Most people don’t really have a financial plan. They have a stack of decisions made at different times and for different reasons: a policy taken up years ago, savings sitting in one place, an investment in another, a few things they always meant to sort out. Each one made sense on its own. Side by side, they don’t add up to a system.

Where do you start? And what should you focus on first?

I set out to condense the core areas that actually matter and organise them into a single order you can work through, one that’s simple to follow without skimming over the detail.

The result is what I call the wedding cake strategy: my own take on how to bring your finances into one system and improve them, starting today.

This topic is wide, so throughout the article I’ll link to related subtopics if you’d like to go deeper on any of them.

Note: this content should not be taken as formal financial advice.

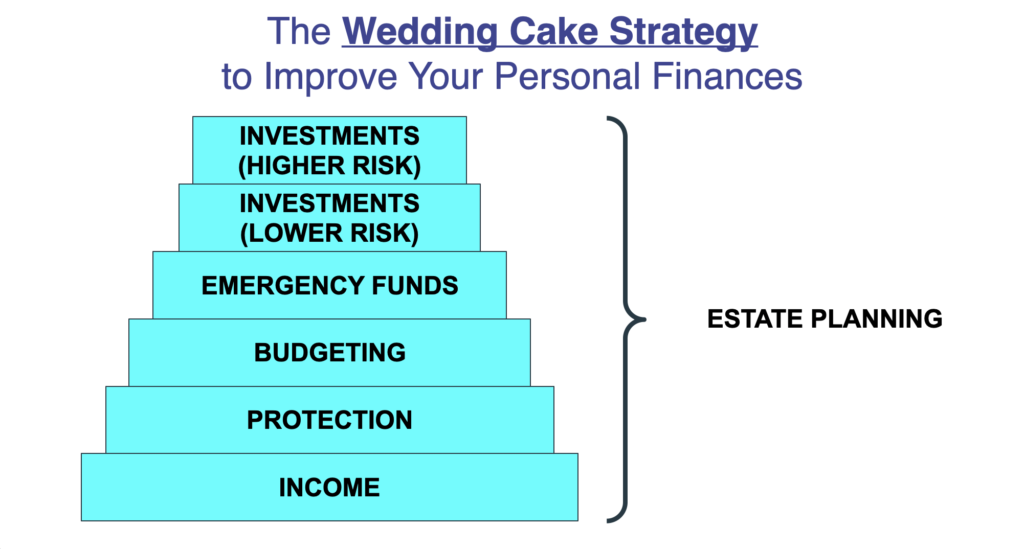

The Strategy in a Nutshell

To build a wedding cake, you start from the bottom layer and work your way up. The lower layers carry the most weight, so they have to come first.

Your finances work the same way.

It looks simple, and that’s deliberate. But there’s more to each layer than first meets the eye. In the sections that follow, I’ll go through every component in order, from your income at the base up through your investments, and explain the part each one plays in the whole.

Estate planning is the exception to the layers. It’s not a tier of its own, because it runs alongside everything rather than waiting until the end. Even early on, with few assets to your name, parts of it matter. A CPF nomination, or naming who would care for your children, counts regardless of how much you’ve built up.

The order matters as much as the items. Working through them in sequence is what turns a pile of decisions into a plan.

What Is Personal Financial Planning?

Before the steps, it’s worth being clear on what financial planning actually means.

Search for a definition and you’ll find plenty wrapped in jargon, some of them descriptions rather than definitions. The practical version comes down to two points. Point A is where you are financially today. Point B is where you want to be.

Financial planning is simply the process of building a plan that gets you from A to B.

So why bother? Because going without a plan quietly costs you, while a good one has a direct effect on the quality of life for you and your loved ones.

A good plan helps you:

- Keep up with the rising cost of living. Inflation slowly eats into idle cash, so your money needs to at least keep pace.

- Stay ready for emergencies. Illness, accidents, and retrenchment can strike without warning, and the right cover and savings cushion the hit.

- Reach your big milestones. A wedding, a home, your children’s education, and retirement all take real money and time to fund.

- Live better today. Planning lets you enjoy the present while still building towards the future.

The seven steps below are that process, laid out in order.

Don’t worry if you can’t act on all of them right now. Planning your finances is a marathon, not a sprint. Taking on too much at once is the surest way to give up entirely. The trick is to start, take small steps, and keep them going so it doesn’t get put off indefinitely.

1) Increase Your Income

Your income is the heart of everything. It pays for daily expenses, covers your financial responsibilities and commitments, and gives you something to save.

In my opinion, one of the best investments you can make is in your career or business, especially in the early stages of life. Businesses, big or small, want competent people who can help them increase revenue or reduce costs. By being genuinely good at what you do, through constant learning, upgrading your skills, gaining professional qualifications, and keeping pace with the tools reshaping your field, you make yourself harder to replace. In return, you tend to be rewarded with pay rises, promotions, and bonuses.

So if you focus on building your career, you’ll generally have fewer problems providing financially. It does take real effort and focus, though, which is part of why outsourcing the management of the rest of your finances can make sense.

Another route is a well-chosen side hustle. Done right, it can grow into a business of its own in time.

Two things tie directly into your earned income, and both deserve attention: CPF and taxes. They have a material impact on your finances, so it’s worth understanding how they work.

This is where higher earners leave the most on the table. Tax reliefs lower your taxable income, and the headroom is bigger than most people realise:

- SRS: up to $15,300 a year for citizens and PRs ($35,700 for foreigners), with the full amount qualifying for relief.

- CPF cash top-ups: up to $8,000 in relief for topping up your own account, plus another $8,000 for family, for $16,000 in total.

There’s a ceiling, though. All your personal reliefs combined are capped at $80,000 per Year of Assessment, so beyond a point, more won’t lower your bill. The aim isn’t to chase every relief going, but to use the room that fits your goals. These figures are current for 2026, so check IRAS and CPF for the latest.

2) Protect Your Income

If your income is everything, it makes sense to protect its continuity.

Three events can cripple your ability to earn:

- Death

- Total and permanent disability (TPD)

- Critical illness (CI) or early critical illness (ECI)

Statistically, these become more likely in the later stages of life. But that’s not the whole picture. The same data shows they can strike at any age, and when they do, the financial fallout for you or your family can be severe.

So you protect your income and your wealth through insurance.

I’ve helped submit a few death claims over the years, and my heart sinks every time, especially when I knew the person and their family well. Nobody wants to claim on insurance. But I can tell you with certainty that you would never want your loved ones carrying a financial burden if you were taken out of the picture.

In practice, that means holding the right types of insurance with an adequate level of coverage.

The risks from the three events above are reduced with life insurance, usually a term insurance plan or a whole life insurance plan, since the lump-sum payout replaces lost income.

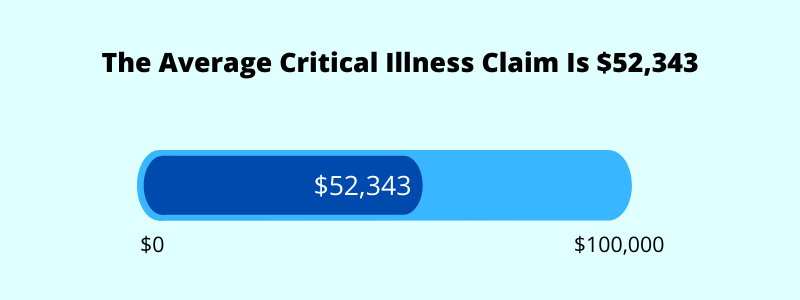

Critical illness deserves singling out. A serious diagnosis such as cancer, a heart attack, or a stroke can halt your income for months or years even when it isn’t fatal. Cancer alone is something an estimated 1 in 4 Singaporeans will face by the age of 75.

A critical illness plan pays a lump sum on diagnosis, and early critical illness (ECI) plans pay out sooner, at the earlier stages when costs and income disruption often begin. The trap is being underinsured: our research puts the average CI claim payout at around $52,000, which can fall well short of replacing several years of lost income.

There’s also disability income insurance, which replaces part of your monthly income if illness or injury stops you working, filling a gap that lump-sum plans might not fully cover.

Alongside life cover, medical or hospitalisation insurance is essential, well into old age. The hospital is the first place you’ll turn when illness or injury strikes, and with the cost of healthcare rising, a large bill can force you to dig into savings, sell assets you’d rather keep, or take on debt.

Proper coverage takes most of that risk off the table. For Singapore citizens and PRs, MediShield Life paired with an Integrated Shield Plan (IP) remains the core of medical protection. Expats and foreigners on an Employment Pass or similar aren’t covered by MediShield Life, so they rely on employer or private medical insurance instead.

Long-term care is worth a mention too: CareShield Life provides payouts for severe disability, and you can boost the cover with an insurer’s supplement.

Those are the common options to consider.

If you’re healthy now, have no dependants, or have no family medical history and don’t feel you need insurance yet, remember that even a minor ailment can affect your insurability later. Insurance is paradoxical that way: when you need it most is often when you can no longer get it.

Whatever you choose, make sure the premium is one you can comfortably afford and is reasonable for the coverage you get.

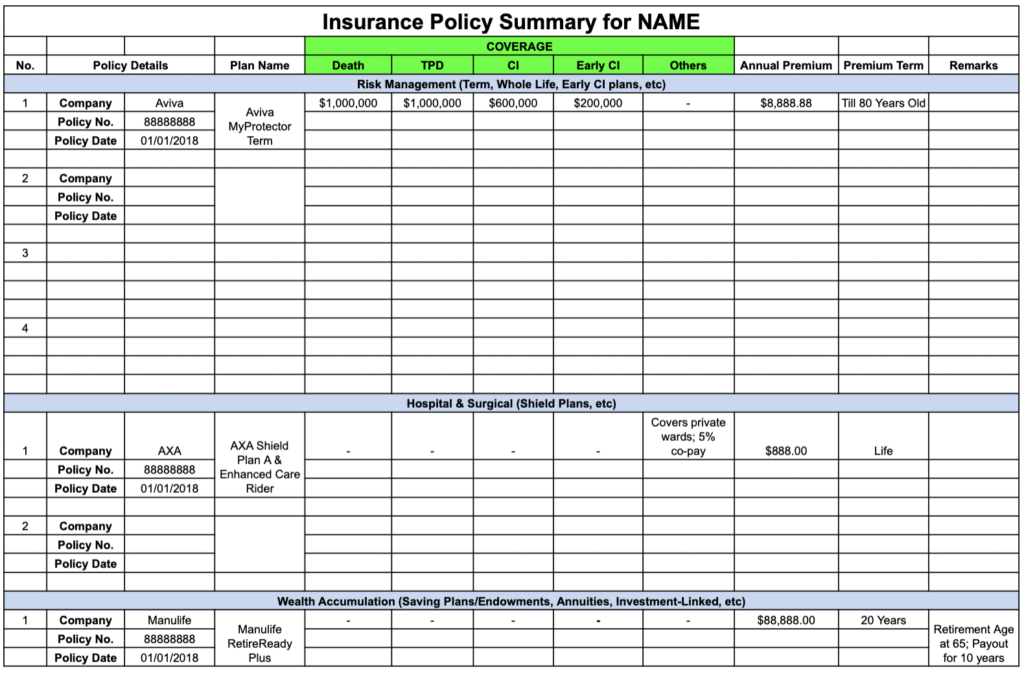

To close this section: many people I speak with don’t actually know what they’ve bought, how much they’re covered for, or which plan types they hold. If that’s you, do yourself and your family a favour and consolidate everything into a simple insurance policy summary.

Here’s a free template you can use. Make a copy or download it as an Excel file.

If you’d like to know whether your current coverage is actually enough, a licensed consultant can review what you hold and compare plans across different insurers to find the right fit.

3) Budget and Track Your Spending

A budget isn’t about restraint. It’s about knowing your savings rate, the gap between what you earn and what you keep, because that surplus is the fuel for everything from Step 4 onwards.

This matters more as you earn more, not less. The classic trap for higher earners is lifestyle creep: income rises, spending quietly rises to match, and the savings rate never moves. A bigger salary achieves little if none of it reaches your investments.

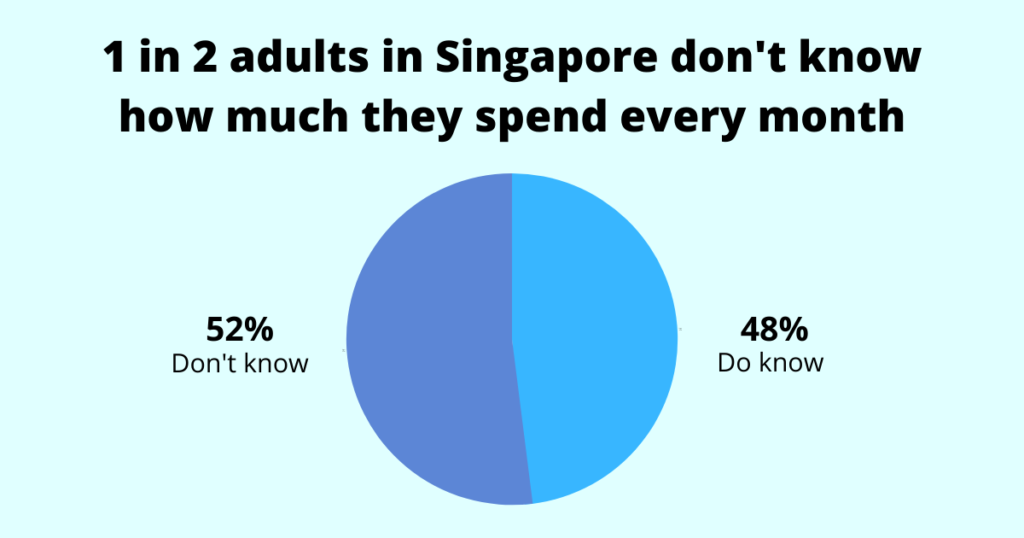

Even so, in a survey we conducted, 52% of adults in Singapore had no idea how much they spend each month.

The fix is simple. Budgeting just means deciding in advance what share of your income goes to needs, wants, and savings (the 50/30/20 rule is a fine starting point), then automating it. The moment your salary lands, a standing instruction moves your savings into a separate account before you can touch it. You save first and live on the rest.

You don’t need to track every coffee. Reviewing your statements once a month, with a simple template if it helps, is enough to see where the money goes and adjust.

4) Build Your Emergency Fund

With the first three steps in place, you should have more set aside. Where should it go?

The first priority is an emergency fund of six to 12 months of expenses. The more specialised your role or the more your household leans on a single income, the closer to 12 months I’d lean, as a senior position can take many months to replace.

It’s there for the things you can’t plan for:

- Retrenchment

- Major repairs

- Sudden hospitalisation or surgery

- The death of a loved one

When one of these hits, you need cash immediately. Without it, you’re forced to borrow or to sell investments at what could be the worst possible time.

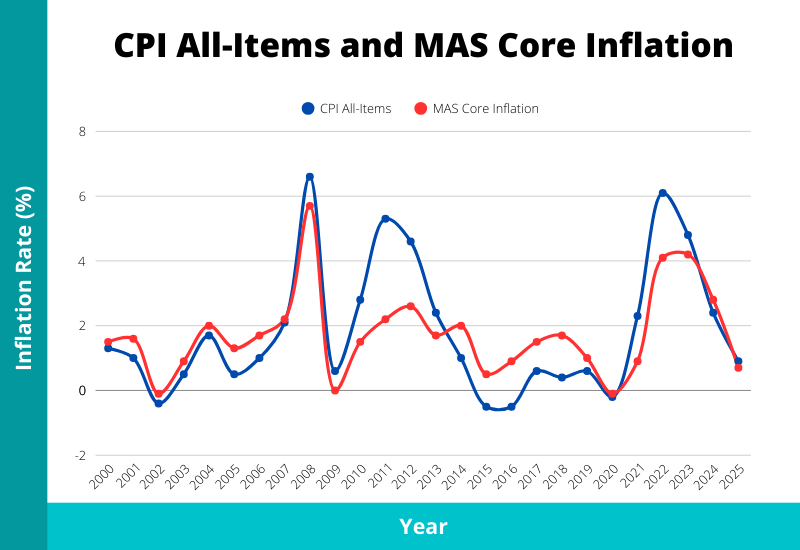

That said, an oversized cash pile has its own cost. Money parked in low-interest accounts loses value to inflation, and headline inflation has averaged 2.14% a year over the past 20 years (2005 to 2025). A regular savings account paying around 0.05% doesn’t come close to keeping up.

So hold enough to feel secure. Depending on how quickly you want to reach it, the usual options are:

- Regular or high-yield savings accounts

- Fixed deposits

- Singapore Savings Bonds (SSBs)

- Treasury bills (T-bills)

- Cash management accounts (which can still dip in value)

You don’t have to pick one. A mix often works well, and the higher-yielding options can offset some of the inflation drag without locking your money away.

One more thing before you invest: clearing any high-interest debt, such as credit card balances or personal loans. At around 25% a year, that debt grows faster than most investments can, so paying it off is effectively a guaranteed return.

Beyond what you set aside for emergencies, the rest should be put to work.

5) Invest Your Surplus

With the base in place, you’ve covered the major catastrophes and the unexpected. If you’ve built your career and kept your spending in check, you should have surplus cash left over. The question is what to do with it.

For most people, the answer is to invest it. Two reasons: to stay ahead of inflation, and to let your money grow faster than it would sitting in a savings account, so you reach your goals sooner.

Singapore’s tax system works in your favour here. There’s no capital gains tax, and dividends are generally received tax-free, so more of what your investments earn stays in your pocket.

The organising idea is simpler than the endless list of products suggests: match the investment to when you’ll need the money.

Money you’ll need soon, or can’t afford to lose, belongs in stable, low-risk holdings. Money for goals that are years or decades away, such as retirement or your children’s university education, can take on more risk for higher potential growth, because it has time to ride out the ups and downs. This is why you never invest your emergency fund: the one time you’d need it could be the one time the market is down.

There’s a second idea most people overlook. Investing has two phases. The first, accumulation, is the one everyone knows: building your pot while you’re earning. The second, decumulation, is turning that pot into a reliable income once you stop working. For Singaporeans and PRs, CPF LIFE provides a monthly income for life from age 65, though most people will need to supplement it. Far more attention goes into growing the money than into drawing it down safely, yet a poorly planned retirement income can run dry too early. If retirement is on your horizon, it’s worth planning for both.

As for the instruments themselves, there are countless ways to invest. Some of the more common ones, on top of the cash options from Step 4, include:

- Property

- Real Estate Investment Trusts (REITs)

- Retirement annuities

- Individual stocks and shares

- Bonds (corporate and government)

- Investment funds such as ETFs and unit trusts

- Cryptocurrencies (high risk, a small allocation at most)

In my opinion, a spread across several of these works better than betting on one, simply because diversification cushions you when any single holding falls.

Which mix is right comes down to you:

- How hands-on you want to be

- What the money is for

- How much risk you can stomach

- Your age and how long until you need it

If you’d rather focus on your career and take a hands-off approach, or you simply don’t know where to start, a financial planning session can map out suitable options for your situation.

6) Plan Your Estate

Death is the one certainty in life. The only question is when. Yet most of us avoid thinking about it, and if it comes unexpectedly, that silence leaves the people we love to pick up the pieces.

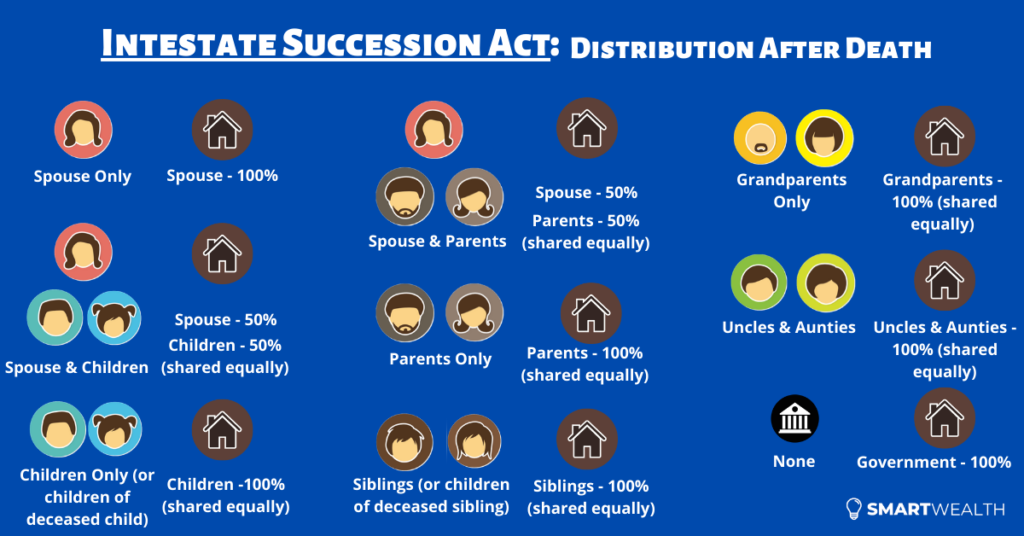

Do you actually know what would happen to your assets? If you’ve done nothing, they’re distributed according to the Intestate Succession Act, or Muslim law for Muslims, and not necessarily as you’d have chosen.

Beyond who receives what, your family also has to find it all. As paper statements disappear and more of life moves online, from bank logins to digital wallets and crypto, it’s easy for assets to go undiscovered simply because nobody knew they existed.

A few core tools put you back in control:

- A CPF nomination. This matters more than most people realise: your CPF savings are not covered by your will. Without a nomination, they’re paid out through the Public Trustee under intestacy rules, which takes time and may not reflect your wishes.

- A nomination on your insurance policies, so the payout goes to the people you intend without delay.

- A will, which sets out clearly who gets what. A straightforward will costs from a few hundred dollars and saves your family considerable time and hassle.

For higher earners and more complex estates, it’s worth going further. If you have young children, dependants with special needs, property here and overseas, or a business, a will alone may not give you the control you want over how and when assets pass on. A trust can hold assets and release them on your terms, and a business needs its own succession arrangements. One piece of good news: Singapore abolished estate duty in 2008, so there’s no inheritance tax to plan around, which keeps the focus on control and a smooth handover rather than tax.

If you haven’t written a will yet, at the very least list your assets and liabilities in one place, with the details, using a free template you can share with someone you trust. If anything happens, they’ll know what exists and who to approach.

All of the above applies on death. But what if you’re still alive yet mentally incapacitated and unable to decide for yourself? That’s the role of advance planning for incapacity, and like estate planning, it has to be set up beforehand. Three tools cover it:

- Advance care planning (ACP), to document your future care wishes

- A lasting power of attorney (LPA), to appoint someone you trust to make decisions for you if you lose mental capacity

- An advance medical directive (AMD), to state in advance that you don’t want extraordinary life-sustaining treatment if you’re terminally ill

Together, they make sure your wishes on healthcare, personal welfare, and your assets are documented or handled by someone you trust.

These two areas, estate and advance care planning, are the most overlooked of all, yet they make the biggest difference to the people you leave behind.

Estate planning is the step most people leave half-done: a CPF nomination made but no will, or a will that’s long out of date. It’s also the one area where mistakes only surface when you’re no longer around to put them right. If you’re unsure whether what you’ve set up actually holds together, a licensed consultant can help you see what’s missing and what to prioritise, and point you in the right direction to get it sorted.

7) Review Everything Regularly

Finally, a plan is never finished. Your circumstances, responsibilities, and goals shift over time, and what worked a few years ago may not fit today.

Set a regular interval, once a year is a sensible default, to look over the whole picture and check it still holds together: whether your coverage still matches your commitments, whether your savings rate and investments are on track, and whether anything in your estate plans needs updating after a marriage, a child, a new property, or a change in income.

This is also the step that keeps the other six working as one system, rather than drifting apart into separate decisions again.

Do You Need Help in Financial Planning?

If you’ve read this far, I hope the framework has given you a clearer sense of the order to work through things, from income and protection at the base, up through your investments, with estate planning running alongside it all.

The point was never the individual products. It’s that these seven steps connect. Worked through in sequence, they turn a pile of separate decisions into a single plan that holds together.

If you don’t yet have that plan, aren’t sure where to start, or simply want a second pair of eyes, consider going through a FullCircle comprehensive financial planning session. You’ll get guidance specific to your situation and goals, which look different for everyone.