Singapore has constantly been ranked as one of the cities with a high cost of living.

While some people may wonder if such statistics on Singapore’s high cost of living is valid, especially since $4 meals still exist in the hawker centres, it is an undeniable fact that other necessities of living are much higher than in other developed countries.

One of the main factors for the rising cost of living in Singapore can be attributed to Singapore’s lack of land and natural resources. This has led to Singapore’s dependency on other countries for supplying natural resources (food, oil, water, etc.) and on foreign labour workers to build our skyscrapers to accommodate a growing population on our tiny island.

Here are 9 statistics on Singapore’s rising cost of living that would affect Singapore residents’ financial decisions in the present day and future.

(Although we can’t control the cost of living, we can take charge by focusing on better ways to manage our finances.)

All prices quoted are in Singapore dollars (SGD).

- 1) Singapore is consistently named one of the world's most expensive cities

- 2) An estimated monthly cost of living in Singapore is $2,560

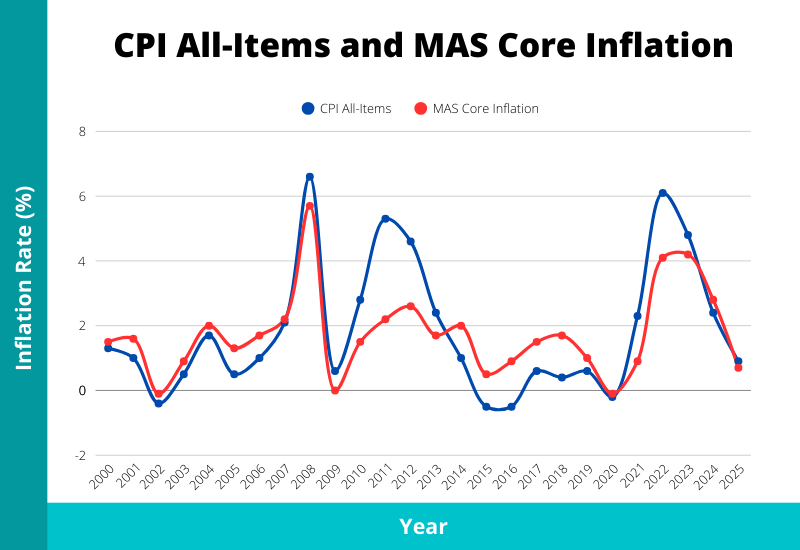

- 3) The average headline and core inflation rate over the past 20 years was 2.14% and 1.88% respectively

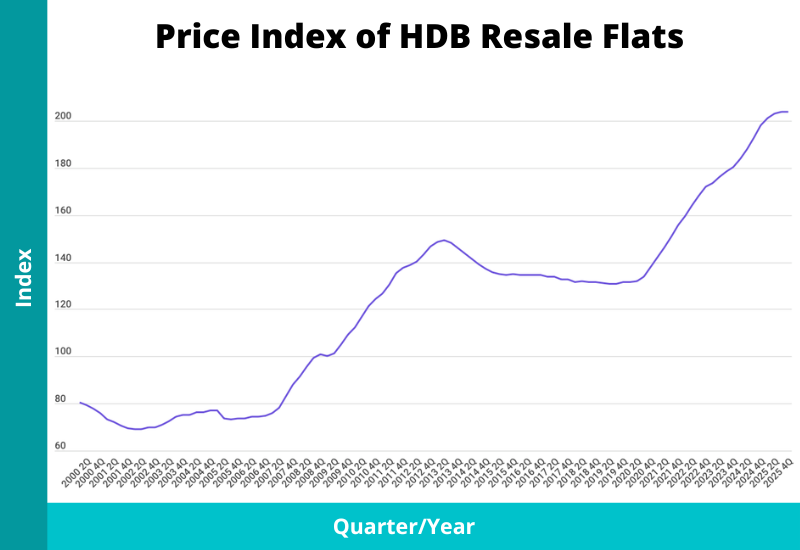

- 4) Prices of HDB resale flats have increased by 168.6% since 2000

- 5) Singapore is the most expensive place in the world to buy and own a private car

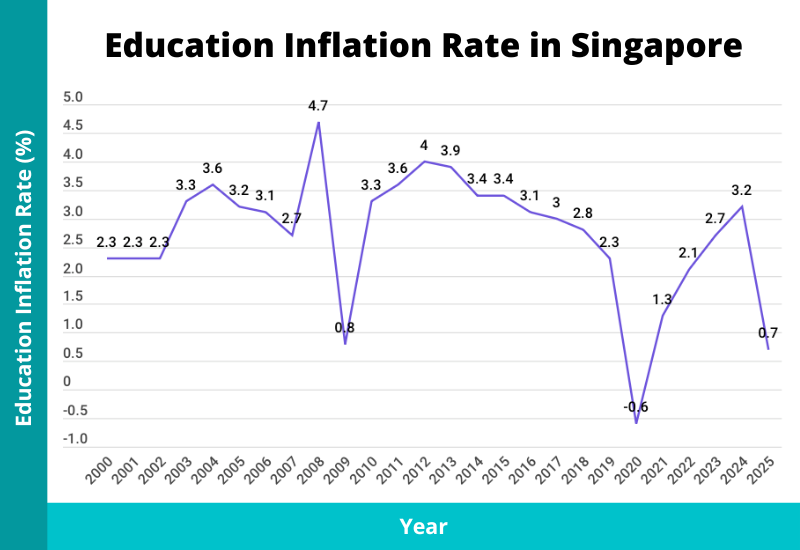

- 6) The cost of education has increased by 69.6% from 2005 to 2025

- 7) The healthcare inflation rate in 2025 was 2.7%

- 8) Food prices are heavily influenced by external factors

- 9) The median gross monthly income has grown by 46.2% over the past 10 years (2015 to 2025)

- What Can You Do About the High Cost of Living?

1) Singapore is consistently named one of the world’s most expensive cities

The Economist runs a biannual Worldwide Cost-Of-Living analysis every year.

The results are derived from a comparison between cities or countries in terms of the price of 138 products and services worldwide. In the survey, the Economist Intelligence Unit (EIU) examined common consumer goods such as clothing and electronics across 130 countries.

From 2014-2019, Singapore was ranked the world’s most expensive city to live in. Even in the midst of the COVID pandemic in 2020, Singapore was still listed in the top five most expensive cities. In 2021, Singapore climbed up to second place. In 2022 and 2023, Singapore regained its spot as the world’s most expensive city.

Here are some of the reasons for the seemingly high cost of living in Singapore.

However, it is important to note that the survey is geared to reflect the cost of living of expatriates/foreigners and not of Singaporean households. It doesn’t take into account subsidies and grants given by the government to Singapore Citizens and Permanent Residents, especially those from lower-income families.

SIDE NOTE

Most people's finances aren't a plan. They're a collection of separate decisions: a policy bought years ago, investments that don't talk to each other, a will that's still on the to-do list.

If that sounds familiar, there's a fix that doesn't require becoming a finance expert.

Here's the 7-step framework we use to organise everything into one system.

2) An estimated monthly cost of living in Singapore is $2,560

An individual’s monthly cost of living is determined by one’s lifestyle and commitments, and whether you’re a Singaporean or not.

In the table below, we considered areas that are necessities and wants and have tabulated rough estimates of the monthly cost of living in Singapore.

| Low-Range | Mid-Range | High-Range | |

| Single Adult (with rent) | $1,245 | $2,560 | $7,780 |

| Single Adult (without rent/mortgage loans) | $545 | $1,360 | $4,380 |

| Couple | $2,740 | $5,770 | $16,560 |

| Family of 4 | $3,200 | $7,920 | $22,060 |

If you are married and have children, the numbers are likely to be much higher. This is due to the inclusion of other essentials such as insurance payments, setting money aside for childcare, or hiring a domestic helper.

(We have not accounted for the full range of expenses, such as a monthly allowance to parents. And tabulated costs may include overlaps, so do not take them seriously.)

3) The average headline and core inflation rate over the past 20 years was 2.14% and 1.88% respectively

The inflation rate is measured by the change in the Consumer Price Index (CPI), which includes the essential prices of things like housing, clothing, food, healthcare, etc.

To put it simply, headline inflation measures the average change in prices of all goods and services, while the core inflation factors in all goods and services excluding the components of “Accommodation” and “Private Transport”. Thus, core inflation is a better indicator of the change in prices of everyday items.

We’ve done an analysis of inflation in Singapore and here is what we’ve found.

| Average Headline Inflation Rate (CPI All-Items) | Average Core Inflation Rate (MAS Core Inflation) | |

|---|---|---|

| Over the last 10 years (2015 to 2025) | 1.72% | 1.76% |

| Over the last 20 years (2005 to 2025) | 2.14% | 1.88% |

| Over the last 30 years (1995 to 2025) | 1.68% | 1.63% |

The average inflation rate is much higher than the interest rate that an average bank savings account gives to Singaporeans; money left in the bank will devalue over time.

The annual inflation rate (both the average headline and core inflation rate) has almost always been positive, and only a few years have seen very low inflation rates.

The highest core inflation rate was 5.7% in 2008. Although there was a financial recession in 2008, higher oil prices pushed inflation upwards. The lowest annual core inflation rate was -0.2% in 2020 due to the COVID pandemic.

Inflation is affected by both internal and external forces. As Singapore has to largely depend on other countries for natural resources, prices of certain goods and services were acutely affected.

4) Prices of HDB resale flats have increased by 168.6% since 2000

It is a well-known fact that property prices are extremely high in Singapore compared to other developed countries (with the exception of Hong Kong).

Property prices are almost always on an upward trend. Here are the private residential property and HDB resale price indexes from 2000 to 2025:

From 2000 to 2025, private residential property prices have increased by 128.0%, while prices of HDB resale flats have increased by 168.6%.

Due to more work-from-home (WFH) arrangements and investments from foreigners, property prices have surged since 2020. There were also 1,594 million-dollar HDB flats transacted in 2025, the highest in any given year.

The table below tabulates the average and median prices for HDB resale flats, private condominiums, and landed properties.

| Housing Type | Average Price | Median Price | Average Price/Sq. Foot | Average Size (Sq. Foot) | Average Price/Sq. Metre | Average Size (Sq. Metre) |

|---|---|---|---|---|---|---|

| HDB Flats | $652,498 | $628,000 | $638.80 | 1,021.38 | $6,876 | 94.89 |

| Condo | $2,128,942 | $1,875,000 | $2,123.95 | 1,002.22 | $22,862 | 93.11 |

| Landed | $5,928,412 | $4,650,000 | $1,815.79 | 3,264.93 | $19,545 | 303.32 |

5) Singapore is the most expensive place in the world to buy and own a private car

The Business Insider reported that Singapore is the most expensive place in the world to buy and own a car.

Car ownership is purposefully designed to be unaffordable for the majority, as the government tries to reduce to use of cars as these will cause congestion and the need for more land space to park them. The government primarily controls the prices of automobiles through the Certificate Of Entitlement (COE). In Apr 2026, the COE was at $118,000 for Category A cars.

A new Toyota Corolla Altis now costs $195,888. This has not accounted for other costs of running a car such as petrol, parking, insurance, payment of road tax, and car maintenance.

| Cost of Running A Car | Monthly Average |

| Petrol | $320 ($80 for 38 litres of petrol) |

| Parking (seasonal HDB pass + public car parks) | $130 |

| Car Insurance | $85-$125 |

| Road Tax | $85-$90 |

| Car Maintenance (oil change every 8000-10,000km (approximately once every 3 months)) | $50-$100 |

| Total | >$675 |

QUICK CHECK

Can you answer these three questions?

1) How much would your family receive if something happened to you tomorrow?

2) What monthly income will your savings and investments actually produce at 65?

3) Who gets your assets, in what proportion, if you never get round to a will?

Most people can answer one at best. Not because they're careless, but because nobody's shown them the order to work through things.

That order exists. Here's the 7-step framework, from income and protection through to investments and estate planning.

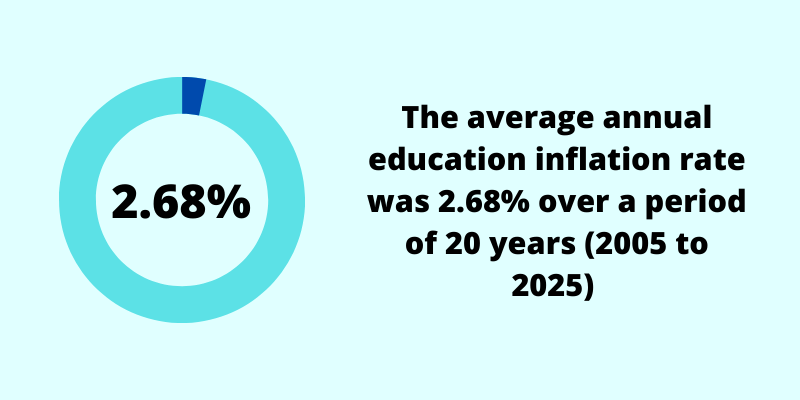

6) The cost of education has increased by 69.6% from 2005 to 2025

The cost of education has risen by 69.6% over the past 20 years. Benchmarked against the CPI-All Items inflation (52.8% over 20 years), the number is considerable.

The dramatic increase can be attributed to the rising demand from the younger generations to get a degree. This is fuelled by the knowledge-driven economy which rewards those with a paper degree in both opportunities and monetary terms.

The graph above charts the inflation rate for education in Singapore. Every year there was an increase, except for 2020, because local universities decided not to raise tuition fees. The average education inflation rate over the past 20 years was 2.68%.

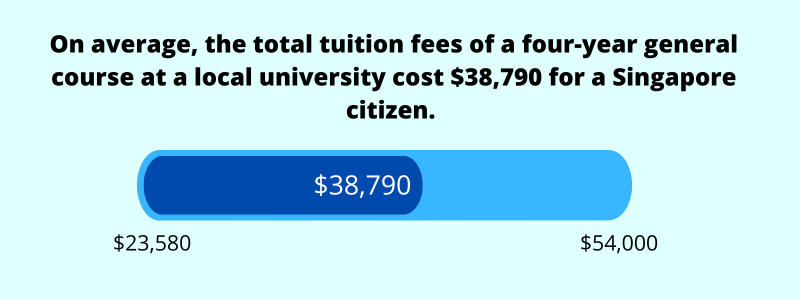

In 2026, the estimated tuition fees for a four-year general course at a local (public) university in Singapore are $38,790.

This does not include the living expenses of a student, which can amount to $43,100 for four years. In total, the cost of obtaining a degree is close to $80,000, in today’s value.

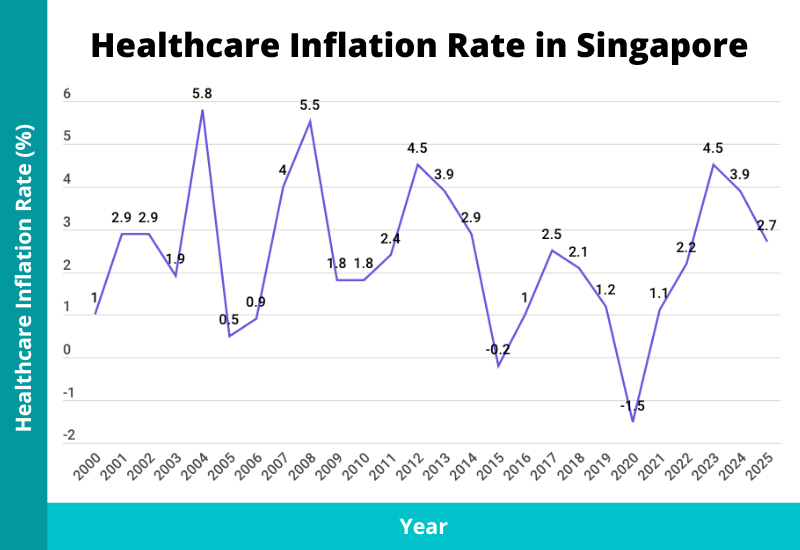

7) The healthcare inflation rate in 2025 was 2.7%

Another contributing factor to the high cost of living in Singapore is the cost of healthcare, which has been of interest lately.

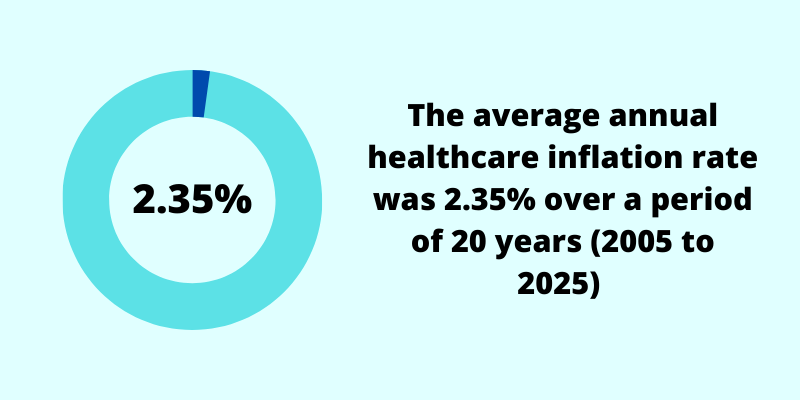

The cost of healthcare has increased by 59.1% from 2005 to 2025, and the average was 2.35% per year.

The reasons for rising healthcare costs are as follows:

- Life expectancy has increased

With a longer life expectancy comes greater healthcare expenditure. It is undeniable that in old age, more healthcare costs are to be expected as the body slows down. - More people are using healthcare facilities

Singapore boasts one of the best healthcare systems in the world. A large part of this is not only because of our well-trained healthcare workforce but the investment in medical technology. This has allowed people to go for more health checkups, and often the early detection of any critical illness would be treated immediately. This also means that more money would be spent on healthcare services. - Increase in manpower and operating costs

As there is strict gatekeeping in Singapore for our doctors, manpower costs have also increased. Students are not only required to have straight A’s but must be ready to set aside at least $60,000-$100,000 for school fees. As such, salaries also need to be matched. Operating costs also went up. - Premiums for health insurance are increasing

Premiums for MediShield Life have gone up since 1 March 2021, due to more comprehensive coverage being provided and to address rising healthcare costs. Integrated Shield Plan premiums have also risen significantly. “Full” riders have since been phased out, with the industry moving towards higher co-payment plans.

8) Food prices are heavily influenced by external factors

Do you know that 90% of the food consumed in Singapore is imported?

Even water, an essential part of life, is imported from Malaysia.

Due to the lack of natural resources and land scarcity, it is almost impossible to grow our food. As such, Singapore is often at the mercy of other countries’ pricing of their goods.

Thankfully, our government has worked hard to control these prices by building good relationships with our neighbours. However, food supply disruptions and tensions can affect the cost of food (and its supply) anytime.

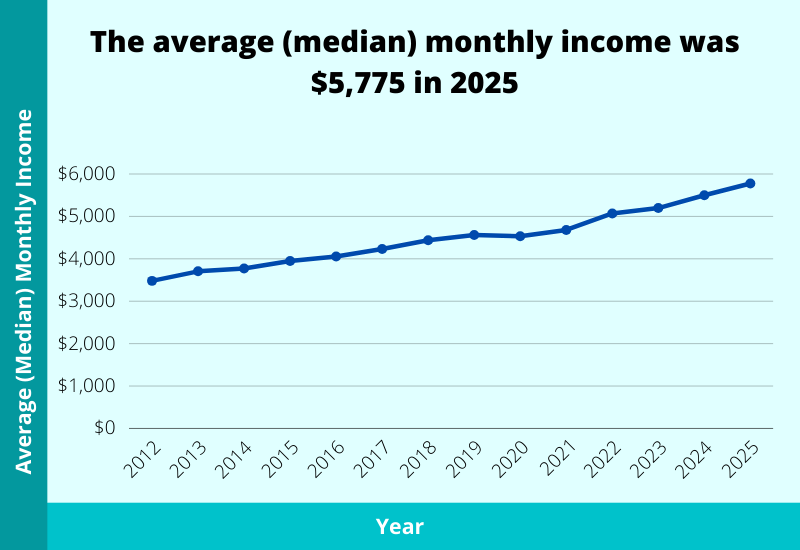

9) The median gross monthly income has grown by 46.2% over the past 10 years (2015 to 2025)

Fortunately, the median gross monthly income has also grown:

| Year | Median Monthly Income (Including Employer CPF Contributions) |

|---|---|

| 2015 | $3,949 |

| 2016 | $4,056 |

| 2017 | $4,232 |

| 2018 | $4,437 |

| 2019 | $4,563 |

| 2020 | $4,534 |

| 2021 | $4,680 |

| 2022 | $5,070 |

| 2023 | $5,197 |

| 2024 | $5,500 |

| 2025 | $5,775 |

In 2015, the median monthly income was $3,949, and it has risen by 46.2% to $5,775 in 2025.

The increase in gross monthly income is thankfully faster than the cost of living, thus outpacing inflation. The real annualised change of median gross monthly income from 2015 to 2025 is 2.1% (after factoring in inflation).

What Can You Do About the High Cost of Living?

While the facts and statistics listed above are things the average Singaporean cannot control, we can try our best to manage our finances and lifestyle choices.

Making use of various government schemes helps reduce our expenses, but we must still be conscientious in managing our overall expenses. For example, you may want to reconsider owning a new car, and weigh your options (either purchase a second-hand car or stick to public transportation and private hire cars).

Foreigners tend to experience a higher cost of living compared to locals as they do not get the same grants and subsidies. Expats who plan to relocate to Singapore should do a thorough analysis of whether they can afford to make the move and preserve their current lifestyle choices.

Whether you’re a local or a foreigner, one way to keep expenses low is to know how to budget effectively.

BEFORE YOU GO

Everything on this site is written for everyone. But your financial goals, your responsibilities, and what you already have in place are yours alone.

FullCircle is our comprehensive financial planning session. You'll walk away with a clearer picture of where you stand and what to prioritise, across protection, retirement, and estate planning.