Buying a property in Singapore is a costly affair.

It could also be one of the biggest financial undertakings you could take on in your life.

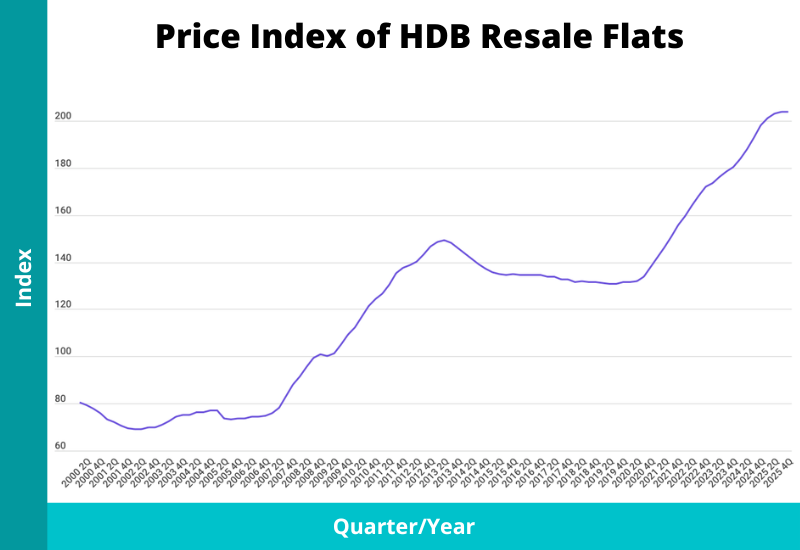

Residential property prices have increased significantly over the years. This can be seen with million-dollar HDB resale flats becoming more common. Even the median price of a 5-room HDB resale flat is at $736,000 now.

But the purchase price of the property is just one half of the equation. There are other costs associated with purchasing and owning a home in Singapore, and that will be the topic for today.

So, read on!

The Average Purchase Prices of Properties in Singapore

Before diving into other fees and charges, let’s quickly go over the current costs of various property types in Singapore. These costs will form a significant portion of the financial resources you’ll need to commit to.

HDB resale flat prices have increased by 51.0% over the past 10 years.

During the same period, prices of private residential properties have risen by 52.8%.

Here are the median prices of both HDB resale flats and private residential properties:

| Housing Type | Average Price | Median Price | Average Price/Sq. Foot | Average Size (Sq. Foot) | Average Price/Sq. Metre | Average Size (Sq. Metre) |

|---|---|---|---|---|---|---|

| HDB Flats | $652,498 | $628,000 | $638.80 | 1,021.38 | $6,876 | 94.89 |

| Condo | $2,128,942 | $1,875,000 | $2,123.95 | 1,002.22 | $22,862 | 93.11 |

| Landed | $5,928,412 | $4,650,000 | $1,815.79 | 3,264.93 | $19,545 | 303.32 |

Will these prices cool down over the next few years? Nobody really knows. However, the government has introduced cooling measures in recent years to address this issue.

Keep in mind, these prices don’t include the additional upfront and recurrent costs that come with owning a home. We’ll touch on those next.

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

The Upfront Costs of Purchasing a Home in Singapore

When buying a home in Singapore, there are several typical fees and charges you’ll encounter, whether you’re purchasing a BTO, resale flat, or private property. Let’s break down the main expenses.

Application Fee

For BTO flats, there is an administration fee of $10 for every application you submit. This fee is relatively small.

When it comes to HDB resale flats, the fees vary depending on the size of the flat. Here are the resale application fees:

- 1- and 2-room flats: $40

- 3-room and bigger flats: $80

Option Fee

An Option to Purchase (OTP) is a legal contract between the buyer and seller of a property. This contract ensures that the seller agrees to sell the property at a specific price within a designated period.

How does it work?

By paying the option fee, the buyer effectively “reserves” the property. During this reservation period, the seller cannot sell the property to anyone else. This arrangement provides the buyer with exclusive rights to purchase the property while offering some protection to the seller. If the buyer backs out of the deal, the option fee is forfeited, compensating the seller for the lost opportunity to sell to others.

Once the option fee is paid, the buyer has a set period to exercise the OTP or finalise the purchase. This window allows the buyer to further inspect the property, secure financing, and address any other necessary details. If the buyer decides to proceed with the purchase, they will then need to pay an option exercise fee. These fees are typically paid in cash and form part of the downpayment required for the property.

The amount required varies depending on whether you’re buying an HDB BTO, resale flat, or a private property.

Below is an overview of the option fees for different types of HDB BTO flats:

| Flat Type | Option Fee |

| 4-room and bigger | $2,000 |

| 3-room | $1,000 |

| 2-room Flexi | $500 |

For HDB resale flats, these are the typical option fees. The buyer has 21 days to exercise the OTP.

| Payment | Amount to Pay |

| Option Fee | $1 to $1,000 |

| Option Exercise Fee | An amount, which when including the Option Fee, does not exceed $5,000 |

As for private properties, the option fee is typically 1%, with an additional 4-9% required to exercise it. The buyer has 14 days to exercise the OTP. These terms are still negotiable.

Downpayment

The downpayment is the difference between the purchase price of the property and the loan amount you’re granted, minus any option fees you’ve already paid.

There will always be a minimum downpayment you need to make because you cannot take a loan that covers 100% of the property’s price.

The percentage of the downpayment required depends on whether you are taking an HDB loan or a bank loan.

Let’s break down the scenarios, assuming you’re buying your first property with no existing property or mortgage loans and are able to secure a healthy loan amount.

HDB Loans:

- You must pay 25% of the purchase price as the downpayment. This is split into 10% at the signing of the agreement of lease and the remaining 15% at key collection.

- The downpayment can be made using cash and/or CPF OA savings.

- Staggered and deferred payment schemes are available for eligible buyers, providing some flexibility in managing the downpayment.

Bank Loans:

- You need to pay 25% of the purchase price as the downpayment, with at least 5% of this amount in cash.

- The remaining 20% can be paid using cash or CPF OA savings.

- Private properties and Executive Condominiums (ECs) must be purchased using bank loans

Stamp Duty

You are required to pay stamp duties, which are essentially taxes on the transaction. There are two main types of stamp duties: Buyer’s Stamp Duty (BSD) and Additional Buyer’s Stamp Duty (ABSD).

Buyer’s Stamp Duty (BSD)

BSD is a mandatory tax that all buyers must pay, regardless of whether they are Singapore citizens, permanent residents (PRs), or foreigners. The amount is calculated based on the purchase price or market value of the property, whichever is higher.

| Purchase price or market value of the property | BSD rates for residential properties |

| First $180,000 | 1% |

| Next $180,000 | 2% |

| Next $640,000 | 3% |

| Next $500,000 | 4% |

| Next $1,500,000 | 5% |

| Remaining amount | 6% |

Additional Buyer’s Stamp Duty (ABSD)

ABSD is an additional tax that may apply depending on the buyer’s residency status and the number of properties they own.

Here are a few scenarios where ABSD becomes applicable:

- If you are a Singapore citizen purchasing a second or subsequent property

- If you are a permanent resident

- If you are a foreigner

For most Singapore citizens purchasing their first home, only BSD is applicable. This means they will not have to pay ABSD unless they are buying additional properties.

Here are the ABSD rates:

| Profile of Buyer | ABSD Rates on or after 27 Apr 2023 |

| Singapore Citizens (SC) buying first residential property | Not applicable |

| SC buying second residential property | 20% |

| SC buying third and subsequent residential property | 30% |

| Singapore Permanent Residents (SPR) buying first residential property | 5% |

| SPR buying second residential property | 30% |

| SPR buying third and subsequent residential property | 35% |

| Foreigners (FR) buying any residential property | 60% |

| Entities buying any residential property | 65% |

| Housing Developers buying any residential property | 35% (Plus Additional 5% (non-remittable)) |

The ABSD rates have been updated as of 27 April 2023, following the introduction of cooling measures aimed at stabilising the property market, particularly in response to foreign investment in Singapore properties.

An interesting note is that US citizens enjoy the same stamp duty treatment as Singapore citizens. This means that they can purchase their first property in Singapore by only paying BSD, without the additional burden of ABSD. This presents a unique opportunity for US citizens who believe in the potential of the Singapore property market.

Agent Commissions

You might need to pay a fee to property agents who assist you in finding a home, conducting viewings, and navigating the buying process. These fees can vary based on the type of property and the services provided by the agent.

For HDB resale flats, the agent commission is typically 1% of the purchase price. This fee covers the agent’s efforts in marketing the property, arranging viewings, and handling the necessary paperwork.

However, as of 13 May 2024, HDB owners have the option to list and market their homes without an agent using HDB’s new Resale Flat Listing (RFL) platform. This platform allows prospective buyers to browse listings on their own and facilitates transactions between buyers and sellers, with or without the use of agents.

For private properties, the commission structure differs. Typically, buyers are not charged a commission. Instead, the agent’s fee is shared between the seller’s and buyer’s agents.

Note that there are no fixed rules or structures for agent fees in Singapore. While there is a market rate, these fees are negotiable and can vary depending on various factors. For instance, if more marketing is involved, there is an urgency to sell, or if the buyer is overseas and requires more handling, the fees might be higher.

Property Valuation Fee

Before granting a loan, both HDB and financial institutions need to know the value of the property you’re intending to buy. This ensures that the loan amount corresponds accurately to the property’s worth, preventing the risk of granting a high loan for a property that isn’t worth as much, which could have potential financial negative impacts.

For HDB resale flats, you can submit a request for value with a fee of $120.

For private properties, the cost of a valuation can range between $200 to $500. However, this fee might be included as part of a loan package offered by some financial institutions.

Legal, Conveyancing, and Other Fees

There are several legal and miscellaneous fees involved in the buying process.

These fees are typically for the registration and transfer of land titles and deeds. Ensuring these documents are accurately processed requires the assistance of a lawyer.

For HDB transactions, the process has been simplified. HDB provides a calculator that allows you to estimate the legal fees you will incur. Additionally, HDB offers legal services, which are convenient and cost-effective.

Here are some of the fees that apply to BTO applicants:

| Legal fees | First $30,000: $0.90 per $1,000 Next $30,000: $0.72 per $1,000 Remaining Amount: $0.60 per $1,000 |

| Survey Fee | $163.5 to $408.75 (depending on flat size) |

| Stamp duty on deed of assignment | 0.4% of loan amount, capped at $500 |

| Lease in-escrow registration fee | $38.30 |

| Mortgage in-escrow registration fee | $38.30 |

Similarly, banks have their preferred law firms that handle the legal aspects of property transactions. These firms are familiar with the bank’s processes and can often expedite the paperwork, making the transaction smoother for the buyer. Using the bank’s recommended legal services can also be more economical, as these firms usually offer competitive rates negotiated by the banks.

While you have the option to source your own lawyer, most people prefer to stick with the legal services provided by HDB or the banks. This choice often boils down to convenience and cost savings.

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

Renovation, Moving, and Furnishings

Are you looking to flip the property quickly for a profit, or are you intending to settle in for the long haul?

If you’re planning a quick flip, it makes sense to be more conservative with your renovation budget. Focus on essential updates that increase the property’s appeal without overspending.

In contrast, if you’re planning to live in the property for many years, it may be worth investing more to make the home aesthetically pleasing and comfortable. This might involve higher-quality finishes, custom furnishings, and advanced electronics and appliances.

The main costs you’ll encounter include renovation, furnishings, electronics, and appliances. These costs can vary widely depending on your choices and the scope of the work. For instance, basic renovations and furnishings can be as low as $10,000, while extensive and high-end projects can exceed $100,000. On average, many homeowners spend around $50,000.

You can also consider financing options if you prefer not to use your existing cash. There is a maximum loan amount you can take for renovations, so you’ll need to plan accordingly.

The Recurring Costs of Owning a Home in Singapore

Here are some of the running costs of owning a home.

Mortgage Insurance

A mortgage insurance policy is essentially a life insurance policy that pays out a lump sum, at least enough to cover your loan liability, in the event of death or total and permanent disability.

Typically, you pay an annual premium for this coverage. The cost of this premium depends on factors such as your age, the coverage amount, the type of coverage, and the length of the coverage.

Given the size of most property loans, having mortgage insurance is recommended. Imagine if something unfortunate happens to you, would your spouse be able to keep up with the mortgage payments? Without the financial means, they might be forced to sell the house. Mortgage insurance can help prevent such a scenario.

For HDB owners paying their mortgages with CPF OA savings, there’s a specific requirement to be insured under the Home Protection Scheme (HPS), which is administered by the CPF Board. So, how much does this protection cost? For a 30-year-old male covering 100% of a 25-year loan of $500,000, it costs $350 per year.

However, if you already have your own life insurance policy, whether term or whole life, you could opt out of the HPS if you meet certain conditions. It’s about finding what works best for you and ensuring you’re not over-insured.

Another option to consider is level term insurance. This type of insurance can combine both income replacement needs and mortgage liabilities. It’s a way to cover all bases with one policy, simplifying your financial planning.

Home and Fire Insurance

Fire insurance is mandatory for anyone with an outstanding HDB loan. This insurance is designed to cover internal structures, fixtures, and areas built and provided by HDB. It’s a basic form of protection to ensure that essential elements of your home are safeguarded.

Administered by Etiqa since August 2024, HDB fire insurance is very affordable. Premiums range from $1.11 to $6.68 for five years of coverage, depending on your flat type.

However, it is important to note that this insurance only provides the basics.

For more comprehensive protection, consider adding home insurance or home contents insurance. These policies can extend your coverage to include personal belongings, renovation work, and even liability for any damages you might accidentally cause to your neighbours’ property.

Home insurance can cost less than $50 a year. The price will vary based on home size, coverage amount and the comprehensiveness of benefits.

Utilities (electricity, gas, and water)

Electricity, gas, and water are basic necessities in any household.

Among these utilities, electricity takes the largest share of the bill. This is especially true in places like Singapore, where the hot and humid weather drives up the use of air conditioning. Additionally, with more people working from home now, the demand for electricity has surged.

How much are we talking about?

On average, the monthly electricity bill for a 4-room HDB flat in Singapore is $118.38. This is slightly below the national average of $133.32.

Property Tax

You are required to pay an annual property tax. This tax is a percentage of your property’s annual value (AV) and varies depending on whether you live in the property or rent it out.

According to IRAS, the AV is defined as “the estimated gross annual rent of the property if it were to be rented out, excluding furniture, furnishings, and maintenance fees.”

This means that the AV represents what you might earn if you rented out your property, minus the costs of keeping it furnished and maintained.

To give you an idea, here are the median annual values for HDBs and private properties:

| Type of Housing | Median Annual Values |

| 1 or 2 Room HDB Flats | $6,540 |

| 3 Room HDB Flats | $9,900 |

| 4 Room HDB Flats | $12,480 |

| 5 Room HDB Flats | $13,500 |

| Executive & Others HDB Flats | $14,220 |

| Non-landed (includes Executive Condominiums) | $27,000 |

| Landed | $39,600 |

If you’re curious about your own property tax, you can use the calculator on the IRAS website to get an estimate.

High property taxes can be a significant burden, especially for owner-occupied residences with an AV of more than $30,000 and for non-owner-occupied residential properties. This can put more strain on those buying residential properties for investment purposes, as higher taxes can affect the overall yields from such investments.

Mortgage Repayments/Home Loan Interest

If you’ve taken a home loan, which most of us do, your mortgage repayments will include both interest and principal. Currently, the HDB mortgage interest rate is 2.6%. In contrast, banks typically offer fixed rates for the first few years, which then switch to floating rates.

A significant portion of your mortgage payments goes towards interest, especially in the early years of the loan. Even with mortgage rates well off their 2023 and 2024 peaks, the interest paid over a full loan tenure adds up to a substantial sum.

To manage this, consider refinancing your loan or paying it off quickly. Refinancing can help you secure a lower interest rate, reducing the amount you pay over the loan’s lifetime. Alternatively, paying off your loan faster reduces the total interest paid.

If paying off your loan quickly isn’t an option, you might consider using your excess cash to invest. This way, you can potentially earn higher returns, putting your money to better use. Of course, this strategy depends on your risk appetite. Investing always comes with risks, and it’s important to assess whether you are comfortable with the potential ups and downs of the market.

Maintenance Fees

Maintenance fees apply to both HDB flats and private condominiums. These fees are collected to fund essential services, such as maintenance and repairs, cleaning, fumigation, and landscaping.

In the context of HDB flats, these fees are known as service and conservancy charges. They can vary depending on the estate, the type of flat, and whether you are a Singapore citizen.

For instance, a 4-room HDB flat under Nee Soon Town Council has a monthly fee of $70.60 (reduced rate).

For private condominiums, maintenance fees cover the general upkeep of the surroundings as well as amenities like gyms and swimming pools. These fees are significantly higher, averaging around $300 per month, and can be even higher for luxury developments. This higher cost can diminish the yield if you’re buying properties for investment purposes.

Final Thoughts

Housing in Singapore is expensive, especially for foreigners. Singaporeans do have some assistance, such as housing grants and the ability to use CPF OA savings. However, even with this help, the cost can still be high. The trend shows median prices of residential properties continuing to rise.

You might not want to overstretch yourself by buying a huge home and taking on a larger loan. This is particularly true given the high interest rates in recent years.

As your home becomes a significant financial resource, or even a liability, consider having life insurance (term insurance or whole life insurance) if you haven’t already. Life insurance can provide a safety net, ensuring that your home is protected even if something unexpected happens. This step can offer peace of mind and financial security for you and your loved ones.

Finally, the purchase is only the start. Our guide on how your home fits into your wider financial plan covers what comes after, from financing and protection through to retirement and inheritance.

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.