Every Singaporean and Permanent Resident has a CPF account, and the savings inside it build up quietly over a working lifetime.

What most people don’t realise is that those savings aren’t treated like the cash in your bank account, while you’re alive or after you’re gone.

Making a CPF nomination might feel like admin you’ll get to eventually. But it’s one of the simplest and most important steps in proper estate planning, it’s free, and it can be done entirely online.

Here’s everything you need to know, and the exact steps to make one.

Too Long; Didn’t Read

When you pass away, your CPF savings don’t form part of your estate. They’re handled separately from your other assets, and a will can’t cover them.

So if you haven’t made a CPF nomination, your savings won’t simply go where you’d want them to. They’ll be distributed according to the law, it can take months, and a fee will be deducted along the way.

Making a CPF nomination fixes all of that. It’s free, your nominees receive the money directly from the CPF Board at no cost, and you can now appoint up to 15 nominees online in a single sitting.

There’s more to it though. Read on for the full picture.

SIDE NOTE

Most people's finances aren't a plan. They're a collection of separate decisions: a policy bought years ago, investments that don't talk to each other, a will that's still on the to-do list.

If that sounds familiar, there's a fix that doesn't require becoming a finance expert.

Here's the 7-step framework we use to organise everything into one system.

What Is a CPF Nomination

A CPF nomination lets you decide who receives your CPF savings when you pass away, and exactly what percentage each person gets.

To make one, you need to be at least 16 years old and of sound mind. The age of 16 lines up with the minimum age to work and earn wages in Singapore, according to CPF Board.

That “sound mind” requirement is also why it pays to do this sooner rather than later. If you lose mental capacity first, you can no longer nominate, and your donee under a Lasting Power of Attorney can’t do it for you. According to CPF Board, only the Courts can make or revoke a nomination for someone who lacks mental capacity, a slow and costly route that may not land where you’d have wanted.

It isn’t compulsory. But as you’ll see, there’s very little reason not to do it, especially when it costs nothing.

And yes, Muslims can make a CPF nomination too. The Fatwa Committee of MUIS has ruled that a CPF nomination can be considered a hibah, or gift, because it’s made while you’re still alive.

Who Can Be Nominated

In short, almost anyone. A nominee can be a person or a legal entity, including:

- Your spouse

- Family members

- Friends

- Foreigners

- Charities and other organisations

There’s no limit to how many people you’d like to provide for in principle, though the way you make your nomination sets a practical cap (more on that later).

That said, if a nominee falls into one of these three groups, it’s worth paying closer attention.

1) Below 18 years old

If your nominee is under 18 when you pass away, the money due to them is held in trust by the Public Trustee’s Office (PTO) until they turn 18. (The exception is a nominee who is a minor widow.)

There’s a one-time charge for this, taken from the CPF money. It follows the same tiered scale the PTO uses for un-nominated CPF, set out in the fee table in the “Without a nomination” section further down.

The money doesn’t just sit idle, though. It’s invested, and it earns interest for the child. A separate fee applies to the interest earned:

| Amount of interest earned | Charge |

|---|---|

| For the first $1,000 | 5.50% |

| For the next $1,000 | 4.50% |

| For the next $1,000 | 3.50% |

| For amounts in excess of $3,000 | 2.25% |

2) Lacks mental capacity

If your nominee lacks mental capacity, the CPF savings are paid to their court-appointed deputy or to a donee under a Lasting Power of Attorney. That person is required to act in the nominee’s best interests.

3) Bankrupt

If your nominee is still an undischarged bankrupt when they become entitled to the CPF savings, the CPF Board will inform the Official Assignee. The money may be paid to the Official Assignee instead.

What Types of CPF Savings Are Covered

A CPF nomination doesn’t cover everything in the CPF universe. It applies to specific accounts and items only.

| A CPF nomination covers: | It doesn’t cover: |

|---|---|

| Savings in your Ordinary, Special, MediSave, and Retirement Accounts | Property bought using your CPF savings |

| Unused CPF LIFE premiums | Payout from the Dependants’ Protection Scheme (DPS) |

| Discounted Singtel shares | Investments and returns under the CPF Investment Scheme |

One point that trips people up: a property bought with your CPF savings isn’t distributed through your nomination. On death, the CPF you used for it isn’t refunded to your CPF account, according to CPF Board. The property passes to the surviving co-owner if it’s held in joint tenancy, or forms part of your estate (distributed by your will or by intestacy) if it’s held as tenancy-in-common. Your nomination only deals with the savings sitting in your CPF accounts.

The 3 Types of CPF Nominations

There are three types of CPF nomination you can make:

- Cash nomination

- Enhanced Nomination Scheme (ENS)

- Special Needs Savings Scheme (SNSS)

Most Singaporeans only ever make the Cash nomination, which is the default. Here’s how each one pays out:

| How it’s paid to nominees | |

|---|---|

| Cash | Received in cash, via GIRO or cheque |

| Enhanced Nomination Scheme (ENS) | Transferred into the nominee’s own CPF accounts |

| Special Needs Savings Scheme (SNSS) | Paid out to the nominee on a regular basis |

The ENS and SNSS options can’t be done online. You’ll need to make those at a CPF Service Centre.

What Happens to Your CPF When You Pass Away

This is the part that shows why a nomination matters so much.

It doesn’t make a difference whether you have a will, because a will can’t include CPF savings. So really there are only two scenarios: passing away with a nomination, and passing away without one.

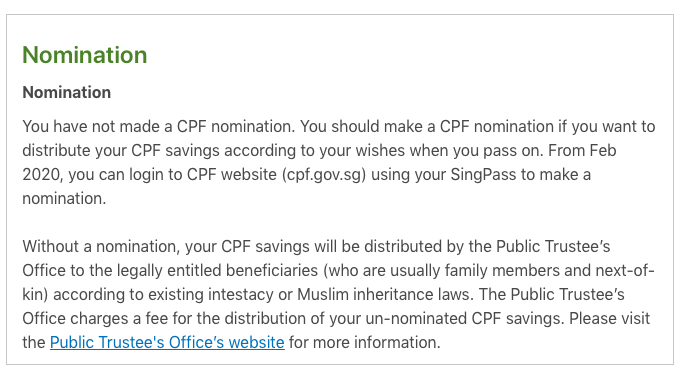

Without a nomination

When you pass away without a CPF nomination (or your nomination was revoked), your CPF savings don’t form part of your estate.

That has one upside. Any creditors you owe generally can’t claim those savings, so the money is preserved for your family.

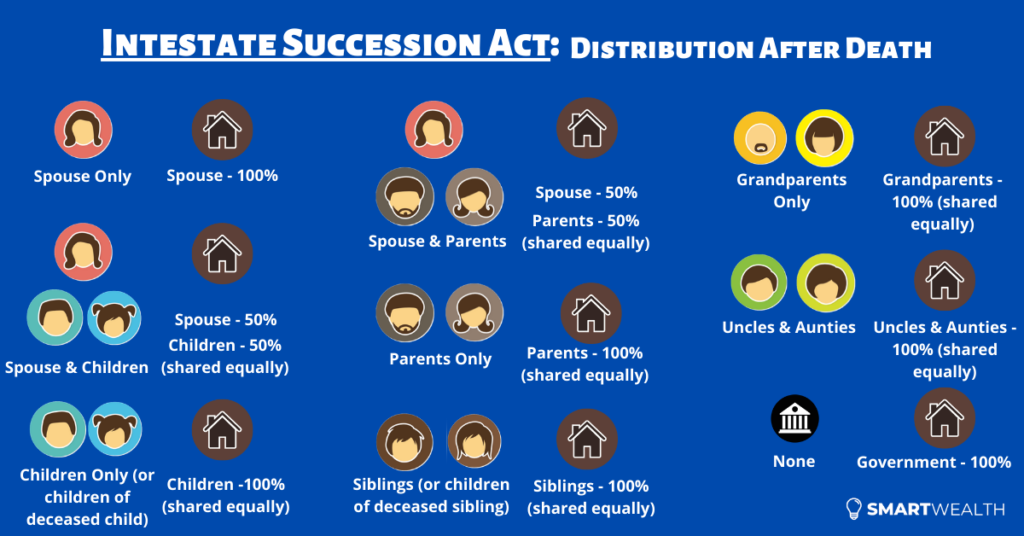

But the trade-offs are real. Your savings get sent to the Public Trustee’s Office, which distributes them in cash according to the Intestate Succession Act for non-Muslims, or the inheritance certificate for Muslims. In other words, the law decides who gets what, not you.

It also takes time. The Public Trustee’s Office can take up to six months just to establish which family members are legally entitled, according to CPF Board. And there’s a fee, deducted straight from your CPF savings (minimum $15, inclusive of GST, and it can’t be waived):

| Amount of CPF money | Charge |

|---|---|

| For the first $1,000 | 2.400% |

| For the next $9,000 | 1.500% |

| For the next $240,000 | 0.750% |

| For the next $250,000 | 0.450% |

| For amounts in excess of $500,000 | 0.300% |

To put that in real terms, the fee on $100,000 of CPF savings works out to around $900. The bigger your CPF balance, the bigger the charge.

After that, your beneficiaries still need to submit documents (death certificate, NRIC, and so on), and the Public Trustee’s Office distributes the money within about four weeks of receiving a complete set.

And this isn’t a rare edge case. As at 31 December 2024, a striking $184 million of un-nominated CPF savings sat unclaimed with the Public Trustee, according to the Insolvency and Public Trustee’s Office. Around $67 million of that was added in 2024 alone. You can read more in our breakdown of unclaimed and unnominated assets in Singapore.

There’s a worst case, too. If you leave no nomination and no relatives entitled under intestacy law, your CPF can ultimately pass to the State as bona vacantia. A nomination is the simplest way to make sure your savings reach a person, not the government.

With a nomination

With a nomination, all of that falls away.

Your CPF savings go exactly where you wanted, in the proportions you chose. The CPF Board contacts your nominees within 15 working days of being notified of your passing, and they receive the money in cash, with no fee taken out.

That’s the whole point of a nomination. It spares the people you leave behind a slow, costly process at the worst possible time, and you can update it whenever your life changes.

One worry you can set aside: there’s no death tax on any of this. Singapore abolished estate duty for deaths on or after 15 February 2008, according to IRAS, and CPF savings your nominees receive aren’t taxed as income.

CPF Nomination vs a Will: What’s the Difference

A common misconception is that a will takes care of everything, CPF included. It doesn’t. Your CPF savings sit entirely outside your will, so the two tools do different jobs and you generally need both.

| CPF nomination | Will | |

|---|---|---|

| What it covers | CPF savings (OA, SA, MA, RA), unused CPF LIFE premiums, Discounted Singtel shares | Almost everything else: bank savings, property, investments, personal belongings |

| Does it cover CPF? | Yes, this is the only way to direct your CPF | No, a will cannot distribute CPF savings |

| Cost to set up | Free | Varies (DIY to lawyer-drafted) |

| If you don’t have one | CPF goes to the Public Trustee, distributed by intestacy law, with a fee | Other assets distributed by intestacy law |

In short, a CPF nomination decides who gets your CPF, and a will decides who gets the rest. Skip either one and that slice of your estate falls back on the law. If you’d like to see exactly how that default split works, we’ve covered what happens when you die without a will.

How Your Nominees Access Your CPF Information

In the past, only people you specifically authorised could view your CPF account details after your death. That made things awkward for nominees who simply wanted to know what was there.

Since 1 February 2024, that’s improved. If you’re a nominee of someone who has passed away, you can now view the deceased member’s CPF information on the Deceased CPF Member Dashboard by logging in with your Singpass. You’ll need to wait at least 10 working days after the death has been registered.

If you’re an eligible family member under intestacy law but weren’t named as a nominee, you can still request access by submitting a FormSG application with documents proving your relationship. The CPF Board reviews these within 10 working days.

How to Check If You Already Have a Nomination

Not sure whether you’ve made one before? It’s quick to check.

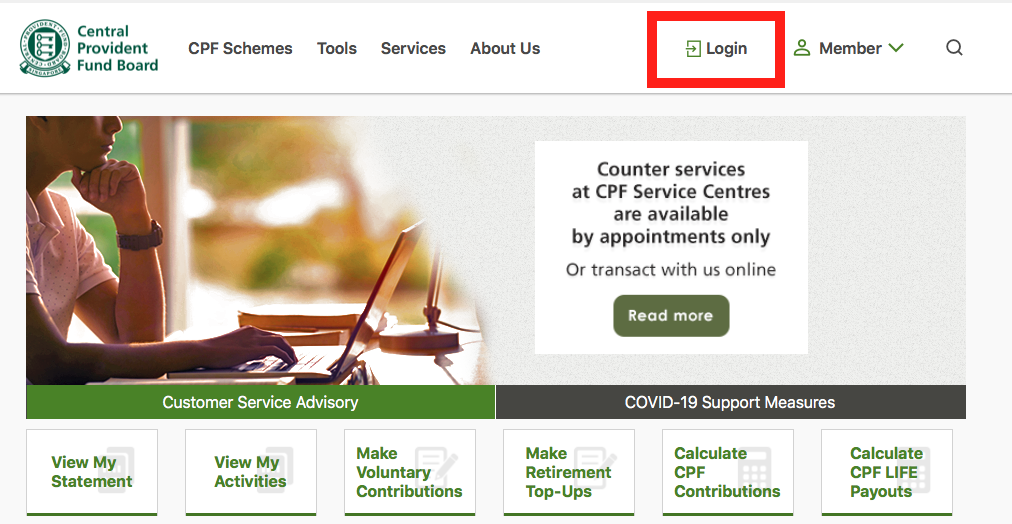

Step 1: Go to cpf.gov.sg and log in with your Singpass.

Step 2: Head to your CPF dashboard and look under your account services or messages for any nomination record.

Step 3: If no nomination is on file, that’s your cue to make one. The steps are below.

One quirk to know: a nomination made more than 30 years ago can’t be viewed online, according to CPF Board. If yours dates that far back, write to the CPF Board to confirm what’s on file. The same goes if you’d simply rather not log in.

3 Ways to Make a CPF Nomination

There are three ways to make a nomination.

1) Online

By far the most convenient option, and the one most people now use. You can appoint up to 15 nominees in the online form. If you want more than 15, you’ll need to visit a Service Centre.

Two things to note. The online route is for the Cash nomination only, and you’ll still need to line up two witnesses (they complete their part digitally).

QUICK CHECK

Can you answer these three questions?

1) How much would your family receive if something happened to you tomorrow?

2) What monthly income will your savings and investments actually produce at 65?

3) Who gets your assets, in what proportion, if you never get round to a will?

Most people can answer one at best. Not because they're careless, but because nobody's shown them the order to work through things.

That order exists. Here's the 7-step framework, from income and protection through to investments and estate planning.

2) Hardcopy application form

You download and print the form, complete it in front of two witnesses, and post it to the CPF Board. Slower, but it’s there if you prefer paper.

3) At a CPF Service Centre

There are five CPF Service Centres islandwide. It’s best to book an appointment first. The Customer Service Executives can act as your witnesses, so it’s a good option if you can’t find two of your own.

This is also the only route for the non-default schemes, the Enhanced Nomination Scheme and the Special Needs Savings Scheme.

The steps below cover the online method, since that’s what most people will use.

How to Make a CPF Nomination Online (5-Step Process)

Step 1: Make sure you have a Singpass

You can’t make an online nomination without Singpass, so have your login ready.

Step 2: Gather your nominees’ details

Decide who you’re nominating and what percentage each person receives. Keep a notepad handy, digital or physical, because the next steps need more details too.

For each nominee you’ll need:

- Full name as per NRIC

- The percentage allocated (all nominees together must add up to 100%)

- NRIC, FIN, or passport number

- Relationship to you

- Email address (optional)

- Mailing address (for foreign passport or ID holders)

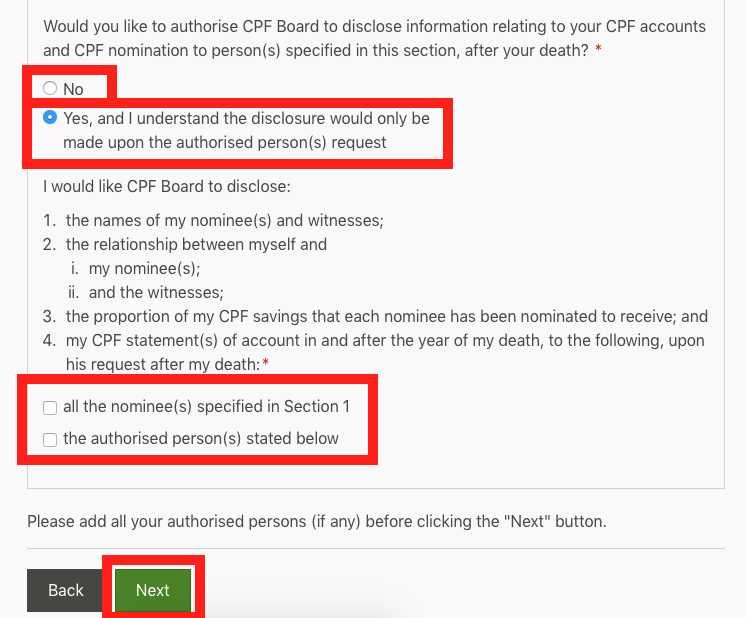

Step 3: Decide on disclosure of your CPF information

You can choose to keep your nomination and CPF details completely private while you’re alive. If you do, not even your spouse or family can check whether they’re a nominee.

After your death, your CPF information can be released to your nominees, and to up to five authorised persons if you appoint them. You’ll need each authorised person’s full name, identification number, and relationship to you.

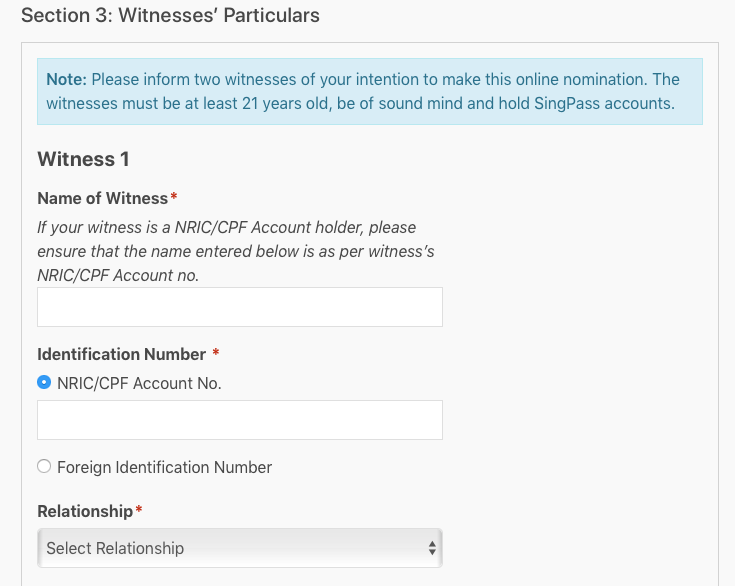

Step 4: Gather your witnesses’ details

You need two witnesses. Each must be at least 21 years old, have mental capacity, and hold a Singpass. They can’t be your nominees, and you can’t witness your own nomination.

The details you’ll need from each of them:

- Full name as per NRIC

- NRIC, FIN, or passport number

- Relationship to you

- Email address or Singapore-registered mobile number

- Mailing address (for foreign passport or ID holders)

Let your witnesses know in advance, because once you submit, they have seven calendar days to acknowledge the nomination with their own Singpass. A nice touch: you can be their witness in return, so a small group of friends can sort this out together in one go.

Step 5: Submit the nomination online

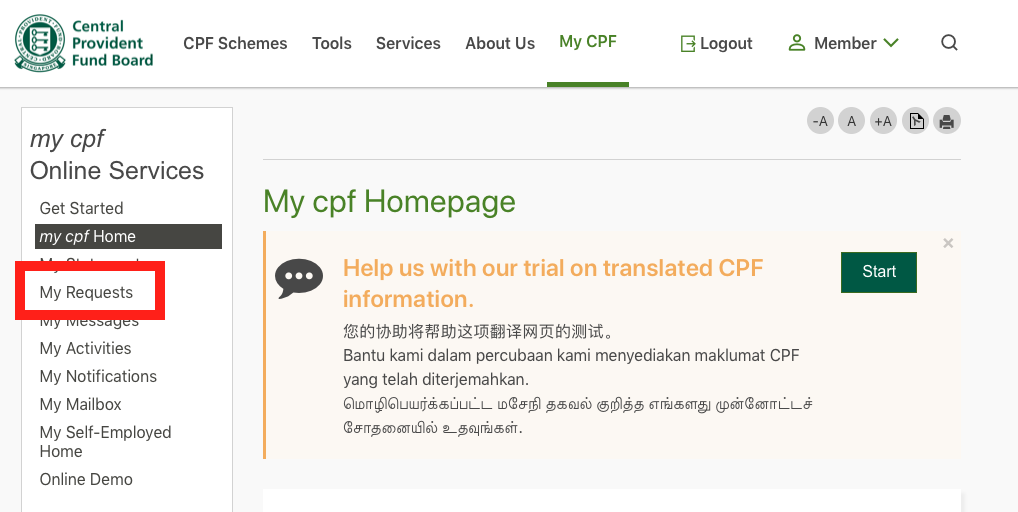

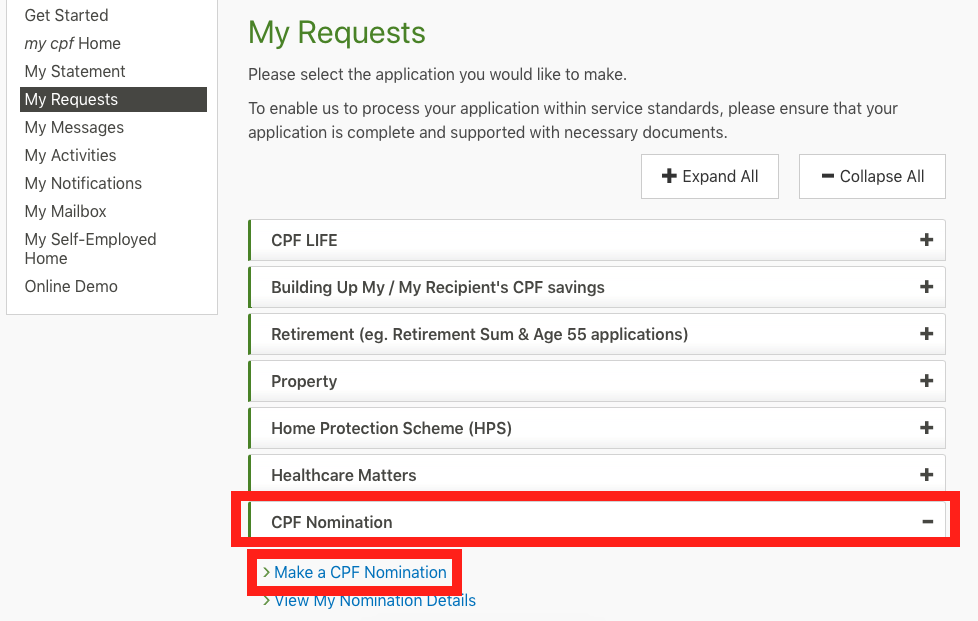

With everything gathered, this last step is mostly data entry. Head to cpf.gov.sg, click “Login”, and sign in with your Singpass.

Once you’re logged in, click “My Requests” on the left-hand panel.

Scroll to “CPF Nomination”, then click “Make a CPF Nomination”.

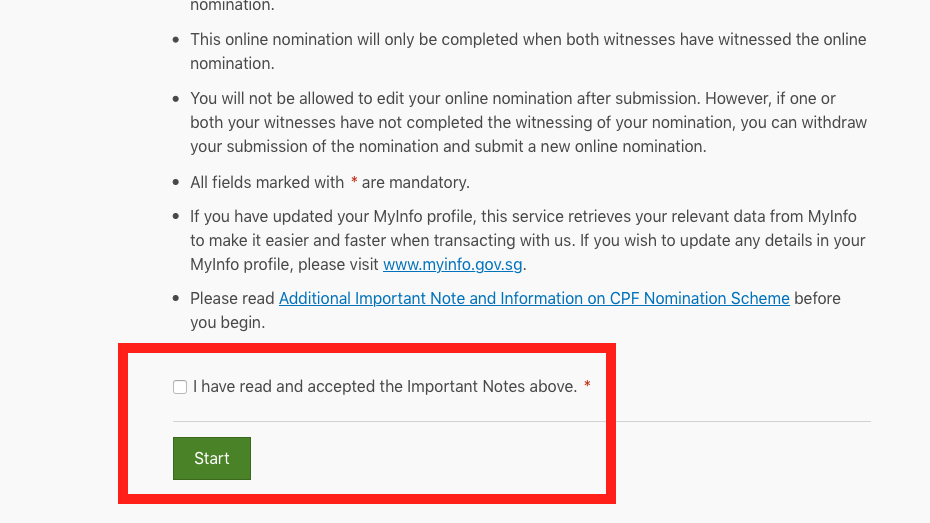

Check your details, read the notes, tick the box, then click “Start”.

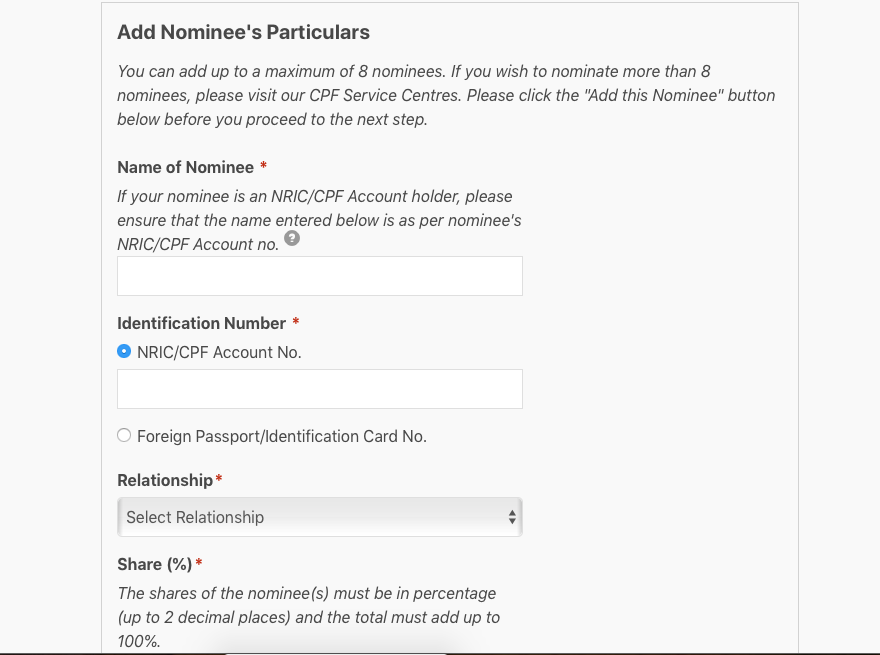

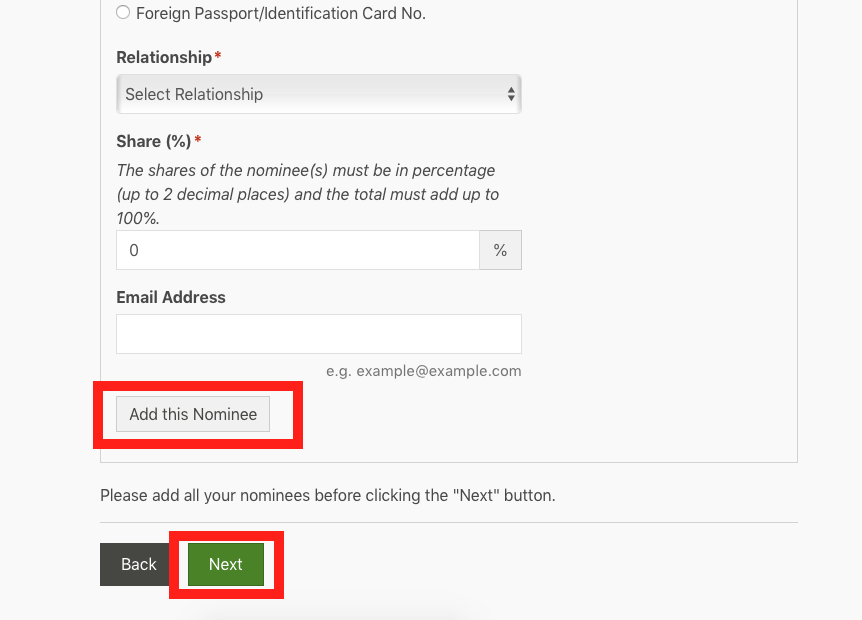

Using the information you’ve gathered, enter your nominee’s particulars.

After entering each nominee’s particulars, click “Add this Nominee”. Add more nominees if needed, or click “Next” to continue.

Next is the Authorised Person(s) section. You can choose either to keep your CPF information private from everyone, or to disclose it to all your nominees and up to five authorised persons. Make your selection.

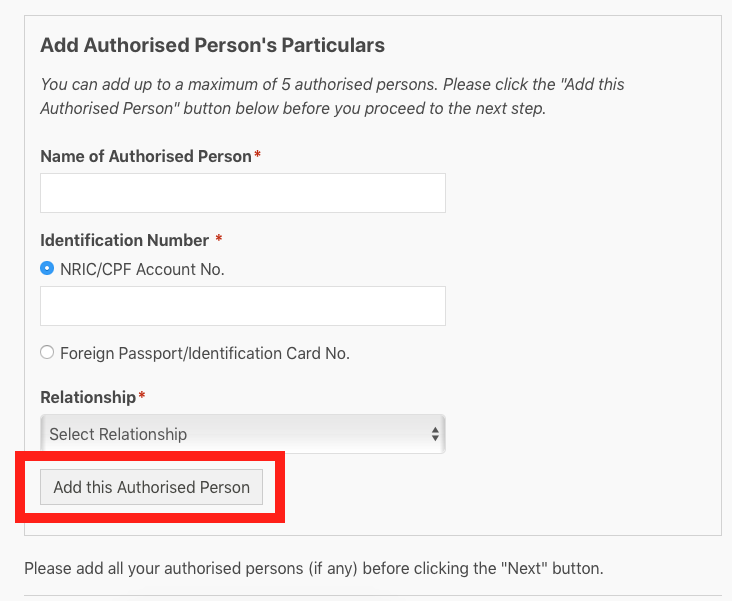

If you’re appointing any authorised persons, add their details, then click “Add this Authorised Person”. Add more if needed, or click “Next” to continue.

Next is the witnesses’ particulars section. Enter the details of your two witnesses, then click “Next”.

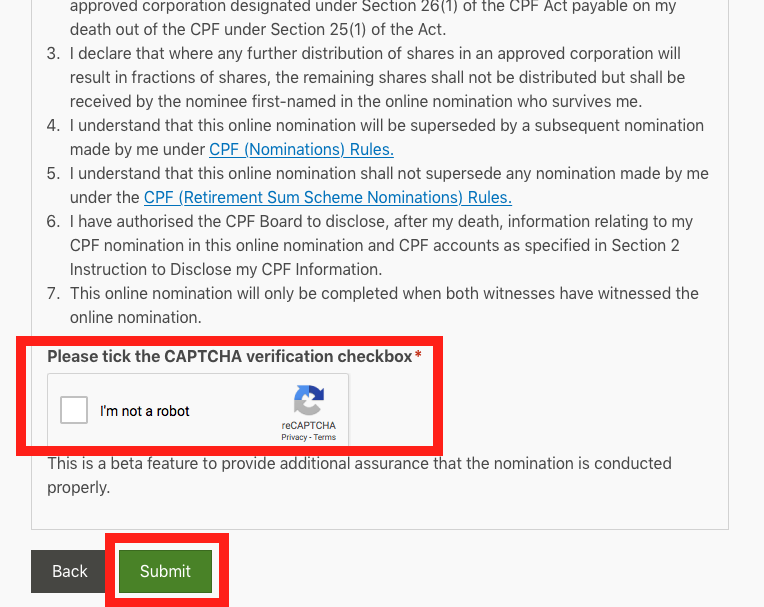

You’ll arrive at the final step, the submission page. Check that all the details are correct. Everything you entered for your nominees, authorised persons, and witnesses will be shown. Read through the declaration, confirm you’re not a robot, then click “Submit”.

And that’s your part done. Your witnesses then complete theirs within seven days.

What Happens to an Existing Nomination

Life changes, and some events affect a nomination automatically while others don’t. Here’s how the common ones work.

After marriage

Getting married automatically revokes your existing nomination. If you die after marrying without redoing it, your CPF is treated as though you never nominated at all, and it goes through intestacy. Worth sorting promptly.

After divorce

A divorce does not revoke your nomination. It stays exactly as it was, on the logic that you might still want to provide for an ex-spouse, say for your children’s sake.

This one catches people out. An ex-spouse you named years ago stays entitled to your CPF until you actively change it, which has led to real disputes when families assumed the divorce had settled things. If that’s not what you want, update it.

After remarriage

Same as a first marriage. Remarriage automatically revokes your existing nomination.

After a newborn

A new child does not automatically revoke your nomination. To include your child, you’ll need to redo it.

After a nominee passes away

If a nominee dies before you, your nomination isn’t revoked. If you then pass away, that nominee’s share is split among the surviving nominees in proportion to their original allocations.

If none of your nominees are still living, the savings fall back on intestacy distribution instead. So it’s worth refreshing your nomination if one of them passes.

How to Change or Revoke a Nomination

Want to change your nominees or their percentages? Just make a new nomination. It overrides the previous one entirely. There’s no separate “edit” process, and like the original, it’s free.

It’s a good habit to review your nomination every year or so, and especially after any big life event.

What’s Next?

Hopefully you’ve got a clear picture of CPF nominations now. If you haven’t made one yet, set aside a few minutes and follow the online steps above. If you already have, that’s one important box ticked.

A CPF nomination is only one part of estate planning, though. Two more pieces round it out:

First, making a nomination on your insurance policies with a death benefit lets your family receive those proceeds without the legal process, giving them quick access to cash.

Second, even with CPF and insurance nominations in place, all your other assets are still in limbo. If you die without a will, they’re distributed by the law rather than by you. So consider writing a will to cover everything else, and for larger or more complex estates, setting up a trust.

Put together, these three tools (a CPF nomination, insurance policy nominations, and a will) each reach assets the others can’t, so your wishes, rather than a default formula, decide where everything goes.

If you’d like a hand putting all three in place, that’s exactly what our FullCircle financial planning session is for.

BEFORE YOU GO

Everything on this site is written for everyone. But your financial goals, your responsibilities, and what you already have in place are yours alone.

FullCircle is our comprehensive financial planning session. You'll walk away with a clearer picture of where you stand and what to prioritise, across protection, retirement, and estate planning.