Your colleague tops up his SRS account every December and swears by the tax savings. Your bank app keeps nudging you to open an account. So what exactly is this scheme, and is it worth locking your money away for?

In this guide, we cover everything important about the Supplementary Retirement Scheme (SRS) in 2026: how the tax relief works, how much you can contribute, and the withdrawal rules that decide how much tax you eventually pay.

If you’re a foreigner working in Singapore, the scheme works slightly differently for you, so read our guide to SRS for foreigners instead.

Key Takeaways

- The SRS is a voluntary savings scheme that helps you save for retirement while reducing your income tax. Every dollar you contribute (up to $15,300 a year for Singaporeans and PRs, or $35,700 for foreigners) reduces your taxable income for that year.

- You can withdraw penalty-free from the statutory retirement age that applied when you made your first contribution. For first contributions made from 1 July 2026, that age is 64. Only 50% of each withdrawal is taxable, and you can spread withdrawals over 10 years.

- The tax savings depend on your income. As of YA 2026, someone earning $100,000 a year saves about $1,760 in tax from a full $15,300 contribution, while someone earning $40,000 saves about $456.

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

What Is the SRS?

The Supplementary Retirement Scheme (SRS) is a voluntary, cash-funded savings scheme introduced by the Government in 2001 to encourage Singaporeans, PRs, and foreigners to save more for retirement, on top of CPF.

While your CPF savings provide for the basic needs of retirement, the SRS does what its name suggests. It supplements them.

And it has grown far beyond a niche scheme for the tax-savvy. There were 516,376 SRS account holders as at December 2025, more than double the number five years earlier, with total contributions of $23.88 billion based on MOF’s cumulative SRS statistics.

Why do so many people contribute?

Mostly the tax savings.

Who Can Open an SRS Account?

Anyone earning an income in Singapore can open an SRS account, whether you’re a Singapore Citizen, PR, or foreigner, as long as you are:

- At least 18 years old

- Not an undischarged bankrupt

- Not suffering from a mental disorder, and capable of managing your own affairs

Your employer can also contribute to your SRS account on your behalf. Employer contributions count towards your annual cap and are taxable as income, but you enjoy the corresponding tax relief.

How Much Can You Contribute to SRS?

You can contribute up to $15,300 a year if you’re a Singapore Citizen or PR, and up to $35,700 a year if you’re a foreigner, as of 2026. Contributions must be made in cash.

| Residency status | Maximum yearly contribution |

|---|---|

| Singapore Citizens and PRs | $15,300 |

| Foreigners | $35,700 |

To count towards a given year’s tax relief, your contribution must reach your SRS account by 31 December of that year (some operators set an earlier cut-off, so check with your bank).

One more thing to know before you contribute: SRS contributions cannot be refunded. Once the money is in, the only way out is a withdrawal, with the tax consequences we cover below.

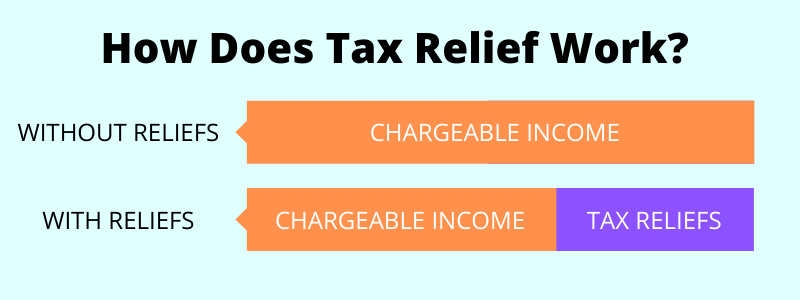

How Does the SRS Tax Relief Work?

Every dollar you contribute to SRS is deducted from your taxable income for that year. A lower taxable income means a smaller tax bill, based on Singapore’s progressive income tax rates.

Let me give you an illustration.

John earns $100,000 a year. If he contributes the full $15,300 to his SRS account, his taxable income drops to $84,700. Assuming he has no other reliefs, his income tax falls from $5,650 to about $3,890.50.

That’s roughly $1,760 saved in a single year, for money he was setting aside for retirement anyway.

Here’s how the savings look across income levels, assuming a full $15,300 contribution and no other reliefs (as of YA 2026):

| Annual income | Tax before SRS | Tax after SRS | Tax savings |

|---|---|---|---|

| $20,000 | $0 | $0 | $0 |

| $40,000 | $550 | $94 | $456 |

| $60,000 | $1,950 | $879 | $1,071 |

| $80,000 | $3,350 | $2,279 | $1,071 |

| $100,000 | $5,650 | $3,890.50 | $1,759.50 |

| $150,000 | $12,450 | $10,155 | $2,295 |

| $200,000 | $21,150 | $18,396 | $2,754 |

The higher your income, the more each SRS dollar saves you, because the contribution comes off your highest tax bracket. That is why around 90% of SRS contributors have an assessable income above $80,000, based on a 2019 parliamentary disclosure by the Minister for Finance.

At lower incomes, the savings are modest. If you earn $40,000, you save $456 but lock up $15,300 until retirement age. Whether that trade is worth it depends on what else you could do with the money. SRS is one of several ways to reduce your income tax, and not always the first one to reach for.

The $80,000 personal relief cap

Before you contribute, check one number: your total personal reliefs. There is a cap of $80,000 on total personal income tax reliefs per Year of Assessment, and SRS relief counts within it.

If your other reliefs already reach $80,000, an SRS contribution earns you no additional tax benefit, and remember, contributions can’t be refunded. Working mothers with several children are among the most likely to hit the cap, so do the sums first. IRAS itself advises evaluating whether you would benefit before contributing.

Your Withdrawal Age Is Locked In When You First Contribute

Most people only find this out years after opening an account, which is a shame, because it is easy to act on.

Your penalty-free withdrawal age is the statutory retirement age that was in force when you made your first SRS contribution. Once locked in, later increases to the retirement age don’t affect you.

That matters because the retirement age in Singapore keeps rising. It moved from 63 to 64 on 1 July 2026, and the Government has committed to raising it to 65 by 2030.

| Date of your first SRS contribution | Your penalty-free withdrawal age |

|---|---|

| Before 1 July 2022 | 62 |

| 1 July 2022 to 30 June 2026 | 63 |

| From 1 July 2026 | 64 |

So opening an account and contributing even $1 locks in the current retirement age before it climbs again. If you think you’ll use SRS at some point before 2030, there’s a real case for putting in a token sum now rather than waiting.

SRS Withdrawal Rules and Tax

Contributions give you tax relief today, but SRS is better described as tax deferment than tax reduction. You still pay tax when you take the money out. How much you pay depends on the rules below.

All the rules in this section are set out on the IRAS page on SRS withdrawal tax. You don’t need to declare withdrawals in your tax return, as your SRS operator reports them to IRAS, and each withdrawal is taxed in the Year of Assessment after the year you make it.

How are withdrawals taxed after the retirement age?

Once you reach your locked-in retirement age, only 50% of each withdrawal is taxable, and there is no penalty. This 50% concession is the scheme’s second big benefit, after the upfront relief.

That’s the whole design of the scheme. You get relief during your working years, when your tax bracket is high, and pay tax on half your withdrawals in retirement, when your income (and therefore your tax rate) is usually much lower.

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

How long do you have to withdraw?

You have 10 years from your first penalty-free withdrawal to empty your account. The clock starts on the date of that first withdrawal, not at your retirement age, so you can delay starting if you have other income and want to wait.

Whatever remains at the end of the 10 years is treated as withdrawn in one go, with 50% of the balance taxed that year. So it pays to plan your drawdown rather than leave a large sum to be deemed withdrawn at the deadline.

One exception: if your SRS funds are in a life annuity, the 10-year window doesn’t apply. You simply pay tax on 50% of each annuity payout for as long as the payouts continue. We explain how SRS annuity plans work, alongside the other options, in our investment options guide.

How much can you withdraw tax-free?

Up to $40,000 a year, if you have no other taxable income. Since only 50% of a withdrawal is taxable, a $40,000 withdrawal produces $20,000 of chargeable income, and the first $20,000 of chargeable income is taxed at 0% under current rates.

Spread over the full 10-year window, that’s up to $400,000 withdrawn completely tax-free.

Compare that with taking the same $400,000 as a lump sum in one year:

| Withdrawal approach | Taxable income | Tax payable |

|---|---|---|

| $400,000 lump sum in one year | $200,000 | $21,150 |

| $40,000 a year for 10 years | $20,000 a year | $0 |

Same money, over $21,000 difference in tax (as of YA 2026 rates, assuming no other income). Unless you need the cash urgently, spreading withdrawals is almost always the better move.

If you expect to have more than $400,000 in SRS by retirement, the same principle still helps. Spreading withdrawals keeps each year’s chargeable income in the lowest possible brackets.

What about your CPF LIFE payouts?

Your SRS withdrawals don’t sit on their own. Everything else you earn that year counts too.

CPF LIFE payouts are not taxable, so they don’t affect this calculation. But rental income or part-time work add to your chargeable income and can push your SRS withdrawals into taxable territory.

That opens up a planning angle. If you retire at 64 but your CPF LIFE payouts only start at 65 or later, the early years of retirement may be your lowest-income years. Drawing down your SRS then, and drawing more in the years you have little other income, keeps more of each withdrawal in the 0% and lower brackets. Timing like this is easier to get right when you map out your whole retirement income plan rather than looking at SRS on its own.

What happens if you withdraw early?

If you withdraw before your locked-in retirement age, 100% of the amount is taxable and a 5% penalty applies on top.

An early withdrawal doesn’t just cancel the tax benefit you got. It usually leaves you worse off than if you’d never contributed. So if you have a definite need for the money before your 60s, SRS is the wrong place for it. Keep your emergency fund and medium-term savings outside the scheme.

Are there exceptions to the penalty?

Yes. In certain circumstances you can withdraw early with no 5% penalty:

| Reason for withdrawal | Amount taxable | 5% penalty? |

|---|---|---|

| Medical grounds (incapacity to work, or partial withdrawal on terminal illness) | 50% | No |

| Full withdrawal due to terminal illness | 50%, after an exemption of up to $400,000 | No |

| Bankruptcy | 100% | No |

| Full lump-sum withdrawal by a foreigner (account held at least 10 years, not a SC/PR for the 10 years before withdrawal) | 50% | No |

What happens to your SRS money when you die?

Your SRS balance is deemed withdrawn on the date of death, with no penalty. To make sure your family isn’t unfairly taxed for you not completing the 10-year drawdown, an exemption of up to $400,000 applies, mirroring what you could have withdrawn tax-free over 10 years. Only 50% of any balance above the exemption is taxable.

One estate planning point matters here. You cannot nominate a beneficiary for SRS, unlike insurance policies or CPF. The money forms part of your estate and is distributed under your will, or under intestacy law if you die without a will.

Don’t Leave Your SRS Money Sitting in Cash

Money sitting in your SRS account earns just 0.05% a year at all three operators.

Yet SmartWealth’s analysis of MOF’s December 2025 data shows about $5 billion of SRS money is sitting in cash, roughly one dollar in five across the scheme.

At 0.05%, that money loses purchasing power every year, potentially for decades before your withdrawal window opens. Left long enough, the loss can cancel out the tax benefit you contributed for in the first place.

Contributing is only half the job. The other half is investing the balance. SRS funds can go into T-bills, shares, ETFs, unit trusts, annuities, and more, and you’re not restricted to what your bank promotes. We compare the best SRS investment options in a separate guide.

How to Open an SRS Account

Only three banks operate SRS accounts:

- DBS/POSB

- OCBC

- UOB

There’s no meaningful difference between them, as the scheme’s rules are identical everywhere, so pick whichever bank you already use. You can only hold one SRS account at a time, but you’re free to transfer between operators later.

Opening an account takes minutes on any of the three banks’ apps, and a $1 contribution is enough to lock in your withdrawal age.

Pros and Cons of SRS

| Pros | Cons |

|---|---|

| Contributions reduce your taxable income (within the $80,000 relief cap) | Early withdrawals are 100% taxable plus a 5% penalty |

| Only 50% of withdrawals taxable after retirement age, up to $400,000 potentially tax-free | Money is locked up until your early 60s in practice |

| Investment returns accumulate tax-free inside the account | Contributions are cash only and cannot be refunded |

| Wide range of investment options | Idle balances earn just 0.05% a year |

| First contribution locks in your withdrawal age before future rises | No beneficiary nomination, unlike CPF or insurance |

So, Is SRS Worth It?

For higher earners, usually yes. Once your marginal tax rate reaches 15% or more (roughly $120,000 of chargeable income and above), a full contribution saves over $2,000 a year, and the 50% withdrawal concession means much of that saving is never clawed back.

For more moderate incomes, it’s a judgement call. The savings are real but smaller, and the money is locked up for decades. In my opinion, SRS earns its place after your protection needs, emergency fund, and CPF considerations are settled, not before.

Whatever your income, two things are worth doing. Contribute early enough in life to lock in your withdrawal age, and don’t let the money sit in cash once it’s in.

SRS is one tool among several for your retirement, alongside CPF, insurance, and investments held in cash. How they fit together, and in what order, depends on your income, your age, and what you want retirement to look like. If you’d like a professional to map that out with you, our comprehensive financial planning session covers SRS in the context of your full financial picture.

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.