Do you fall within the majority of Singaporeans who are invested? Which instruments have you chosen to invest in?

Bonds are one of the most popular forms of investments in Singapore. This is because they generally pose lower risk than stocks and equities.

Even within this category, there are many different types of bonds, with Singapore Government Securities (SGS) being possibly the most secure.

In this article, we’ll cover the different types of SGS and more.

So, read on!

What are Singapore Government Securities (SGS)?

Singapore Government Securities are basically government bonds issued by the Monetary Authority of Singapore (MAS). They are debt instruments which typically give fixed interest rates to the investors “loaning” their funds to the government. Although they do not give high returns, they have extremely high credit ratings since they are backed by the government.

Furthermore, the Singapore government has a balanced budget policy and often enjoys a surplus. This means that they do not actually require these funds for its expenditure. Instead, the primary purpose of issuing these bonds is to grow the debt market and to offer investors a safe form of investment with long-term returns.

There are 4 main types of SGS, namely the Singapore Savings Bond (SSB), Singapore Government Securities (SGS) Bond, Treasury Bills (T-Bills), and Special Singapore Government Securities (SSGS). The most commonly known type of SGS is the SSB, while the T-bills are least common. The SSGS Bond is not typically relevant for individual investors, however they have been included in this article for interest and educational purposes.

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

How Do the 4 Types of Singapore Government Securities (SGS) Work?

1) Singapore Savings Bonds (SSB)

Singapore Savings Bonds (SSBs) were introduced on 1 October 2015 as a form of non-marketable SGS for retail investors. The primary objective of SSBs is to provide retail investors with a secure long-term investment option. These savings and investment funds could then be channelled towards their long-term financial goals, such as retirement. SSBs are issued by the MAS for the Singapore government.

SSBs are secure as both the principal and interest payments are guaranteed by MAS. In alignment with the aim of protecting individuals from capital losses, SSBs are also non-tradable securities. This means that SSBs are directly issued by the MAS and there is no secondary market.

SSBs have a tenor of 10 years, with an interest rate that increases over time. This is meant to encourage longer-term investments. However, SSBs are also fully liquid, allowing retail investors to exit anytime before the bond matures, with no penalties.

But is it worth it investing into SSBs? What are the historical yields?

The average return depends on the amount of time you stay invested. It also be noted that the interest rates do differ slightly depending on which month’s bond you buy into. An investor can expect about 1.64% (Feb 2022’s issue) of returns per year if they hold the SSB until maturity.

If you are interested in buying SSBs, you can do so as long as you are 18 years old and above, have a CDP account, and a bank account in one of the three local banks – POSB/DBS, OCBC, or UOB. If you are already in the Supplementary Retirement Scheme (SRS), you may also use these funds to invest in SSBs. The minimum amount for investment is $500.

2) Singapore Government Securities (SGS) Bonds

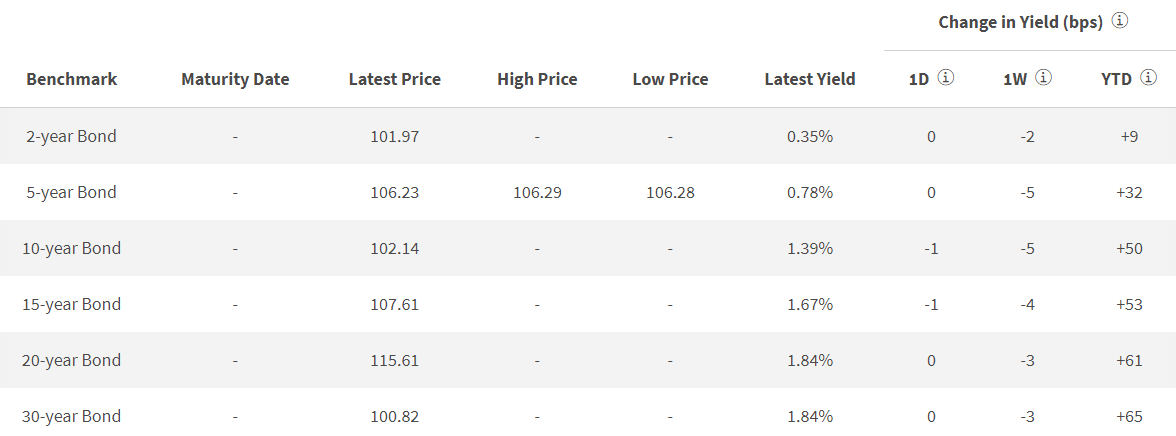

SGS bonds are longer-term bonds which mature in either 2, 5, 10, 15, 20, or 30 years. They pay a fixed interest rate every 6 months. This is also called a semi-annual coupon. Similarly to SSBs, SGS bonds are meant to be a safe, long-term investment product. However, it is less flexible compared to SSBs as investors are not allowed to redeem their funds early. Instead, investors who wish to exit may sell their SGS bonds in the secondary market.

The typical yield for SGS bonds varies depending on the length to maturity.

To invest in SGS bonds, you are required to be above 18 years old. You will also have to invest a minimum of $1,000, and in multiples of $1,000. SGS bonds are issued through uniform-price auctions, which are held according to the annual issuance calendar. Both competitive and non-competitive bids are accepted.

You may choose to invest using cash or funds from the Central Provident Fund Investment Scheme (CPFIS) or Supplementary Retirement Scheme (SRS).

3) Treasury Bills (T-bills)

T-bills are shorter-term bonds that mature in either 6 months or 1 year. They are issued at a discount to their face value, and can be redeemed at face value upon maturity. Once again, T-bills are meant to be secure investments.

The historical yield for T-bills are 0.54% for 6-month T-bills and 0.54% for 1-year bills. These are comparable to the other SGS bonds given the length of investment time.

T-bills are issued fortnightly or quarterly by MAS via uniform-price auction, similar to SGS bonds. You can check the issuance calendar for more information on when T-bills are issued.

The minimum amount for investment is $1,000, and in multiples of $1,000. You can invest using cash, SRS or CPF.

4) Special Singapore Government Securities (SSGS)

While SSGS bonds are not available for individual retail investors, it may be of interest to note what they are and how they work.

SSGS bonds are non-tradable bonds issued by the government to meet the investment needs of the CPF Board. They are funded by CPF monies, which are then typically entrusted to the MAS and GIC.

Under the Government Securities Act established in 1992, proceeds from SSGS and other SGS funds cannot be used for the Singapore government’s expenditures. Instead, those funds, along with government surpluses, are invested safely by MAS and GIC. Specifically, the funds are deposited and converted by MAS into long-term foreign assets through the foreign exchange market (FOREX). These investments are transferred to GIC for long-term management.

This enables the CPF Board to focus on its primary function as a national social security institution, while having the funds managed well and able to offer fair returns.

SSB vs. SGS Bonds vs. T-bills: 9 Key Differences

To sum up, these are the key factors for comparison against the three different types of SGS – SSBs, SGS bonds, and T-bills.

| Singapore Savings Bonds (SSB) | Singapore Government Securities (SGS) Bonds | Treasury Bills (T-bills) | ||

| 1 | Tenor | 10 years | 2, 5, 10, 15, 20 or 30 years | 6 months or 1 year |

| 2 | Method of issuance | Quantity ceiling | Uniform price auction | Uniform price auction |

| 3 | Secondary market | No | Yes Via local banks or SGX | Yes Via local banks |

| 4 | Minimum investment amount | $500, and in multiples of $500 | $1000, and in multiples of $1000 | $1000, and in multiples of $1000 |

| 5 | Maximum investment amount | $200,000 | None | None |

| 6 | Ability to invest using CPF and SRS funds | Yes for SRS, no for CPF | Yes for both | Yes for both |

| 7 | Average annual yield | 1.39% over 10 years (0.35% in year 1 to 2.55% in year 10) | 1.39% for 10 year bond | 0.35% for 1 year |

| 8 | Frequency of interest payments | Every 6 months | Every 6 months | At maturity |

| 9 | Flexibility for early redemption | Flexible and can be redeemed in any given month with no penalty | Not flexible | Not flexible |

7 Pros and Cons of SGS (In General)

As in all forms of investment, there are pros and cons to choosing SGS. Being aware of these advantages and disadvantages will allow you to make a more informed decision.

Pros

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

1) Backed by the Government (With AAA Credit Rating)

The Singapore government has a strong AAA credit rating. This makes its guarantees of principal and returns highly reliable, thus making the SGS bonds safe forms of investment.

2) Receive Regular Interest

Both the SSB and SGS, which are longer-term bonds, provide regular interest payments every 6 months. The T-bill is an exception, although this is because it is a shorter-term bond that matures within either 6 months or 1 year. This means that retail investors can enjoy regular interest payouts even while saving for the long-term future.

3) Low Minimum Investment to Get Started

There are extremely low barriers to entry to start investing in SSB, SGS and T-bills. The minimum investment amounts range from $500 to $1,000, which most Singaporean adults will be able to afford.

4) Multiple Ways to Invest

Furthermore, Singaporeans do not have to invest solely using cash. You can also use funds from your CPF or SRS to invest in these securities. This makes it easier for you to invest, without impacting your cash flow. It is also a great way to make use of the funds you have already amassed under those schemes to gain more returns.

Cons

5) There Are Limits

There are limitations to how much you can invest in the SSB in particular, which is capped at $200,000. This is important because it limits the amount of absolute returns that can be earned overall.

6) Potential Illiquidity

Apart from the SSB, SGS bonds and T-bills are relatively illiquid. If you exit the investment early by selling them in the secondary market, there is a possibility you might not make a profit.

7) Relatively Low Interest

This is potentially the largest disadvantage of investing in the SGS. The interest rates for all SGS are relatively low, especially when compared to the average annual inflation rate which has been estimated at 1.52% over the past 30 years. This means that the returns from SGS bonds will barely cover, or may even be less than, the loss in money value due to inflation. For this reason, many retail investors choose to diversify into other investments such as stocks and equities, which carry higher risk but also potentially higher returns.

Conclusion

SGS can be a great way to diversify your investment portfolio and safeguard your wealth. The SSB, SGS bonds, and T-bills are good instruments that can be used to save up for long-term financial goals. However, it would be wise to also invest in other instruments such as stocks, equities, and ETFs if you are looking to grow your wealth over time.

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.