Singapore’s property market is known for its high prices. The main reason for this is simple: demand outweighs supply.

Given that Singapore is a small nation with limited land, the supply of property is constrained. As long as demand persists, prices are bound to rise, making it increasingly important to explore more affordable financing and housing-related solutions.

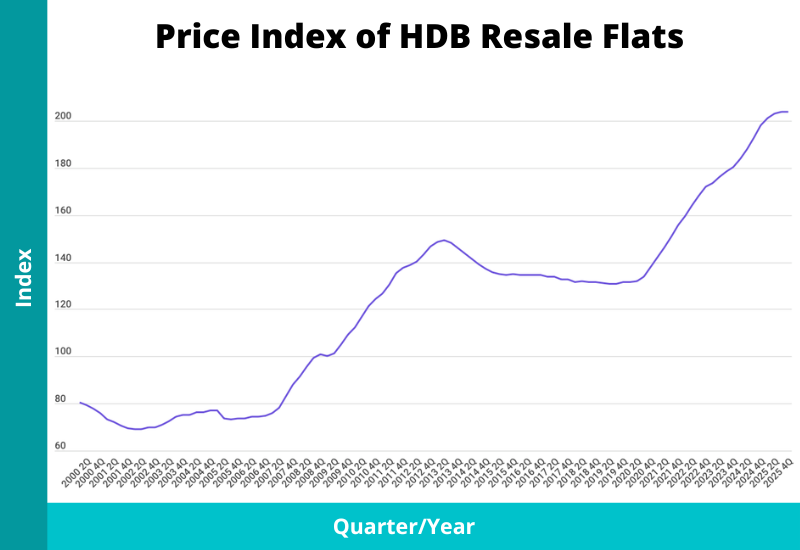

Looking at the long term trend, this pattern shows no signs of slowing down.

But what drives such appeal for residential properties in Singapore? Let’s delve into some of the main reasons behind the demand for properties in Singapore.

- How Much Do Properties in Singapore Cost?

- 1) Land Scarcity

- 2) High Population Density

- 3) Strong Financial Ability of Its Population

- 4) External Demand From Foreigners

- 5) Long Waiting Times for Subsidised Public Housing

- 6) More Choose to be Single

- 7) Low Interest Rates

- 8) Higher Construction Costs

- Final Thoughts

How Much Do Properties in Singapore Cost?

Singapore is often recognised as one of the most expensive cities in the world, particularly for foreigners.

The cost of living has been steadily rising, and recent years have seen a surge in inflation.

This trend is mirrored in the property market, where prices have increased significantly. For instance, the prices of HDB resale flats have risen by 51% over the last 10 years, while private property prices have seen a similar increase of 52.8%.

As a result, Singapore is now one of the most expensive cities in which to own property, with correspondingly high rental prices.

The median prices for both public and private housing reflect this reality. Whether you’re looking at public housing, like HDB flats, or private condos and landed properties, the cost of owning or renting a home in Singapore is steep.

| Housing Type | Average Price | Median Price | Average Price/Sq. Foot | Average Size (Sq. Foot) | Average Price/Sq. Metre | Average Size (Sq. Metre) |

|---|---|---|---|---|---|---|

| HDB Flats | $652,498 | $628,000 | $638.80 | 1,021.38 | $6,876 | 94.89 |

| Condo | $2,128,942 | $1,875,000 | $2,123.95 | 1,002.22 | $22,862 | 93.11 |

| Landed | $5,928,412 | $4,650,000 | $1,815.79 | 3,264.93 | $19,545 | 303.32 |

SIDE NOTE

A policy bought years ago. Savings in three places. A will that's still on the to-do list.

None of it is wrong. It's just not a plan yet.

There's an order that turns the pieces into one system, and it doesn't require becoming a finance expert. Here's the order, in 7 steps, so you know what to sort out first.

1) Land Scarcity

Singapore is a small city-state, measuring just 27 km from north to south and 50 km from east to west.

This limited space means that land is a scarce resource. When supply is constrained by physical boundaries, as it is in Singapore, demand inevitably pushes prices up. Solving this issue would be a major step towards addressing the challenge of unaffordable housing.

Over the years, Singapore has undertaken land reclamation projects to increase its usable area. While these efforts have added some space, there are limits to how much land can be reclaimed. Despite ongoing projects, the fundamental issue of scarcity remains.

2) High Population Density

Singapore’s total fertility rate has been on a downward trend, reaching an all-time low of 0.87 in 2025.

Despite this decline, the total resident population, which includes citizens and permanent residents, has continued to grow.

This growth can be partly attributed to Singapore’s efforts to attract multinational corporations and businesses with various incentives, such as low corporate taxes and a favourable business environment. These advantages also draw expatriates to live and work in Singapore.

As a result, even with a declining birth rate, the population density in Singapore has been increasing.

With a limited land area and more people choosing to reside here, property prices naturally rise.

3) Strong Financial Ability of Its Population

Singapore’s lack of natural resources and limited land led the nation to invest heavily in human capital from its early years. This investment resulted in a strong emphasis on education, which has paid off significantly over time.

Today, Singaporeans are among the most educated populations globally, often securing high-income jobs that contribute to the country’s high GDP.

In 2025, the median income, inclusive of CPF contributions, stands at $5,775 per month.

Furthermore, many households in Singapore are dual-income, have small family sizes, and may have received assistance from asset-rich parents. This combination provides many Singaporeans with substantial disposable income and savings.

Additionally, the ability to use CPF Ordinary Account (OA) savings, a form of compulsory savings, enhances the financial capability of Singaporeans. It enables a significant portion of the population to afford and sustain higher housing prices.

Being able to afford the purchase is one thing. Sustaining it alongside your other financial goals is another, and that comes down to how you plan around your property.

4) External Demand From Foreigners

If Singaporeans find local property attractive, it’s no surprise that foreigners do too.

Singapore offers a range of appealing features: it is safe from natural disasters, boasts a very low crime rate, and enjoys political stability. The country is also renowned for its cleanliness and green spaces, making it an attractive place to live, especially for the wealthy.

Whether during their working years or in retirement, many find Singapore an ideal place to reside.

For those not looking to live here, investing in Singaporean property is seen as a secure and potentially lucrative option. The risk of downsides is relatively low, while the potential for capital appreciation is high.

Foreigners are allowed to buy private properties in Singapore, the same ones locals can purchase. Celebrities like Chow Yun-Fat and Jackie Chan are known to own properties here.

Historically, there was an Additional Buyer’s Stamp Duty (ABSD) of 30% for foreigners, a manageable sum for wealthy investors, which contributed to steady foreign demand.

However, as property prices soared, the government implemented cooling measures, raising the ABSD to 60%.

Despite this, citizens of countries with free trade agreements with Singapore, such as the United States, Iceland, Liechtenstein, Norway, and Switzerland, are treated the same as Singaporeans regarding ABSD. This exemption presents a unique investment opportunity for those looking to enter the Singaporean property market without the heavy tax burden.

QUICK CHECK

Can you answer these three questions?

1) If something happened to you tomorrow, how much would your family receive?

2) At 65, what monthly income will your savings and investments pay you?

3) If you never get round to a will, who inherits what, and in what proportion?

Most people manage one at best. Not because they're careless, but because nobody has shown them which order to tackle things in.

That order exists. Work through your finances in this sequence, from income and protection through to investments and estate planning.

5) Long Waiting Times for Subsidised Public Housing

77.2% of Singapore residents live in public housing, known as HDB flats, while the rest live in private properties.

The Housing and Development Board (HDB) offers a Build-To-Order (BTO) scheme, where eligible buyers such as married couples can purchase new HDB flats at a more affordable price. However, these flats come with a significant waiting period, typically three to four years.

The COVID-19 pandemic extended waiting times. As a result, married couples who cannot wait for a new flat often turn to the resale market, where prices are generally higher.

The supply picture is now shifting. An estimated 13,480 flats will reach their Minimum Occupation Period in 2026, nearly double the 6,973 in 2025, and analysts expect this to moderate resale price growth. HDB has also been ramping up BTO launches, including Shorter Waiting Time flats that are ready in around three years or less. Even so, buyers who cannot wait continue to turn to the resale market and pay a premium for it.

6) More Choose to be Single

Household dynamics in Singapore are changing, with more individuals choosing to remain single.

| Proportion of Total Households in 2025 | Proportion of Total Households in 2015 | Difference in Proportion | |

|---|---|---|---|

| Married Couple-Based With Children | 47.6% | 56.5% | -8.9% |

| Married Couple-Based Without Children | 19.1% | 15.5% | 3.6% |

| Lone Parent | 6.8% | 9.7% | -2.9% |

| Living Alone | 16.7% | 11.9% | 4.8% |

| Others | 9.8% | 6.3% | 3.5% |

Why does this matter?

It has a significant impact on the housing market. For instance, if ten people marry each other, they would collectively seek to buy five homes, typically. However, if all ten choose to stay single, they would potentially look to purchase ten homes.

This shift increases the number of households and, consequently, the demand for housing. As more people opt to live independently, the demand for housing units rises, potentially driving up property prices even further.

This trend, if it becomes more pronounced, could put additional pressure on an already competitive housing market.

7) Low Interest Rates

Singapore has benefited from relatively low mortgage interest rates over the years. This trend was especially pronounced during the pandemic when interest rates hit their lowest levels.

Cheaper borrowing costs made it easier for people to afford homes, which in turn spurred demand for properties.

Rates did climb sharply in 2022 and 2023 on the back of rate hikes in the United States, which raised the cost of servicing a home loan. But that spike has since unwound. The 3-month SORA, which most floating home loans are pegged to, fell to a three-year low of around 1.2% by early 2026, and fixed-rate packages are now roughly half of what they were at the start of 2025.

With borrowing this affordable again, financing costs are once more supporting demand for property rather than holding it back.

8) Higher Construction Costs

The pandemic and recent wars have triggered global inflation and supply chain shortages, affecting many industries.

In Singapore’s construction market, these challenges have led to a shortage of skilled labour, which, in turn, has increased overall construction costs and caused delays in project completions.

The prices of raw materials have also risen, contributing to the higher costs.

Additionally, anything related to housing, such as renovations and furnishings, has become more expensive. These factors drive up the cost of housing in Singapore, making it more challenging for buyers and developers alike.

Final Thoughts

It’s reassuring to know that the government can control property prices through cooling measures, such as increasing the Additional Buyer’s Stamp Duty (ABSD) and tightening loan limits.

These measures aim to prevent property prices from rising unsustainably and becoming unaffordable for the average Singaporean.

While properties may still appear expensive, many locals are well-equipped to purchase homes.

Housing grants are available to assist buyers, and a significant portion of the population lives in HDB flats or BTO units, which are subsidised.

Lower-income families, in particular, receive additional subsidies to help them afford housing, ensuring that homeownership remains accessible across different income levels.

BEFORE YOU GO

Articles can tell you what generally makes sense. They can't see your policies, your CPF, or your plans.

FullCircle is our comprehensive financial planning session. A licensed consultant goes through what you have, shows you the gaps and overlaps, and tells you what to prioritise across protection, retirement, and estate planning.

It's complimentary, takes about 45 minutes, and if nothing needs changing, we'll say so.