Many parents still hope to send their children to university, even as the world puts more weight on skills and talent.

A degree still counts for a lot, and many graduates value what it gave them, the way of thinking and the people they met, as much as the certificate itself. So if university is the plan for your child and you are wondering where the money will come from, this guide is for you.

In Singapore, there are six main ways to fund a university education: bursaries, scholarships, loans, savings, investments, and child education endowment plans. Most families end up combining several. We explain how each one works, with the pros and cons, below.

Funding is only one piece of the wider picture. For the full cost breakdown from preschool to degree, and how much to save each month, see our complete guide to child education planning in Singapore.

How Much Does a University Education Cost?

How Much Does a University Education Cost?

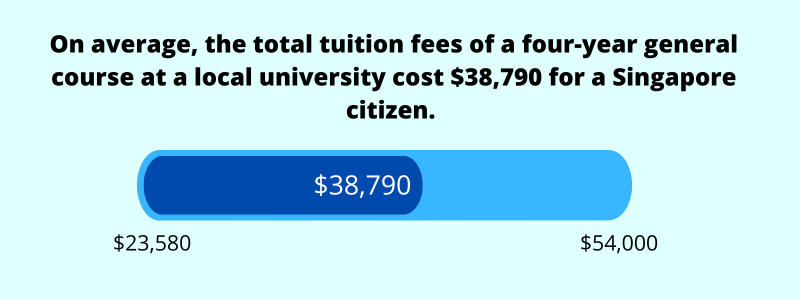

A four-year degree at a local autonomous university costs a Singapore citizen an average of $38,790 in tuition fees as of 2026, after the MOE Tuition Grant. The range runs from about $23,580 at SIT to $54,000 at SUTD, and professional degrees cost far more. A law degree is around $51,000 over four years, and medicine at NUS is about $166,000 over five.

That is tuition alone. Add roughly $43,100 in living expenses over four years for a student staying in hostel, and the true bill for a local degree climbs to about $81,890.

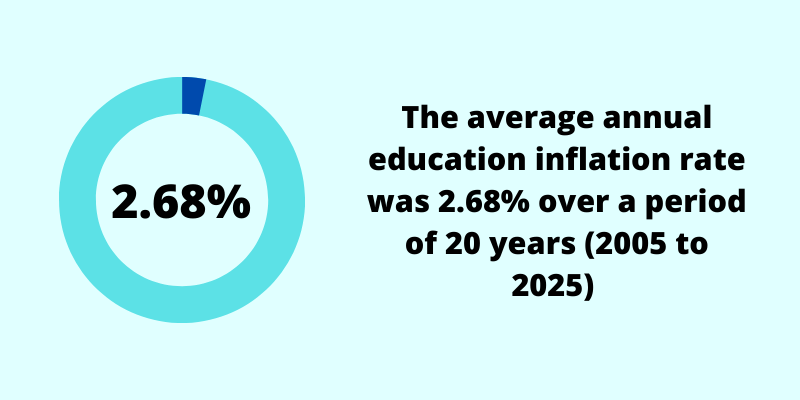

These are today’s prices. Because education costs in Singapore have risen 2.68% a year over the past two decades, faster than general inflation, the figure your child faces will be higher still.

To project the cost for your child’s age and estimate a monthly savings target, use our free education fund calculator.

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

1) Bursaries

Bursaries help Singapore citizens who need a hand with tuition fees. There are two broad types: government-funded and university-funded.

The main government bursaries for university students are the Higher Education Community Bursary and the Higher Education Bursary. Both are income-tested on either gross household income (GHI) or per capita income (PCI), and the amount rises as household income falls. From Academic Year 2026, the Ministry of Education raised the income ceilings and the payouts, so more middle-income families now qualify.

| Monthly household income (from AY2026) | Annual bursary for full-time undergraduates |

|---|---|

| GHI up to $4,000, or PCI up to $1,000 | $6,300 |

| GHI $4,001 to $5,500, or PCI $1,001 to $1,375 | $5,100 |

| GHI $5,501 to $9,000, or PCI $1,376 to $2,250 | $3,250 |

| GHI $9,001 to $12,000, or PCI $2,251 to $3,000 | $1,350 |

Source: MOE government bursary quanta for autonomous universities, effective AY2026. Figures are for general degrees and exclude Medicine and Dentistry, which have their own higher bursary tiers.

Even at the top tier, a bursary rarely covers the whole bill. For a general degree, the largest award of $6,300 a year works out to roughly 75% of subsidised tuition, so a middle-income family will still have fees left to cover, before living costs and education inflation are counted.

Two more things to note. Government bursaries are awarded yearly, so your child re-applies each year and the amount can change as your household circumstances shift. University-funded bursaries, paid from donor and alumni gifts, are also income-assessed, and recipients may be asked to help at university events or meet donors in return.

2) Scholarships

A scholarship is many parents’ dream, since it can cover most or all of the cost of a university education. BrightSparks is a useful platform that lists scholarships students may be eligible for and how to apply.

Most scholarships come with strings attached, though. Once your child signs, they usually commit to a minimum bond of a few years and have to maintain a certain grade point average.

Problems arise when a student finds the course is not for them, decides their values no longer match the sponsoring organisation, or struggles to keep up the required grades. Breaking a bond can cost anywhere from $50,000 to $200,000, which lands back on the parents’ shoulders, on top of the strain it puts on the child. Because a scholarship is never guaranteed and can be costly to exit, it belongs in your plan as a welcome bonus, not as the foundation.

3) Loans

For parents who want their child to share the cost, or who prefer to keep their own savings intact, loans are a common route. The two main options are the government student loan and the CPF Education Loan Scheme.

The Higher Education Student Loan (HESL)

This is the big change for 2026. From 1 July 2026, the Higher Education Student Loan replaced the old Tuition Fee Loan and Study Loan for students at the autonomous universities, polytechnics, ITE, and arts institutions. Students already on a Tuition Fee Loan or Study Loan can carry on as before, with no action needed.

The HESL has two parts. The base provision covers up to 90% of subsidised tuition fees for a Singapore citizen. On top of that, a means-tested provision can cover the remaining fees plus a living allowance for citizens whose per capita household income is $3,500 or less. Your child chooses which parts to take up, so they can borrow for fees only, living costs only, or a combination.

Like the scheme it replaced, the HESL is interest-free while your child is studying, with interest starting only after graduation. The standard rate is the three-month compounded Singapore Overnight Rate Average (3M SORA) plus 1.5 percentage points, revised twice a year, so it moves with market rates rather than sitting at a fixed number. One difference worth flagging: the maximum repayment period is now 10 years, shorter than the up-to-20 years the old Tuition Fee Loan allowed.

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

CPF Education Loan Scheme

If you have enough in your CPF Ordinary Account, the CPF Education Loan Scheme lets you use those savings to pay your child’s subsidised tuition fees at approved local institutions. It solves a cash-flow problem without touching your take-home pay.

Remember that this is a loan, not a free withdrawal. Your child must repay the amount used plus the accrued interest in cash, starting one year after they graduate. Every dollar taken out of your OA also stops earning CPF interest for your own retirement, so weigh this route carefully against your longer-term needs.

4) Savings

Parents can also simply save towards the cost in cash, in a dedicated account topped up each month.

Cash has one big advantage: liquidity. Your money is not locked away, and it is hard to get wrong. The catch is that it is tempting to dip into for other things before your child reaches university, and bank interest has historically trailed education inflation, so cash alone slowly loses ground against the target over a 20-year horizon. It works best for near-term needs and as the stable core of a longer plan.

5) Investments

Parents comfortable with markets may plan to fund part of the cost through investments in shares, exchange-traded funds, or unit trusts. Over a long runway, this route offers the best odds of outpacing education inflation.

The trade-off is volatility. Markets can fall exactly when the fees are due, and there have been cases of investors losing their capital. A common approach is to invest while your child is young, then move progressively into safer assets in the final years before university, so a bad year does not derail the plan. Returns are never guaranteed, so relying on investments alone carries real risk.

6) Child Education Endowment Plans

Finally, child education endowment plans are a popular choice. An endowment plan is an insurance savings plan that helps you commit to saving regularly, and is usually capital guaranteed at maturity, which is timed around university entry. You can choose shorter or longer premium terms.

The projected return is modest, though generally better than leaving the money in a bank account. And if your child ends up not needing the fund, you keep the option to redirect it, whether towards your own retirement or a gift for their wedding, first home, or graduation.

The weaknesses are worth stating plainly. Returns are typically lower than investing, surrendering early usually means a loss, and the plans are rigid if your child’s path changes. In my opinion, they suit savers who value certainty and forced discipline over maximum returns, but they are one option among several, not the automatic answer.

Which Route Is Right for You?

There is no single best way to fund a university education. Most families blend a few: bursaries and scholarships where they qualify, a core of savings or investments built up over the years, and a loan to bridge any gap at the end.

One principle holds across all of them. You can borrow for a degree, but nobody lends for your own retirement, so avoid funding your child’s education at the expense of your retirement savings. Whatever mix you choose, starting early is what does most of the work, since it gives compounding, and your savings, the most time.

If you would like to see how education fits alongside your protection, retirement, and estate plans, our team can walk through it with you as part of a wider look at planning for your child’s education.

Knowing the six options is the easy part. The harder question is which mix fits your income, timeline, and risk appetite, and how to combine savings, investments, and an endowment plan so they work together. That is what comprehensive financial planning is for: a licensed consultant helps you choose and combine the instruments that save and invest more efficiently, without shortchanging your own retirement.

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.