Have you received letters telling you about ElderShield and you have no idea what it’s all about?

Or perhaps someone told you about upgrading your ElderShield and you wanted to know whether it’s worth it?

Rest assured.

In this ultimate guide, we’ll cover everything you need to know about ElderShield and its upgrade/supplements.

Make sure to read till the end to be well-informed on what ElderShield is all about.

(Update: CareShield Life has replaced ElderShield on 1 Oct 2020.)

This page is related to the CareShield Life 2-Part Series:

- Part 0: ElderShield vs CareShield Life

- Part 1: What is CareShield Life?

- Part 2: CareShield Life Supplement

What Is ElderShield?

In 2002, the Ministry of Health (MOH) initiated a severe disability insurance scheme named ElderShield.

As a Singapore Citizen or a Permanent Resident (PR), you’ll be automatically enrolled once you reach the age of 40 years old.

Roughly 3 months before your 40th birthday, you’ll be sent a letter to inform you about it.

The MOH appointed 3 insurance companies to assist in the ElderShield scheme. They are Singlife with Aviva, Great Eastern (GE) and Income Insurance (formerly NTUC Income).

You’ll be randomly selected to be under any one of the three companies and have the option to change insurer once you receive the welcome package.

Do not mistake ElderShield with MediShield Life or the Integrated Shield Plan. They are entirely different health schemes, and the latter is to provide medical insurance coverage, enabling the insured to claim inpatient and outpatient medical bills.

Only the 3 companies mentioned above can assist in this ElderShield.

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

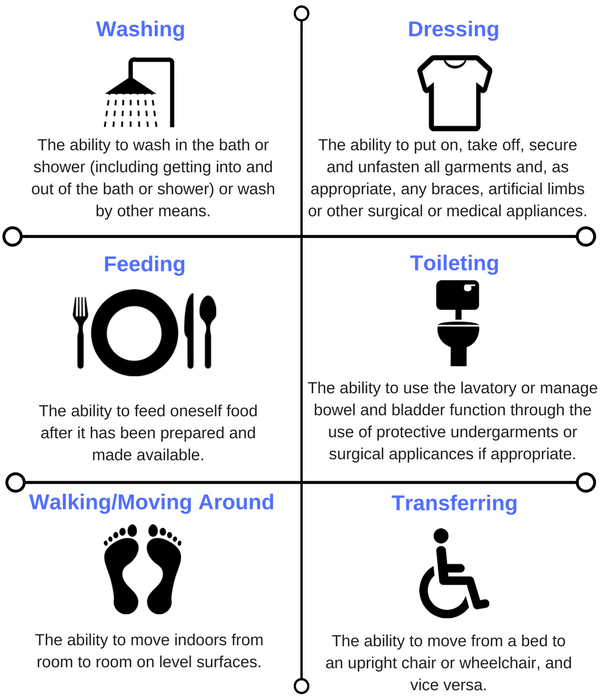

What Does ElderShield Cover?

There are 6 Basic Activities of Daily Living (ADLs). The below definitions are taken from the MOH website:

As long as you’re unable to perform at least 3 of these 6 ADLs (certified by an approved assessor) independently, with or without mobility aids, you’re eligible to receive a monthly payout from ElderShield.

How Much Will You Receive?

Well it depends.

Currently, there are ElderShield 300 and ElderShield 400.

If you turned 40 and subsequently joined after September 2007, you should be under ElderShield 400. If you had joined before this date, you should be under ElderShield 300.

Now, as ElderShield was introduced in 2002, there may be a chance that those who turned 40 years old before that date to not have any ElderShield at all.

To be sure, check your CPF online.

- Login at www.cpf.gov.sg

- Click ‘My Messages’ on the left-hand panel

- Scroll down to Healthcare

How Much Does ElderShield 400 Cost?

If you’re automatically enrolled at 40, you should be paying the amount of $174.96/year for males and $217.76/year for females. This premium is payable from the CPF Medisave till age 65, after which you enjoy a lifetime cover.

If you’ve opted out before or do not have an existing ElderShield and wish to enter back in, the premiums would be based on your entry age.

You can take a look at the premiums over here.

Your family members can also help you pay the premiums. Here are examples of those who can:

- Spouse

- Parents

- Children

- Grandchildren

How Are the Claims for ElderShield?

It has been awhile since ElderShield was introduced in 2002.

Throughout these years, are there many who claimed from it?

Let’s look at some statistics on ElderShield claims:

- Out of 1.3 million Singaporeans covered under ElderShield, only 15,600 policyholders had claimed

- ElderShield premiums amounting to $3.3 billion were collected

- Only $133 million were paid out in ElderShield claims

Looking at just the statistics, they may not look promising, however, they don’t tell the full story.

One point to note is pre-funding.

Basically, the probability of severe disability claims is much lower when you’re young compared to when you’re old.

So the premiums that you’d pay now are meant to be paid out when you’re older. And that’s why the premiums stop at age 65, but the coverage is for lifetime.

The concept for this is to “save for a rainy day”.

Is the Basic ElderShield Enough?

The purpose of ElderShield is to provide some financial assistance to deal with expenses incurred in the event of severe disability.

The monthly payout can be used to pay for long-term care like hiring a maid/caregiver or stay in a nursing home.

Imagine you’re severely disabled and not able to earn an income anymore, you’re likely to need someone to take care of you.

It could be one of your family members, but do you want to burden them? Most people don’t want to be a burden to their family and would prefer a paid caregiver.

And if Basic ElderShield pays out only $400 a month for just a short period of 6 years, do you think it’s enough?

Most people do not think so.

Why Basic ElderShield May Not Be Enough

According to a study done by Singlife with Aviva in 2011, an individual who is severely disabled would require an amount of $2,150/month to pay for a domestic helper, nursing homes and miscellaneous expenses incurred from being unable to take care of themselves.

Long-term care can be costly and if you want to find out more about how much the different long-term care cost, you can take a look here.

Furthermore, 37% of caregivers have been providing care for more than 10 years (basic ElderShield only pays out for 6 years).

Moreover, the average life expectancy in Singapore has been increasing over the years. From the latest data, the average life expectancy for males and females is 81.4 years and 85.4 years, respectively. This shows a growing need for lifetime care.

So What? I Already Have My Own Private Insurance

Most of us would have some form of private insurance that covers disability.

But take note that most insurance companies only provide coverage for total and permanent disability till 70 years old at most. After which, the coverage stops.

The good news is that ElderShield and its upgrade can provide lifetime coverage.

Introducing ElderShield Upgrades

With the ElderShield reform in 2007, you’re now able to enhance your benefits with ElderShield supplements.

Below are some benefits of having your ElderShield upgraded:

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

The 7 Benefits of Upgrading Your ElderShield Early

1. Higher Monthly Payouts

Instead of a monthly payout of $400 or $300, you can select a higher amount.

The monthly amount may differ from company to company but currently, Singlife with Aviva has the highest amount allowed at $5,000 a month.

With a higher monthly payout, you’re able to enjoy professional care facilities if the need arises.

2. Lifetime Payouts

Instead of a short 5 or 6 years payout period, you can enjoy payouts for a lifetime.

As severe disabilities may be permanent and occur for a longer period, the lifetime payout ensures much-needed care can continuously be given.

Therefore, you wouldn’t need to burden your family members.

3. Easier Claim Eligibility

The basic ElderShield pays out upon the inability to perform 3 out of 6 ADLs.

Some may want easier claim eligibility for when the undesired situation comes.

As such, supplements would come in handy as you can choose plans that pay out upon the failure to perform only 2 out of 6 ADLs.

4. Maximising Your CPF Medisave

To pay the premiums of the upgrades, you can use your CPF Medisave (subjected to a cap of $600/year). For those who want a higher monthly benefit, you may need to top up with cash.

At the very least, most people would stick to solely using their Medisave to pay for their premiums.

Furthermore, you’ll receive 4% interest on your CPF Medisave balance every year.

Example: If a person has $40,000 in the Medisave, an interest of $1,600 will be credited to the Medisave account every year. Even if that person had stopped working, the interest itself could cover the premiums.

As of now, there are some limitations in using your CPF Medisave.

Firstly, your Medisave balance doesn’t form part of your CPF retirement monies so you wouldn’t be able to withdraw it out.

Secondly, if you pass away, only then can your Medisave monies go to your beneficiaries.

Thirdly, you’re only allowed to use your Medisave for certain uses, such as paying for medical expenses (subject to limits), enhancing your MediShield Life or ElderShield.

So it may be a good idea to utilise the Medisave to enhance your ElderShield so that you can get better coverage.

5. Benefits Are Higher/Premiums Are Cheaper

Unlike the hospitalisation plans where premiums get higher as you go up the age band, the premiums of ElderShield enhancements are level.

If you enter at an earlier age, the premiums you pay would be cheaper at the same amount of monthly benefit.

On the flip side, if you intend to utilise the full $600/year cap on the Medisave, the monthly benefit amount would be higher if you upgrade now compared to later.

6. Pay As You Go

Similar to how hospitalisation plans work, you pay for coverage as you go.

As an ElderShield upgrade has no cash value, you may stop it without penalties (other than the premiums you’ve paid).

Therefore, if you find yourself in a fix 3-4 years later and unable to afford the premiums, you can choose to discontinue the upgrade. But take note, you also lose the coverage that comes with it.

7. Capitalise On Your Good Health

The condition fo your health is important to insurance companies.

Are you currently healthy or do you have any medical conditions?

Even conditions like High Blood Pressure (HPB) may or may not be accepted depending on its severity. Applicants with Diabetes are generally rejected.

Why wait for a chance for health to deteriorate and make it harder to apply for better coverage in the future?

How To Upgrade ElderShield

You can upgrade your ElderShield with any of the three companies:

- Singlife with Aviva

- Great Eastern

- Income Insurance (formerly NTUC Income)

No matter which company your basic ElderShield is from, you can choose any of the 3 companies for the upgrade.

Example: Even if your basic ElderShield is under Great Eastern, you can opt to apply for Singlife with Aviva’s ElderShield supplement.

Below are some of the various supplements available:

- Singlife with Aviva – Singlife ElderShield Standard and Singlife ElderShield Plus

- Great Eastern – ElderShield Comprehensive

- Income Insurance (formerly NTUC Income) – PrimeShield

Conclusion

We’ve covered quite a bit on ElderShield and its upgrades.

Hopefully, it has been useful to you.

In my opinion, if you have excess CPF Medisave, why not do an enhancement?

You can enjoy better benefits mentioned above without the need of paying cash but by using your Medisave.

Do note that all applications need to go through medical underwriting so even if you wish to upgrade, it is not guaranteed that the application will go through as your current health condition will be assessed.

Take the first step and compare the ElderShield upgrades of the 3 companies by clicking here.

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.