Healthcare in Singapore is world-class. It is also expensive, and it is getting more so.

Whether you are planning for a hospital stay, reviewing your insurance coverage, or simply trying to understand where your money goes, knowing the real cost of healthcare in Singapore matters.

Here is a compilation of the most important statistics on healthcare costs in Singapore. This page will be updated regularly to reflect the latest information.

Read on.

Key Healthcare Cost Statistics in Singapore (2026)

- Healthcare CPI inflation was 2.7% in 2025; insurer-reported costs rose 15.5%

- The government spent $18.2 billion on healthcare in FY2024

- The same procedure can cost up to 6 times more at a private hospital than a subsidised public ward

- Late-stage cancer treatment can cost $100,000 to $200,000 per year

- MediShield Life premiums are rising by up to 35% over three years (2025–2028)

- IP rider co-payment cap has doubled from $3,000 to $6,000 from April 2026

- Households spend an average of $474 per month on health

- Healthier SG provides fully subsidised screenings and vaccinations for enrolled citizens

- Long-term care costs an average of $2,952 per month, up 27% since 2018

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

A Quick Overview of Healthcare in Singapore

Singapore punches well above its weight when it comes to healthcare quality.

In 2025, Singapore General Hospital (SGH) was ranked ninth among the world’s best hospitals out of 2,400 evaluated globally, making it the only Asian hospital in the top 10. Singapore has also consistently ranked as one of the most efficient healthcare systems in the world, according to the Bloomberg Health-Efficiency Index.

Singaporeans also benefit from one of the highest life expectancies in the world, currently at 83 years.

But a high-quality healthcare system comes with a cost. And in recent years, that cost has been rising on multiple fronts: government spending, insurance premiums, and household out-of-pocket expenses have all trended upward.

So let’s look at the numbers.

1) Singapore’s healthcare inflation rate was 2.7% in 2025, while insurer-reported medical costs rose by 15.5%

There are two ways to measure healthcare inflation in Singapore, and both tell a different part of the same story.

The national CPI

The first is the Consumer Price Index (CPI), published by the Singapore Department of Statistics (SingStat). This measures what consumers actually pay for healthcare at the point of service, covering everything from polyclinic visits to private specialist consultations.

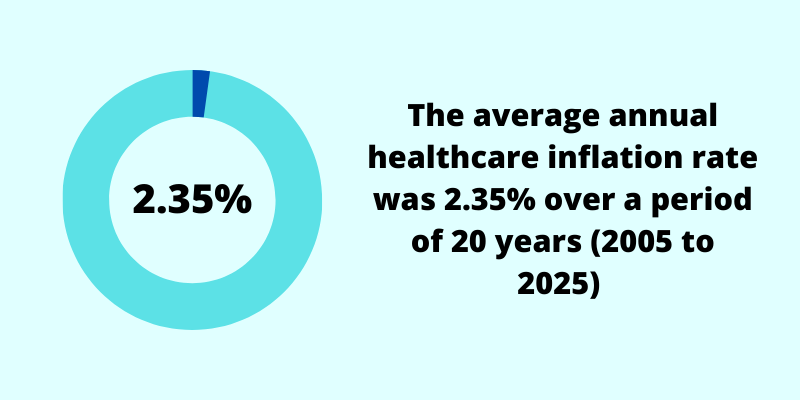

According to SingStat, Singapore’s CPI-Healthcare rose by 2.7% in 2025, down from 3.9% in 2024. Over the past 20 years from 2005 to 2025, the average annual compound healthcare inflation rate was 2.35%, compared to 2.14% for headline inflation over the same period.

In other words, the rising cost of healthcare has consistently outpaced the rising cost of living.

But the headline figure masks an important split. Outpatient care services fell 0.3% in 2025, and inpatient care services edged down 0.1%. The overall CPI-Healthcare figure was pushed upward almost entirely by health insurance premiums, which surged 12.7% in 2025, up sharply from 5.1% in 2024.

The insurer survey

The second measure comes from insurer surveys. According to WTW’s 2026 Global Medical Trends Survey, Singapore’s medical inflation rate as reported by insurers was 15.5% in 2025, and is projected to reach 16.9% in 2026. This is above the Asia Pacific regional average of 14%.

Why the gap between 2.7% and 15.5%?

The CPI measures what consumers pay, including subsidised public healthcare. The WTW figure measures what healthcare is actually costing insurers, factoring in rising utilisation and more expensive treatments on top of price increases. They are measuring different things.

2) The government spends more than $18 billion a year on healthcare

Singapore’s government has long treated healthcare as a national priority, and the spending figures reflect that.

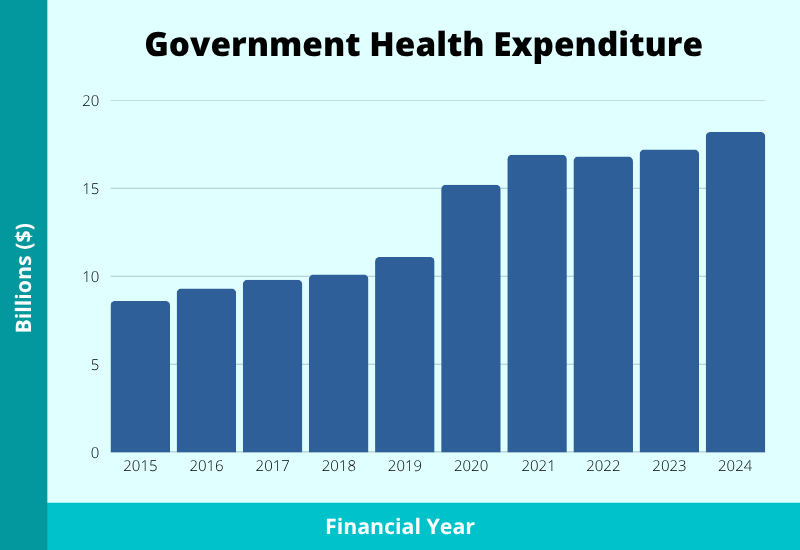

Government health expenditure has grown significantly over the past decade and a half, crossing the $10 billion mark in FY2018 and continuing to climb in the years since.

Here is the government health expenditure over the years:

| Financial Year | Government Health Expenditure |

|---|---|

| 2024 | $18.2 billion |

| 2023 | $17.2 billion |

| 2022 | $16.8 billion |

| 2021 | $16.9 billion |

| 2020 | $15.2 billion |

| 2019 | $11.1 billion |

| 2018 | $10.1 billion |

| 2017 | $9.8 billion |

| 2016 | $9.3 billion |

| 2015 | $8.6 billion |

Government Health Expenditure figures are actual figures up to FY2023. The FY2024 figure represents operating and development expenditure, as the consolidated GHE figure is not yet available.

The direction of travel is clear: spending is not coming down. And with an ageing population placing greater demand on healthcare services, the government has signalled that expenditure will continue to rise.

That said, higher spending does not automatically mean higher costs for individuals. A significant portion of this expenditure goes towards subsidies that reduce what Singaporeans pay out of pocket, particularly for those in lower-income households.

3) The same hospital procedure can cost up to six times more depending on your ward and hospital

There is no single answer to “how much does a hospital stay cost in Singapore?” The bill depends on what you are being treated for, which hospital you go to, and which ward you choose. The same procedure can cost vastly different amounts.

Take a knee joint replacement as an example:

| Ward | Total Bill (Median) |

|---|---|

| Public – C | $6,993 |

| Public – B2 | $7,567 |

| Public – B1 | $24,358 |

| Public – A | $25,738 |

| Private | $48,746 |

The same pattern plays out for heart and stroke-related treatments:

| Procedure | Ward | Total Bill (Median) |

|---|---|---|

| Heart, Multivessel Percutaneous Coronary Intervention | Public – C | $7,027 |

| Public – B2 | $8,100 | |

| Public – B1 | $25,572 | |

| Public – A | $26,563 | |

| Private | $58,852 | |

| Stroke and Other Cerebrovascular Disorders | Public – C | $2,503 |

| Public – B2 | $2,795 | |

| Public – B1 | $7,557 | |

| Public – A | $9,525 | |

| Private | $21,047 |

A few things stand out. First, the jump from a B2 ward to a B1 ward in a public hospital can more than double your bill. Second, choosing a private hospital over a subsidised public ward can multiply costs by four to eight times for the same procedure.

These figures are based on past MOH published bill data and are meant to illustrate the scale of variation. For the most current estimates specific to your procedure, use MOH’s bill estimator.

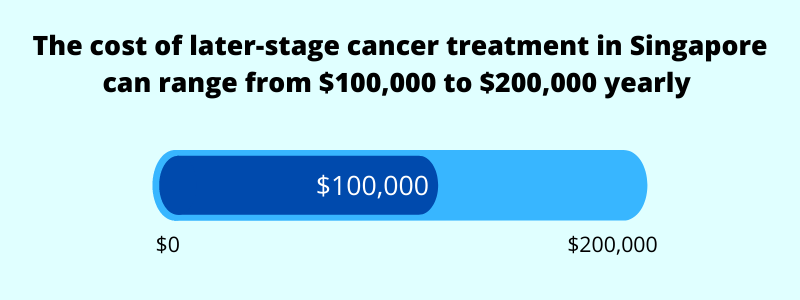

4) The costs of treating a critical illness can amount to $100,000 to $200,000 yearly

Most Singaporeans are not too worried about minor injuries. A trip to the GP, a short hospital stay, and life goes on.

What people fear more is a critical illness.

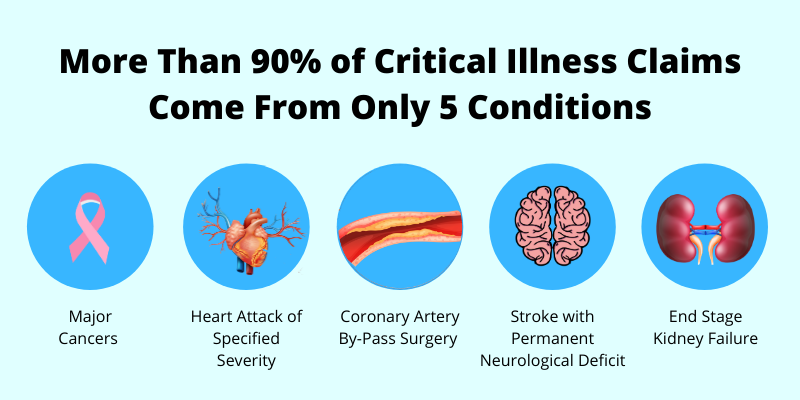

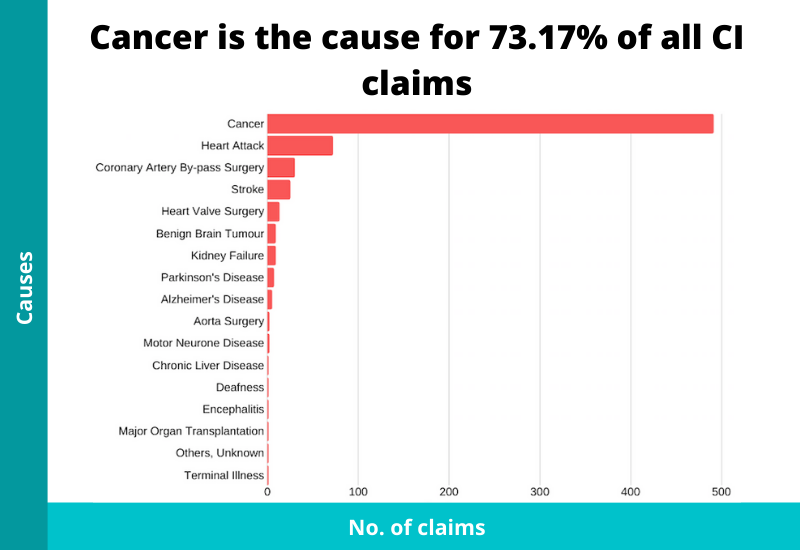

The top five critical illnesses in Singapore are major cancers, heart attack of specified severity, coronary artery by-pass surgery, stroke with permanent neurological deficit, and end-stage kidney failure.

Together, they account for 93.45% of all CI claims, with cancer alone making up 73.17%.

The risk is also higher than most people expect. One in four Singaporeans may develop a critical illness in their lifetime.

The financial impact runs deeper than most people plan for. Late-stage cancer treatment can cost $100,000 to $200,000 per year, and that is before accounting for lost income during recovery.

This is where many Singaporeans are exposed. CI claims make up 49.68% of all life insurance claims, yet the average CI claim payout is only $52,343. The LIA recommends having 3.9 times your annual income in CI coverage. For someone earning $5,000 a month, that works out to $234,000, more than four times the average payout.

5) MediShield Life premiums are rising by up to 35% over three years

MediShield Life is Singapore’s national health insurance scheme. It is compulsory for all citizens and permanent residents, and premiums are fully payable from your MediSave account.

Following a review in 2024, the government accepted recommendations to enhance the scheme’s benefits and adjust premiums accordingly. The increases are being phased in over three years, from April 2025 to March 2028, with the total increase capped at 35% and the average increase per policyholder reaching 22% by the end of the third year.

Here are the current annual MediShield Life premiums, effective from 1 April 2025:

| Age Next Birthday | Annual Premium (before subsidies) |

|---|---|

| 1–20 | $200 |

| 21–30 | $295 |

| 31–40 | $503 |

| 41–50 | $637 |

| 51–60 | $903 |

| 61–65 | $1,131 |

| 66–70 | $1,326 |

| 71–73 | $1,643 |

| 74–75 | $1,816 |

| 76–78 | $2,027 |

| 79–80 | $2,187 |

| 81–83 | $2,303 |

| 84–85 | $2,616 |

| 86–88 | $2,785 |

| 89–90 | $2,785 |

| >90 | $2,826 |

Note that these are gross premiums before subsidies. Lower and middle-income Singaporeans, particularly in older age groups, receive premium subsidies of up to 60%.

These are also not the final rates. As the phased increase continues through to March 2028, premiums will rise further before the cycle is complete.

Singaporeans who want coverage beyond what MediShield Life provides, particularly for private hospital stays, can upgrade with an Integrated Shield Plan. Those plans have also seen significant changes recently, which we cover in the next section.

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

6) New IP rider rules from April 2026 double the co-payment cap to $6,000

Integrated Shield Plans (IPs) are optional upgrades to MediShield Life that provide coverage for higher ward classes and private hospitals. Most policyholders pair their IP with a rider to reduce their out-of-pocket costs further.

From 1 April 2026, MOH introduced new requirements for IP riders that change how much policyholders are expected to share in their own medical costs.

The two key changes are:

New riders can no longer cover the minimum IP deductibles, which range from $1,500 to $3,500 depending on ward class. Previously, some riders could cover these deductibles entirely, meaning policyholders paid nothing upfront before their insurance kicked in.

The annual co-payment cap has been raised from $3,000 to $6,000, excluding the deductible. The minimum 5% co-payment requirement remains.

In practical terms, policyholders on new riders will face higher potential out-of-pocket costs when they make a claim. The flip side is that new rider premiums are projected to be around 30% lower on average compared to existing maximum coverage riders.

Why these changes? MOH data shows that policyholders with maximum coverage riders are 1.4 times more likely to make a claim, and their average claim size is also 1.4 times higher. The changes are designed to encourage more mindful use of healthcare services and bring down overall system costs.

7) Singaporean households spend an average of $474 per month on health

According to the Singapore Department of Statistics’ Household Expenditure Survey, households spent an average of $5,931 per month on goods and services in 2023. Of that, health accounted for $474 per month, or 6.7% of monthly household expenditure.

The largest component within health spending was outpatient services, at $293 per month. This covers GP visits, specialist consultations, health screenings, and A&E visits.

Separately, insurance and financial services accounted for $590 per month. This sits under the broader “Others” category in SingStat’s breakdown and covers all types of insurance, not just health insurance.

8) Healthier SG is making preventive care more affordable

Rising healthcare costs are partly a demand problem. The more Singaporeans rely on treatment, the more the system costs for everyone. The government’s response is to shift the focus upstream.

Healthier SG is a national preventive care initiative that encourages Singaporeans to enrol with a regular family doctor, build an ongoing care relationship, and take a more proactive approach to their own health.

For enrolled citizens, the practical benefits are immediate. Nationally recommended vaccinations are provided at no cost at participating Healthier SG clinics. Health screenings covering cardiovascular risk factors, diabetes, high blood pressure, high cholesterol, and selected cancers including colorectal, cervical, and breast cancer are fully subsidised for eligible enrollees. The onboarding health consultation is also fully paid for by the government.

The intent is clear: catch problems early, before they become expensive ones. A screening that costs nothing today could prevent a hospitalisation that costs tens of thousands later.

For Singaporeans who have not yet enrolled, it is worth doing. The benefits are meaningful and the process is straightforward through the HealthHub app or a participating GP clinic.

9) Long-term care costs an average of $2,952 per month

Most conversations about healthcare costs focus on hospital bills and insurance premiums. But for many Singaporeans, the bigger financial challenge comes later, when a family member can no longer care for themselves.

According to a 2024 study by Singlife, the average monthly cost of caring for a loved one with long-term care needs is $2,952, a 27% increase from 2018. Notably, 37% of respondents had underestimated this, initially guessing under $2,000 per month.

One in two healthy Singaporeans aged 65 could experience severe disability at some point, making this a risk most families will eventually face.

Singapore’s national scheme for this is CareShield Life, which pays out $689 per month in 2026 if you become severely disabled. Against an average monthly care cost of $2,952, that leaves a significant gap. Supplementary plans can provide up to $5,000 per month on top of the base payout, and government subsidies can cover up to 75% of nursing home costs for eligible individuals. MOH has also announced enhanced long-term care subsidies from July 2026 as part of Budget 2025.

Why Is Healthcare in Singapore So Expensive (and Rising)?

Healthcare in Singapore is expensive, and getting more so, because demand keeps outgrowing supply. Four things drive it: an ageing population, newer and pricier treatments, rising manpower and operating costs, and insurance that softens the price at the point of care.

1) An ageing population that is living longer

Singapore is ageing fast. The share of citizens aged 65 and above rose from 13.1% in 2015 to 20.7% in 2025, and by 2030 around 1 in 4 will be 65 or older, even as the working-age base supporting them shrinks to just 3.3 residents aged 20 to 64 per senior.

Older people need more care, and although Singaporeans are among the longest-lived in the world, the final years tend to be the least healthy and the most medically expensive.

It is not only about age. Chronic conditions such as diabetes, high blood pressure, and obesity are becoming more common and appearing earlier, each one meaning years of ongoing treatment rather than a one-off cost.

2) Medical advances mean more treatment, not less

Better technology rarely lowers total spending. Conditions that were untreatable a generation ago can be treated today, and newer options tend to work better but cost more.

Drugs are the clearest example: immunotherapies and the latest cancer treatments can run many times the price of what they replace, which is why insurers now rank pharmaceutical advances among the top drivers of medical cost inflation.

Earlier detection saves lives and lowers the cost per case, but it also puts more people into screening, diagnosis, and follow-up. More capability means more consumption.

3) Manpower and operating costs make up most of the bill

Healthcare is labour-intensive: manpower is about 60% of hospital costs, and a shortage of nurses and allied health workers has pushed wages up as providers compete for the same pool.

Wages are only part of it. Hospitals also carry rising rent, utilities, and equipment costs, and in land-scarce Singapore high property prices feed straight into running a facility.

The government has expanded the workforce and published fee benchmarks to rein in private charges, but as these costs rise, so does the price of every consultation, procedure, and ward day, part of why the average hospital bill keeps climbing.

4) Insurance made healthcare feel free, and usage followed

When patients pay little at the point of care, they tend to use more of it. MOH found that policyholders on maximum-coverage IP riders claim more often and in larger amounts, a pattern sometimes called buffet syndrome.

Higher claims feed higher premiums, and those premiums have themselves become a driver of headline inflation: health insurance premiums rose 12.7% in 2025.

Breaking this loop is the point of the recent MediShield Life adjustments and the April 2026 rider rules, though only the next few years of data will show whether they work.

What’s Next?

The cost of healthcare in Singapore is real, and it is rising across the board.

Medical inflation is climbing, insurance premiums are increasing, and long-term care needs are often far more expensive than people expect. The numbers in this article are not meant to alarm, but to inform.

The best defence is a combination of healthy living and the right financial protection.

Start with the basics: MediShield Life provides a baseline for all Singaporeans, and an Integrated Shield Plan is worth considering if you want more comprehensive coverage, particularly for private hospital stays.

And with CI affecting one in four Singaporeans over their lifetime, having an early critical illness plan that pays out on diagnosis gives you financial flexibility when you need it most. If a standalone CI plan is not on the cards, CI coverage attached to a term or whole life insurance policy can also serve that purpose.

Take some time to review your coverage today.

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.