, in an afternoon. Here’s how it works, and how it fits with the two legal documents that sit alongside it.

Too Long; Didn’t Read

Advance Care Planning (ACP) is an ongoing conversation about how you’d want to be cared for if you ever couldn’t speak for yourself. It isn’t legally binding. It’s a guide for your family and care team, and it lets you appoint up to two Nominated Healthcare Spokespersons to voice your wishes.

Two legal documents work alongside it. An Advance Medical Directive (AMD) lets you refuse extraordinary life-sustaining treatment if you’re ever terminally ill and unconscious. A Lasting Power of Attorney (LPA) lets you appoint someone to make welfare and money decisions if you lose mental capacity.

Since 13 June 2025, generally healthy Singaporeans aged 21 and above can complete their ACP online through the free myACP tool, with no need to see a facilitator. Read on for how all three pieces fit together.

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

What Is Advance Care Planning (ACP)?

Advance Care Planning is the process of thinking through, and sharing, how you’d want to be cared for in future if a serious illness or injury left you unable to make or communicate your own decisions.

It isn’t a single form. According to the Ministry of Health, ACP is an ongoing process of planning for your future health and personal care, so your loved ones and healthcare team understand your beliefs, values, and the kind of care you’d want when you can’t tell them yourself.

If you couldn’t communicate, how would anyone know whether you’d want every possible intervention, or whether you’d rather be kept comfortable and allowed to go naturally? Without your wishes written down somewhere, they’re left to guess, and then to live with having guessed.

ACP is for everyone, not just the elderly or the seriously ill. Anything can happen at any age, and the point is to plan while you’re well enough to think it through calmly.

Worth being clear from the start: an ACP isn’t legally binding. It guides the people making decisions for you, but it doesn’t compel them the way a legal document does. That’s exactly why it works best paired with the two legal tools we’ll cover below.

Why ACP Matters

At some point, most of us will face a decline in health. Maybe slowly, maybe overnight. And it won’t only fall on you. It falls on the people who’d have to step in.

Planning ahead does a few valuable things:

- It keeps your values and beliefs in the picture when your family and doctors are weighing up treatment.

- It takes the guesswork, and the second-guessing, off your loved ones’ shoulders.

- It names someone to speak for you, so your family isn’t left arguing over what you “would have wanted”.

- It lets you set out, in advance, how far you’d want treatment to go if recovery is no longer realistic.

And more people are acting on it. More than 87,000 Singaporeans have now completed an Advance Care Plan, though 94% are aged 50 and above, so younger adults still lag behind, as our roundup of legacy and estate planning statistics in Singapore shows.

ACP, AMD and LPA: How the Three Tools Differ

Here’s where a lot of people get tangled up. ACP, AMD and LPA are three separate things that work together, not one big thing with three names. The quickest way to see it is side by side.

| ACP | AMD | LPA | |

|---|---|---|---|

| What it is | A plan and conversation about your future care wishes | A directive refusing extraordinary life-sustaining treatment | A document appointing someone to act for you |

| Covers | Your care values and preferences, end of life included | Terminal illness when you’re unconscious | Personal welfare and/or property and money |

| Legally binding? | No, it’s a guide | Yes | Yes |

| You appoint | Up to 2 Nominated Healthcare Spokespersons | No one (it’s your own instruction) | One or more donees |

| How to do it | Online via myACP or a facilitator, free | Through a doctor, with two witnesses, registered with MOH | Online via OPGO with Singpass |

In plain terms: your ACP captures what you’d want and who should speak for you. Your AMD is a narrow, legal “no” to machines that would only prolong your dying. Your LPA hands day-to-day welfare and money decisions to someone you trust. You can do any one of them on its own, but most people are best off with all three in place.

The Advance Care Plan Itself (and the New myACP Tool)

At its simplest, an ACP starts as a chat with your family over dinner. Writing it down matters, though, because memories fade and people recall things differently.

A documented plan records the medical treatments you would or wouldn’t want, your priorities between comfort and life-sustaining care, and preferences around daily care, hygiene, companionship, and any religious needs. It’s then kept on file so your healthcare team can refer to it when the time comes.

Appointing a Nominated Healthcare Spokesperson (NHS)

A central part of ACP is naming a Nominated Healthcare Spokesperson (NHS), the person who’ll voice your care preferences if you can’t speak for yourself. You can appoint up to two people, according to MyLegacy@LifeSG. Choose someone who understands your wishes and whom you trust to honour them, even under pressure from other relatives.

It’s worth being clear on what an NHS is and isn’t. Your spokesperson voices your wishes but has no legal authority to make decisions for you. An LPA donee, by contrast, holds legal power to act. That’s why, if you also make an LPA, your NHS and your LPA donee for personal welfare should ideally be the same person. If they’re different people, you risk them pulling in different directions on a healthcare decision, which is the opposite of what you set out to avoid.

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

Doing your ACP online with myACP

This is the biggest change in recent years. Until 2025, making an ACP meant booking time with a trained facilitator. Now there’s a free, self-service option.

Launched in July 2025 by MOH, the Agency for Integrated Care and GovTech, myACP lets generally healthy Singaporeans document their care preferences entirely online, with no facilitator needed. You access it through the MyLegacy@LifeSG portal using Singpass, then work through your preferences and send digital invitations to the people you’ve named as your NHS.

A few conditions apply. myACP is open to those aged 21 and above with no existing serious illness, such as cancer or dementia. Because it runs on Singpass, it’s available to Singapore Citizens and PRs alike. If you do have a serious illness, your ACP should be done with a trained facilitator who can tailor it to your medical situation. And if you’d simply prefer face-to-face guidance, you can do it in person through an ACP provider listed on the same portal.

Keeping it up to date

An ACP isn’t a “do it once and forget it” task. Your views can shift after a major life event, a new diagnosis, a marriage or divorce, or simply with age. It’s worth revisiting your plan every few years, or whenever something significant changes, and updating it so it still reflects what you’d want.

Advance Medical Directive (AMD): Refusing Futile Treatment

The AMD is the most misunderstood of the three, so it’s worth being clear about what it does.

An Advance Medical Directive (AMD) is a legal document you sign in advance to tell the doctor treating you that, if you ever become terminally ill and unconscious, you don’t want any extraordinary life-sustaining treatment used to artificially prolong your life. It lets you die naturally and with dignity when that point is genuinely reached.

It’s narrower than most people assume. An AMD isn’t euthanasia, which is illegal here, and it isn’t a general “do not treat” order. It applies only to that one end-of-life situation, and ordinary care like pain relief and nursing carries on regardless. You make one through a doctor with two witnesses, register it with MOH, and you can revoke it at any time.

For the full process, the witness rules, the safeguards that stop it being acted on lightly, and the common misconceptions, see our dedicated guide to the Advance Medical Directive in Singapore.

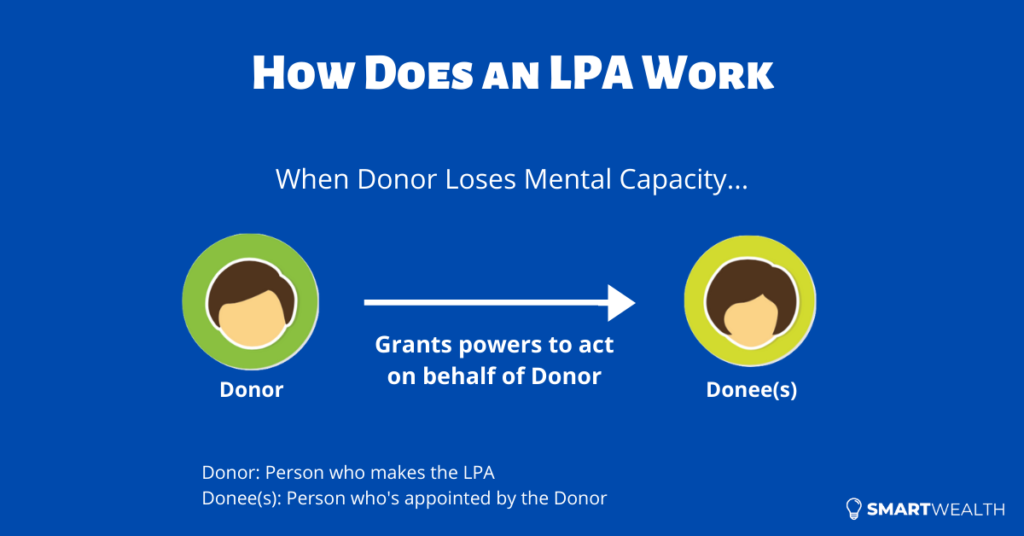

Lasting Power of Attorney (LPA): Who Acts for You

While an AMD covers one specific end-of-life decision, an LPA covers much wider ground: the everyday decisions that pile up while you’re alive but lack mental capacity.

With an LPA, you (the “donor”) appoint one or more people (your “donee”) to act in your best interests if you can no longer decide for yourself. A donee can be given power over your personal welfare, such as your care and where you live, your property and affairs, such as your bank accounts and bills, or both. It’s a legal document, so your donee genuinely has the authority to step in.

This is where ACP and LPA dovetail. Say you’ve done an ACP and named an NHS, but never made an LPA. If you lose capacity, your spokesperson can voice your care wishes, but nobody can legally access your bank account to pay your medical bills. Your family would have to apply to court for a Deputyship order, which is slower, costlier, and more stressful than an LPA would have been.

Flip it around. If you’ve made an LPA but never done an ACP, your donee has the authority to act, but little idea of what you’d actually have wanted. They’re deciding in the dark.

That’s why the two belong together, and why your NHS and your personal welfare donee should ideally be the same person. For the online process, the 2026 fees, and exactly what a donee can and can’t do, see our full LPA guide.

How ACP, AMD and LPA Fit Together

It helps to think of the three as covering different jobs at different moments:

- Your ACP records your wishes and names who should speak for you. It guides, but doesn’t bind.

- Your AMD is a specific, legally binding instruction for one situation: terminal illness with unconsciousness.

- Your LPA gives someone legal authority to handle your welfare and finances across the board.

What happens if they seem to overlap or clash? In practice they rarely do, because each governs a different decision. Your AMD, being a legal directive you made yourself, takes precedence on the specific question of refusing extraordinary life-sustaining treatment, your donee cannot override it. Your LPA donee and NHS handle the broader and more everyday calls, guided by the wishes you set out in your ACP. Keeping the same trusted person across these roles is the simplest way to avoid any friction.

None of the three replaces the others, and none is only for the old or the sick. Together, they make sure that if you ever can’t speak for yourself, the right person can act and your wishes still carry weight.

Where ACP Sits in Your Wider Plan

Advance care planning tends to matter most in that grey zone, neither fully well nor gone. It’s an uncomfortable thing to picture, but it’s exactly the scenario worth preparing for. And it doesn’t stand alone. Two other areas sit right beside it.

The first is financial planning. You might have made your care wishes crystal clear, but if you don’t have proper insurance in place, a hospitalisation plan, life cover, and long-term care support through something like CareShield Life, the care you wanted may be hard to fund. And without savings and a retirement plan, there may be little to fall back on in your later years.

The second is estate planning. Once you lose mental capacity, the window for arranging things closes. You can no longer make a CPF nomination, an insurance nomination, or a will. And if you die without a will, your assets are divided by a fixed legal formula rather than according to your wishes.

Care planning, financial planning, and estate planning all feed into one another. Sorted together, they cover you across every stage, while you’re well, while you’re unable, and after you’ve gone.

The Bottom Line

Advance Care Planning, and the AMD and LPA that sit beside it, are some of the kindest things you can do for the people who’d otherwise have to make impossible choices on your behalf. They take a little time and almost no money, and now that ACP can be done online for free, there’s one less reason to put it off.

If you’ve been meaning to get to it, treat this as your nudge. Start the conversation with your family, complete your ACP, and round it out with an LPA and the estate planning basics: a will, a CPF nomination, and an insurance nomination. Each covers something the others can’t.

And if you’d rather map out the whole picture at once, protection, retirement, and estate planning together, that’s what a session like FullCircle is for.

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.