Yes, you heard that right.

There’s a newborn baby in the financial world.

For some of you, it can be a game changer because this baby inherited the best DNAs from both parents – Papa Term and Mama Whole Life.

For all the money you’ve paid to insurance companies, it’s time to get it back (finally!).

I’ll touch on what this is but first, let me make a very quick detour…

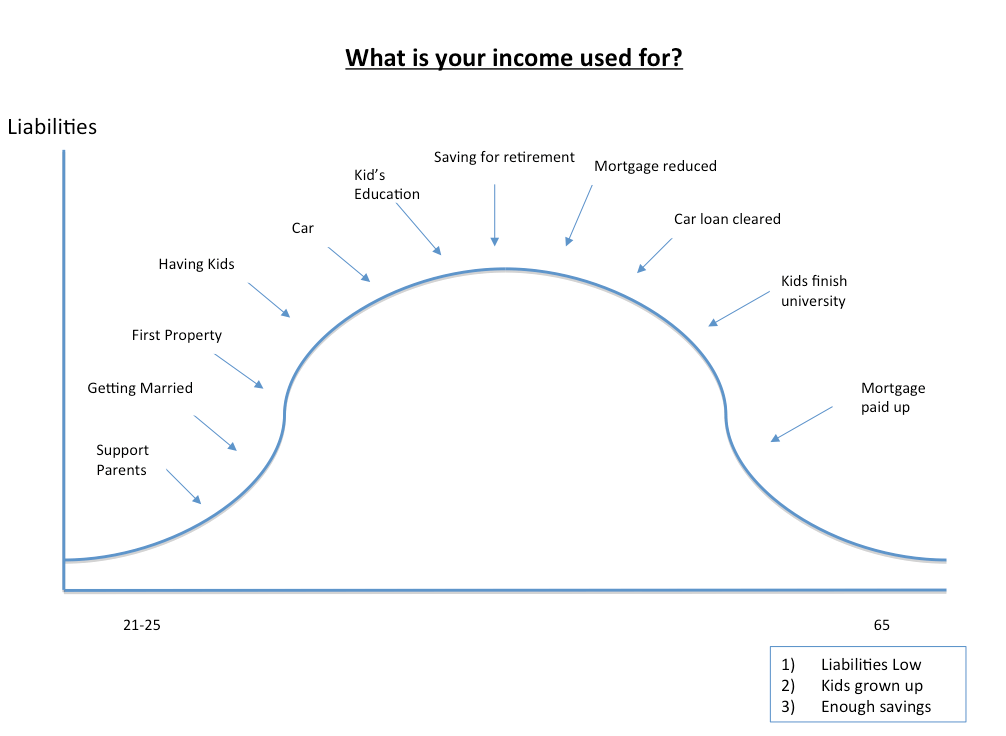

Main Purpose of a Term or Whole Life: Protecting Your Income

If you’re here, you already know what they are.

Chances are that you already have one of either, both, or for some reason, multiples of both.

Once upon a time, there was a rationale for you to get it… and it all boils to this:

Income Protection.

Here’s a quick refresher:

Your income is used to pay for everything.

Once you lose this income, everything comes at a standstill.

SIDE NOTE When was the last time you conducted thorough financial planning or reviewed your finances? In this day and age in Singapore, doing so will absolutely improve the quality of life for you and your loved ones. Here are 5 reasons why financial planning is so important.

There are 2 scenarios for you to lose this income:

1) You firing your employer, or your employer firing you

This is only temporary because you’ll likely find another job within 3-6 months in Singapore.

2) Death, Total & Permanent Disability or Critical Illness

With any of these 3 happening, your income will be permanently lost. That’s why it’s a BIGGER concern.

That was the reason you got a term or whole life to replace the loss of potential income with the insurance payouts.

(I’m not going to cover how much you need because it’s outside the scope of this article).

Let’s just quickly touch on the advantages and disadvantages of both…

The Slow Downfall of the Whole Life Plan

The best aspects of a whole life plan are that it gives you cash value and coverage for life.

This means that whether you surrender the policy at a certain age or you live till your last day, you can still get back something.

But because part of the premiums you pay goes into Coverage AND Savings…

This translates to:

- Higher Premiums

- Lower Coverage

Which is why the next alternative is more popular now.

Most People Turn To Term Insurance Now

With a term plan, the premiums you pay solely goes into coverage.

This translates to:

- High coverage

- Lower premiums

But… There are 2 Downsides with Term Plans

Like in Marvel, there’s always good and evil.

There are 2 “villains” in this case.

1) Term plans have no cash value

I’m sure this thought went through your mind before:

“I’ve spent so much on paying the premiums, but if nothing happens, I don’t get a single cent back”

2) Not sure when to cover till

The general rule of the thumb is to cover till your retirement age.

But some of you may be thinking:

“…but what if something happens to me just 1 year after I retire?”

Well, you still don’t get anything back as the plan would’ve already expired.

So now, you’re thinking whether you should cover till 65… 70… 75… 80…

There’s unrest in the world of “what ifs”.

And thus, a super-superhero is here to save the day (corniness intended).

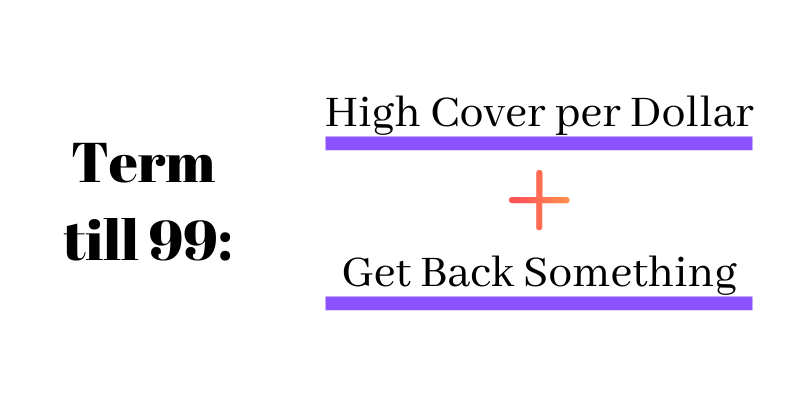

Introducing… the Term till 99

With the best DNAs from whole life and term, this baby is born.

As the name suggest, it’s a term plan that covers till age 99.

It’s like a term but at the same time, not like a term.

The plan usually only covers death (100% chance of happening) but you can still add in other coverage if you wish.

Let me explain why this baby is so unique.

DID YOU KNOW? According to a survey conducted by MoneySense, about 3 out of 10 Singapore residents aged 30 to 59 had not started planning for their future financial needs. This isn't surprising because personal finance can seem complicated and daunting. But really, there are only a few things that you should focus on. Learn how to significantly improve your personal finances with the 7-step "wedding cake" strategy today.

A Lifetime of Paying?

Now it used to be that most insurance companies have such plans that you’ll need to pay till 99 years old.

And people still get it because such plans are meant for your kids (eventually).

So if your kids want to have the payout, then they can help you “service” the premiums when you stop earning an income.

(Having said that, you need to first make sure you can afford the premiums without factoring in your kids).

But some want to see it as purely a gift – leaving a legacy behind – and don’t want their kids to “support” their death.

And that’s why there are limited pay options such as paying till 65 or 75 years old and you’ll still maintain coverage after.

(Note: the annual premium of a limited pay option is almost always higher than the pay till 99 years option)

But…

Living to a Ripe Old Age

The average lifespan in Singapore is 84.8 years.

So based on statistics, there’s a higher chance that you get a death payout before that age.

But if you’re lucky (or unlucky… I’m not sure these days) and you live beyond 99 years old, what happens then?

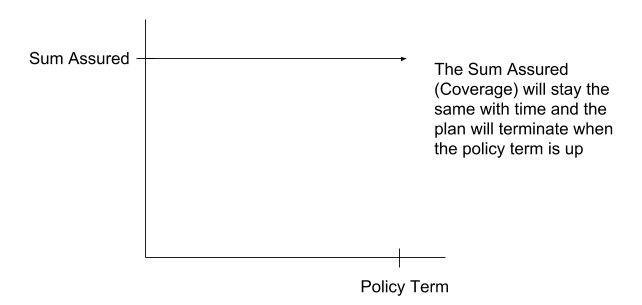

Traditional term plans expire when the policy term is up.

So if one were to live to a “three digit age”, there will be no payouts because the term plan would’ve expired prior to that.

Luckily there’s a new addition.

“Hedge” Against Living Beyond 99

So only recently, there’s a way to counter a term expiring without payouts.

Some insurance companies introduced a clause in their policy and it goes like this…

In short, once you hit 100 years old and the plan is in-force, you can receive 100% of the sum assured.

What this means that no matter rain or shine, you’ll still receive the sum assured.

Let me give you some numbers to illustrate…

Case Study: Jimmy

Jimmy just crossed his 35th birthday and doesn’t smoke.

Jimmy loves his family very much – his wife and 2 kids.

He decides to get a term till 99 plan (that has the “longevity payout”) which covers $1,000,000 for Death only, and chooses to pay premiums till 75 years old.

He needs to pay a premium of $6,192/year.

In the worst case scenario (if he lives beyond 75), the total premiums he’ll need to pay is only just $241,488.

But he’s covered for $1,000,000 throughout.

If he passes on earlier, say for example, 5 years later, he would’ve paid $30,960 in total.

But the payout is still $1,000,000.

(There may be ongoing promotions such as a 10% perpetual discount. Get quotes to find out more)

Too Good To Be True

Although it may seem like the insurance companies are giving you the opportunity to earn their money, this is not always the case.

There are 3 conditions for a term till 99 to make sense for you.

1) Age-sensitive

As with all insurance, the younger you apply, the lesser the premiums you pay.

This is not within your control because you can’t turn back time (even if you can, you probably wouldn’t think about insurance).

But it can still make sense at an even older age.

You’ll need to see how much premiums you need to pay and judge for yourself.

2) Must be healthy

If you have any medical conditions – small or not – then you might need to reconsider.

If you’re accepted as “standard life”, then you’re good to go.

However if you’re given a premium loading (% increase in the premiums), then this drastically reduces the chance for a term till 99 to make sense for you.

Simply because the overall premiums you need to pay is higher.

3) Must have a healthy surplus

It goes without saying that a term till 99 is more pricier than a normal term that covers till 65 years old.

In my opinion, a term till 65 is a need – income protection.

But if you have the budget, then extending a term till 99 can be the best combination of income protection and creating a legacy.

Just be prepared to pay the premiums and don’t go breaking the bank.

So if you satisfy these 3 criteria, then only a term till 99 can be something for you to consider.

All in All…

Death is certain – 100% Guaranteed.

The question is when?

Earlier or Later?

With a term till 99…

You ensure that your income is protected if it happens Earlier

And at the same time…

You ensure you can leave a legacy if it happens Later

Either way, you Win.

What’s Next?

Numbers make the most sense.

If you’re curious to see how much premiums you would need to pay for a term till 99…

Take the first step by comparing different companies and get free quotes online now. Compare and Get FREE Quotes Now!