Why is it so crucial to set personal financial goals?

Your finances are a key resource that enables you to lead the life you desire. They can help you accomplish important milestones such as attaining a house, getting married, having children, and paying for your children’s education. Having strong finances can also grant you the capacity to travel, indulge in other leisure, or start a business, just to list a few examples.

As such, in order to live your life to the fullest, it is essential to plan your financial goals such that they are aligned with your life goals. Otherwise, you may wind up lacking the monetary resources to fund your activities, which would hinder you from attaining your desired lifestyle.

In this article, there are nine examples of personal financial goals that may be relevant to you.

9 Examples of Personal Financial Goals: Short, Medium & Long Term

SIDE NOTE

Most people's finances aren't a plan. They're a collection of separate decisions: a policy bought years ago, investments that don't talk to each other, a will that's still on the to-do list.

If that sounds familiar, there's a fix that doesn't require becoming a finance expert.

Here's the 7-step framework we use to organise everything into one system.

Short term goals

Short term financial goals are the most urgent and should thus be prioritised first.

At the same time, they are achievable within a shorter time frame and can serve as a good foundation for subsequent mid to long term goals.

Achieving your short term personal financial goals will also give you a peace of mind from immediate or ad hoc expenses that crop up, allowing you to shift your focus towards mid and long term goals.

1) Adopt good money management habits

Having healthy money management habits is perhaps the most vital prerequisite to achieving your other financial goals.

This includes setting a budget and sticking to it in a disciplined manner. Your budget should include considerations about your expenses (separated into needs versus wants), debt repayments, savings, investments, and insurance.

There are numerous financial experts who attest to different ways of budgeting money, including the 50-30-20 allocation popularised by Senator Elizabeth Warren. The 50-30-20 rule basically recommends that you take your after-tax income and allocate 50% on needs, 30% on wants, and 20% on savings or paying off liabilities such as debt.

However, as you can see, this may not be suitable for everyone. You should thus take the time to consider your own financial situation and set a feasible budget that would allow you to make the most of your money. This can be adjusted over time, as your income or your mid to long term financial goals change.

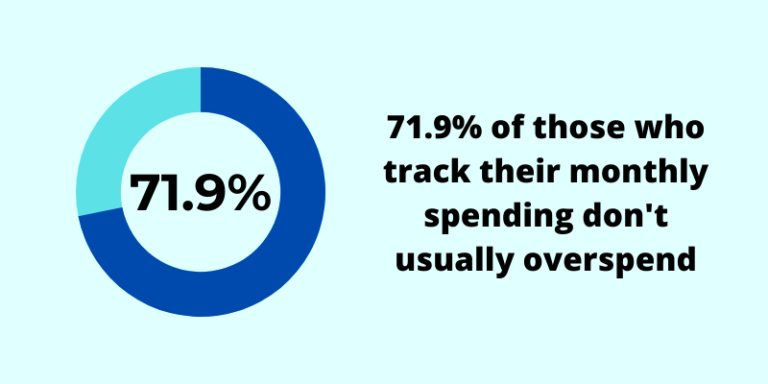

It is also important to track your monthly expenditure to check if you are keeping to the planned budget allocations and whether you are overspending in any way.

According to a survey we did, people who track their spending are less likely to overspend than those who don’t.

2) Be adequately insured

Insurance is all about income and wealth protection.

Being adequately insured protects you and your family against the financial risks of accidents, total and permanent disability (TPD), severe illnesses, and even death. Key insurance policies to note include your medical and healthcare insurance such as MediShield Life and Integrated Shield Plans, term insurance, and whole life insurance.

Getting insurance is classified as a short term goal because such incidents can occur suddenly and wipe away your entire savings, setting you back from your mid to long term financial goals or even making it difficult to survive.

Thus, being sufficiently insured is an important step to take for your personal finances.

3) Have an emergency fund

Not all huge ad hoc expenses or loss of income can be covered by your insurance policies.

According to Statista, about 26,000 were retrenched in 2020. In cases of unexpected economic downturns such as that caused by the pandemic, one can expect even higher rates of retrenchment.

Having a stash of money stowed away for such rainy days will provide a peace of mind and allow you and your family to continue living comfortably while you search for new job opportunities.

Financial experts recommend that you save at least 3-12 months’ worth of emergency funds. You may begin with saving 3 months, then progress to 6, and finally 12. The amount required should be calculated based on your monthly food, bills, utilities, and other necessary expenses.

Mid term goals

After achieving your short term goals, you can proceed to save up for your mid to long term expenses. These tend to be key milestones in your twenties and thirties, such as getting married, buying your first flat, and obtaining a car.

4) Be able to pay for wedding expenses

A wedding is a joyous occasion. It can also be an expensive affair. On average, a wedding in Singapore can cost about $30,000 to $50,000, and can go up to $100,000. The amount depends on the type of wedding you are planning.

For instance, the cost of ROM & solemnisation is only about $2,500 to $7,000. This is largely due to the cost of booking a venue and getting catering for a lunch reception.

The bulk of wedding expenses are incurred from hosting a wedding banquet, especially if it is at a 5-star hotel. Other miscellaneous costs include money for wedding bands, wedding photography, and your honeymoon. Discussing your ideal wedding with your partner and working towards this financial goal together can help ensure the both of you have enough savings to pay for your dream wedding.

QUICK CHECK

Can you answer these three questions?

1) How much would your family receive if something happened to you tomorrow?

2) What monthly income will your savings and investments actually produce at 65?

3) Who gets your assets, in what proportion, if you never get round to a will?

Most people can answer one at best. Not because they're careless, but because nobody's shown them the order to work through things.

That order exists. Here's the 7-step framework, from income and protection through to investments and estate planning.

5) Purchase your first property

One of the biggest milestones you will have in your life is purchasing your first property. For most Singaporeans, this would be a Build To Order (BTO) flat, which can cost about $250,000 to $500,000 on average. The actual price will depend on the number of rooms and location of the unit.

However, if you and your spouse’s total monthly income is above the income ceiling, you may have to purchase a resale flat or a private property instead. Both will typically come at a heftier cost.

Although you and your partner do not have to pay off the entire sum immediately, paying for housing should still be an important personal financial goal.

6) Buy a car

A survey done in 2016 showed that nearly two-thirds of young people aged 18 to 35 desire to own a car in Singapore. This is mostly for convenience and family transport needs. If you are one of them, you will need to make saving up for a car one of your personal financial goals, as these things don’t come cheap.

An average family-friendly car such as a Volkswagen Golf 1.4 costs about $110,479.80. This is largely due to the rising price of the Certificate of Entitlement (COE) in Singapore, which ranged from $48,510 to $60,109 for cars in June 2021.

Long term goals

Last but not least, your personal financial goals should include long term goals with a 10 to 40 years horizon. These are long term milestones that go beyond you and your family’s immediate needs. They typically require a huge amount of financial resources and are saved up or earned over many decades.

7) Providing a university education for your children

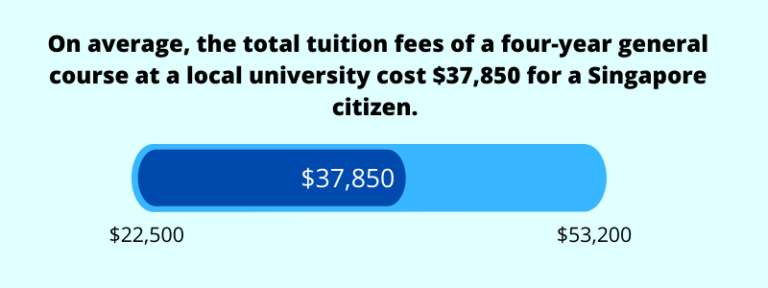

Ideally, every parent would want to provide for their children’s education to allow them to attain better qualifications without having to worry about student debt. However, university tuition fees aren’t cheap.

On average, the total tuition fees can amount to $37,850 for a Singapore citizen. This amount will definitely increase over time, especially when we take education inflation into account.

Thus, it is important to start saving as early as possible. You may even consider endowment plans that allow you to save up specifically for your children’s education in a relatively safe way while gaining higher returns.

8) Saving for retirement

While you plan for your children’s future, it is also important to balance your own needs and prepare for your retirement as well.

Saving up for retirement is one of the most vital long term personal financial goals as ageing and retirement are inevitable for all. Having the financial resources to lead a comfortable lifestyle and pay for medical expenses in your old age will be extremely important and entirely based on your savings or financial portfolio, unless you still have means of earning passive income.

So how can you plan for your retirement?

First, you will have to envision what your ideal retirement is, and when you hope to retire. You can then deduce the amount of funds required to achieve that, assuming your life expectancy will be at least 85 to 90 years.

Your personal financial goal should also take inflation into account. Based on this estimated figure, you can work with a financial advisor to discuss the best methods you can use to achieve this goal.

For instance, you may want to use a variety of instruments.

9) Leaving more for your next generation

Once you have accumulated enough wealth for you and your family, you may begin thinking about amassing these financial resources for your next generations. This can include taking care of your children or even your grandchildren financially after you have passed on. This is termed as estate or legacy planning.

Why is estate planning important? Statistics show that $132 million in CPF savings and more than 8,000 insurance policies are left unclaimed.

This demonstrates that it is necessary to do estate planning to ensure your assets go to the intended beneficiaries. Otherwise, it will be left entirely up to the law, which may result in delays, gaps or unfair distributions of your remaining assets.

Final Thoughts

Setting personal financial goals is one of the most beneficial things you can do for yourself and your family.

If you are married and have children, you will also find that many of these goals are not solely individual, but often require partnership and discussion with your spouse.

Having open communications with your spouse and financial advisor can ensure that you work together optimally to maximise the use of your resources for future life goals.

BEFORE YOU GO

Everything on this site is written for everyone. But your financial goals, your responsibilities, and what you already have in place are yours alone.

FullCircle is our comprehensive financial planning session. You'll walk away with a clearer picture of where you stand and what to prioritise, across protection, retirement, and estate planning.