We plan for death with insurance and a will. Far fewer of us plan for the in-between: being alive, but no longer able to make our own decisions.

A stroke, accident, or dementia can take away your mental capacity in an instant. And here’s what catches families off guard: even your spouse or children can’t simply step in to manage your money or your care. Without the right document in place, no one has the legal authority to act for you.

That document is the Lasting Power of Attorney (LPA), and making one is now easier and cheaper than ever.

Here’s everything you need to know, including the exact steps to make one.

Too Long; Didn’t Read

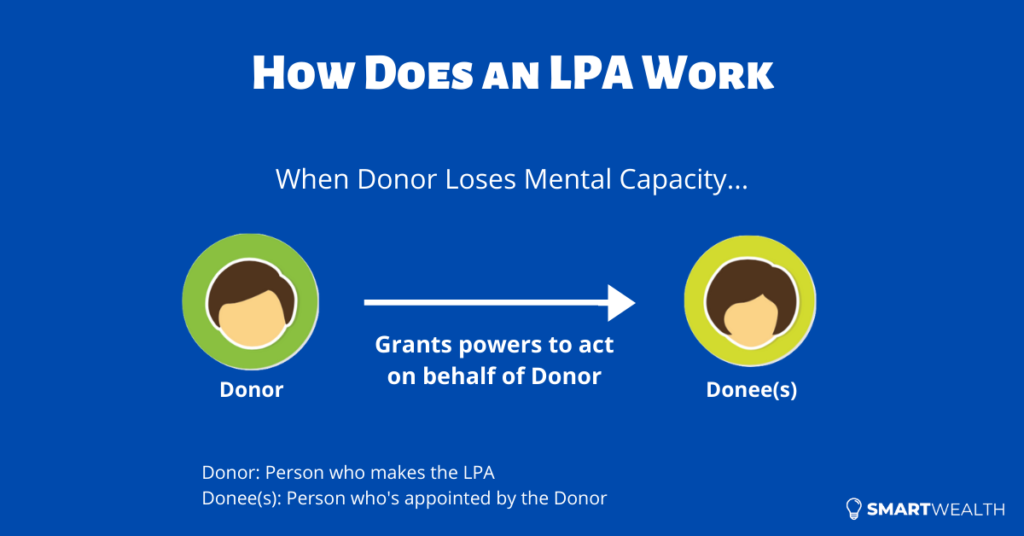

An LPA lets you appoint someone you trust (your “donee”) to make decisions on your behalf if you ever lose mental capacity, over your personal welfare, your property and finances, or both.

Without one, your loved ones can’t just take over. They’d have to apply to court for a Deputyship order, which is slower, more stressful, and more expensive than making an LPA in the first place.

It’s now done online through OPGO using Singpass, and you’ll need a Certificate Issuer (a doctor, lawyer, or psychiatrist) to certify it. As of 2026, the application fee is free for Singapore Citizens, $30 for PRs, and $160 for foreigners, plus a separate fee to your Certificate Issuer.

There’s more to it though, including what your donee can and can’t do. Read on for the full picture.

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

What Is a Lasting Power of Attorney (LPA)?

A Lasting Power of Attorney (LPA) is a legal document that lets you (the “donor”) appoint one or more people (your “donee”) to make decisions and act for you if you lose mental capacity one day.

You can give your donee power over two broad areas:

- Personal welfare, such as your healthcare, where you live, and your daily care

- Property and affairs, such as your bank accounts, paying your bills, and managing your CPF monies

You can grant power over one area or both, and you don’t have to give the same person both jobs.

The key word is capacity. Under the Mental Capacity Act, you lack it when you can’t make a decision for yourself because of an impairment in the way your mind or brain works, whether permanent or temporary. Common causes include a stroke, dementia, mental illness, or a head injury.

Capacity also isn’t all-or-nothing. It’s assessed for a specific decision at a specific time, and the law assumes you have it unless proven otherwise. Someone might manage their daily shopping but not a complex property sale. Your LPA only comes into play for the decisions you genuinely can’t make yourself.

Why Making an LPA Matters

You can only make an LPA while you still have mental capacity. Once it’s gone, that door closes, and your family is left with a much harder path.

Picture the common scenario: you’re in a coma after an accident. Bills need paying, treatment decisions need making, and your accounts need accessing to fund your care. None of it happens automatically. Even though the money is for your own benefit, your next-of-kin has no legal right to touch it, because your assets remain yours alone.

With an LPA, the person you chose simply steps in. Without one, your family has to go to court.

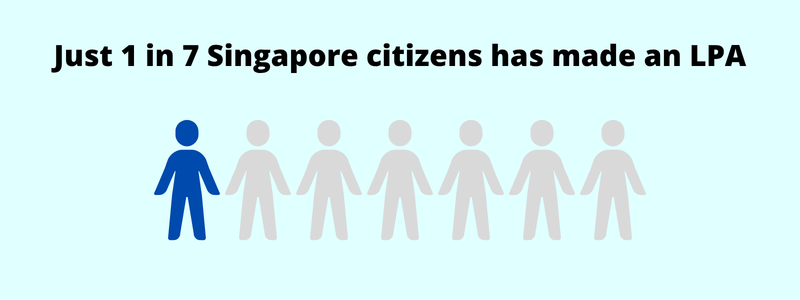

Yet uptake is still low. Only about 1 in 7 Singapore citizens have made an LPA, and even among over-65s just 1 in 4 have, going by the latest LPA uptake figures.

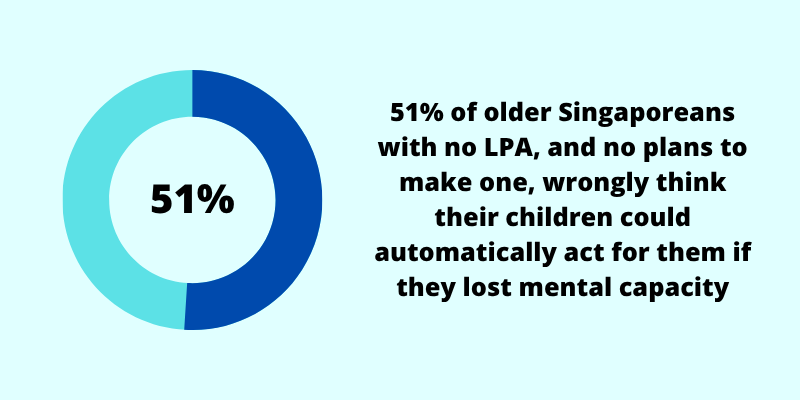

More than half of older Singaporeans without one wrongly assume their children could automatically step in, exactly the gap an LPA closes.

What happens if you don’t have one

They’d need to apply to the Family Justice Courts for a Deputyship order, appointing a “deputy” to decide for you. It works, but it’s heavier than an LPA in three ways.

It costs more. Court filing fees are modest, $40 to $50 for the simplified process and $300 to $500 for the standard one, but those exclude the doctor’s medical report and, usually, lawyer’s fees, which is where the real expense adds up.

It takes longer. A simplified application usually takes four to six weeks, a standard one three to four months. That’s time your family spends in limbo while bills go unpaid.

It’s an ongoing commitment. A deputy is supervised by the Public Guardian and generally has to submit regular reports. The court also decides who gets appointed, which may not be who you’d have chosen.

An LPA sidesteps all of this, and from 2026 it’s free for Singapore Citizens to make.

Who Can Be a Donor and a Donee

To make an LPA as a donor, you must be at least 21, have mental capacity, and not be an undischarged bankrupt if you’re granting powers over property and affairs.

Your donee is the person you’re trusting with all this. The requirements:

- At least 21 years old

- Reliable, competent, and someone you genuinely trust

- A personal welfare donee must be an individual (not a company)

- A property and affairs donee can be an individual (who must not be bankrupt) or a licensed trust company

With the standard Form 1, you can appoint up to two donees, plus one replacement donee as backup. For more than that, you’ll need Form 2.

No one suitable to appoint? You can engage a vetted professional through the Professional Deputies and Donees scheme, made up of lawyers, doctors, accountants, social workers, and others who act as your donee for a fee.

What your donee can do

A personal welfare donee can decide where you live, your day-to-day care, what you eat and wear, who you have contact with, and your healthcare arrangements (within limits we’ll come to). A property and affairs donee can operate your bank accounts, pay your expenses, collect income owed to you, handle your tax, manage your CPF monies, and deal with your property.

A point most guides skip: you can appoint different donees for each area, say your sister for healthcare and your spouse for the money. Just note that some decisions, like a move into a nursing home, touch both, so donees with different powers will need to cooperate.

What your donee cannot do

This is the part almost every guide leaves out. Even a wide-ranging LPA has firm legal limits. Per the LPA guide, your donee cannot:

- Decide anything you still have the capacity to decide yourself

- Consent to or refuse your healthcare treatment, unless you expressly granted that power

- Consent to or refuse life-sustaining treatment, which can’t be handed to a donee at all

- Make or revoke a CPF or insurance nomination for you

- Gift your property, unless you expressly allowed it

- Make or execute your will

The law also bars a donee from certain decisions whatever your LPA says, including consenting to marriage or divorce, consenting to an adoption, adopting or renouncing a religion, and making or revoking an Advance Medical Directive.

So an LPA is powerful, but it isn’t a blank cheque. It covers everyday welfare and financial decisions, not the deeply personal or end-of-life ones, which is why it works alongside a will and an Advance Medical Directive rather than replacing them.

Jointly vs jointly and severally

If you appoint more than one donee for the same area, you decide how they act:

- Jointly: they must agree and act together. A safeguard, but it risks deadlock or delay if one disagrees or is away.

- Jointly and severally: they can act together or alone. Far more practical day to day, though any one donee can then act without the others.

If you don’t specify, the law assumes jointly. It’s worth a real think rather than leaving it to the default.

Replacement donees and what cancels an appointment

A replacement donee is your backup, stepping in if your original donee can no longer act. It’s smart to appoint one, because a donee’s appointment can be cancelled automatically when:

- The donee (or you) passes away

- You and your donee divorce or have your marriage annulled, unless your LPA says otherwise

- The donee becomes bankrupt (this ends only their power over property and affairs)

- The donee loses capacity, or formally refuses the role

That divorce rule catches people out. Appoint your spouse, later divorce, and their appointment falls away unless you stated otherwise. Without a replacement, your LPA could be left with no one to act, sending your family to court after all.

A donee’s duties

A donee doesn’t get a free hand. Under the Mental Capacity Act, they must act in your best interests, help you make your own decisions where you still can, and choose the least restrictive option. Abuse that trust, and the Public Guardian can investigate and apply to court to remove them.

LPA Form 1 vs Form 2

| Form 1 | Form 2 | |

|---|---|---|

| Type | Standard form | Customisable form |

| Powers | General, with basic restrictions | Tailored, specific powers you define |

| Donees | Up to 2 donees and 1 replacement | More than 2 donees and replacements |

| Needs a lawyer? | No, you fill it in yourself | Yes, a lawyer drafts the clauses |

| Best for | Most people | Complex wishes or intricate estates |

For most people, Form 1 is all you need. In fact, 98% of Singapore Citizens who have made an LPA used Form 1. You’d only reach for Form 2 to grant unusual powers, appoint more donees, or add custom conditions, and because a Singapore-qualified lawyer must draft it, it costs more.

How Much Does an LPA Cost in Singapore? (2026)

There are two costs: the application fee to register your LPA, and the professional fee for your Certificate Issuer.

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

Application fees

This is the big news of 2026. From 1 April 2026, Singapore Citizens can make a Form 1 LPA completely free of charge, now a permanent arrangement rather than a temporary waiver. From 1 May 2026, fees were also reduced for everyone else.

| Form 1 | Form 2 | |

|---|---|---|

| Singapore Citizens | Free | $30 |

| Permanent Residents | $30 | $30 |

| Foreigners | $160 | $160 |

Cancelling a registered LPA costs $28. No refund is given once you submit, even if the application is later rejected, so get the details right first.

Certificate Issuer fees

Your Certificate Issuer charges a separate professional fee, which the government doesn’t set. As at June 2025, the published fee ranges for the 20 most visited Certificate Issuers, for Form 1 certification, were:

| Certificate Issuer | Median fee | Range |

|---|---|---|

| Accredited doctors | $47.50 | $24 to $500 |

| Lawyers | $104.50 | $50 to $600 |

| Psychiatrists | $350 | $24 to $1,500 |

These exclude consultation charges and GST. For a standard Form 1, an accredited doctor is usually the most affordable. If cost is a real concern, some organisations offer pro bono or means-tested certification, such as Potter’s Place Community Services Society and the Mount Alvernia Outreach Medical Clinic at Enabling Village.

In practice, a Singapore Citizen making a Form 1 today pays nothing to register and roughly $25 to $50 to an accredited doctor.

How to Make an LPA Online (Step-by-Step)

This is what’s changed most. The whole process now runs through OPGO, the online portal that replaced the old paper-and-post system. You’ll need Singpass, both for yourself and your donees.

Step 1: Draft your LPA on OPGO

Log in with Singpass and select “Apply for an LPA”. Your details are pulled in from Myinfo, so you mostly just check them. Add your donee(s), choose each one’s powers, set how they should act, and add a replacement donee if you have one. The draft is then routed to your donees electronically.

Step 2: Your donee(s) accept their appointment

Each donee gets an SMS and email to log in with their own Singpass and accept the role. Your application can’t move forward until every donee, and your replacement, has accepted. So give them a heads-up.

Step 3: Visit a Certificate Issuer to certify

Once your donees have accepted, you see a Certificate Issuer in person. They check you understand what you’re doing and aren’t being pressured, then you both sign the LPA digitally using the Singpass app, so set up digital signing beforehand. The Certificate Issuer then submits it for registration.

Step 4: Pay the application fee online (if any)

You’ll be prompted to pay any fee through OPGO by Visa or Mastercard. Singapore Citizens making a Form 1 pay nothing. Cheques and cash are no longer accepted.

Step 5: Registration

There’s a mandatory three-week waiting period to allow objections. If there are none, your LPA is registered, with processing taking about eight working days on top. You and your donees can then view it anytime in OPGO.

Two notes: paper applications are now accepted only in limited exception cases, and you can alternatively start a Form 1 through MyLegacy@LifeSG, which guides you through the same process.

The Certificate Issuer: What They Do and How to Choose One

The Certificate Issuer is a built-in safeguard. They confirm you understand the LPA and the powers you’re handing over, and that no one is defrauding or pressuring you.

Only three professionals can act as one: an accredited medical practitioner, a practising Singapore lawyer, or a registered psychiatrist. To keep the safeguard meaningful, the law disqualifies anyone with a conflict of interest, so it can’t be a family member, your donee (or their family member), your business partner, or someone who runs the care facility you live in.

The easiest way to find one is the Health Appointment System, which lets you book directly and shows each issuer’s fee and earliest slot upfront.

How an LPA Is Activated

A common misunderstanding is that an LPA gives your donee power the moment it’s registered. It doesn’t. Your donee can only act once a registered doctor has certified that you’ve lost the capacity to make the decision in question. Until then, your LPA sits dormant.

When that happens, your donee presents your electronic LPA, sent through their OPGO dashboard, to whichever institution they’re dealing with, along with the medical report. Each organisation sets its own requirements, so once your LPA is registered, it helps to let your doctor, bank, the CPF Board, and insurers know it exists.

One reassuring point: loss of capacity can be temporary. If you recover, your donee steps aside and you decide for yourself again, with the LPA staying valid for next time.

How to Change or Revoke an LPA

You can revoke your LPA anytime while you still have mental capacity. To do it properly, notify both your donee(s) and the Public Guardian, and a cancellation fee applies. To change donees or powers, simply revoke the old LPA and make a new one.

That “while you still have capacity” point is the whole reason not to delay. Once capacity is lost, the LPA is locked in as it stands.

And if a donee misbehaves after you’ve lost capacity, perhaps acting dishonestly, the Public Guardian can investigate and apply to court to strip them of their powers. Such cases are uncommon, but the safeguard is there.

LPA vs a Will: How They Fit Together

People often muddle up an LPA and a will, but they cover different moments. A will takes effect when you die and says who inherits your assets. An LPA takes effect while you’re alive but lack capacity and says who manages your affairs. Neither does the other’s job, which is why you generally want both.

Think of it as covering two gaps. An LPA handles “alive but unable”. A will, plus a CPF nomination since a will can’t touch your CPF, handles “after death”. Leave either out and that part falls back on a default process, a court Deputyship while you’re alive or intestacy law once you’ve gone.

The LPA also sits alongside Advance Care Planning and the Advance Medical Directive, which cover your medical and end-of-life wishes. These are three distinct but related tools. Together with your broader estate plan, they make sure the people you trust can act and your wishes are followed.

The Bottom Line

An LPA is one of the simplest, highest-value things you can do for the people who’d pick up the pieces if you ever lost mental capacity. It takes little effort to set up, it’s now free for Singapore Citizens, and it spares your family a slow, costly trip to court at the worst possible time.

If you’ve been meaning to get to it, this is your sign. Then round out the picture: a will, a CPF nomination, an insurance nomination, and for larger estates, a trust. Each reaches something the others can’t, so your wishes, not a default formula, decide what happens.

And if you’d rather map out the whole picture, protection, retirement, and estate planning together, that’s what a session like FullCircle is for.

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.