Healthcare costs in Singapore are undeniably high, and they are only getting higher. With rising costs come rising premiums, tighter insurance terms, and greater financial pressure on households when something goes wrong.

But just how expensive is a hospital stay today, and are you prepared for it?

This article breaks down what a hospital bill in Singapore actually looks like, with real procedure examples, and what you can do to protect yourself financially.

Read on.

Summary of Key Findings

- There is no single “average” hospital bill: costs vary enormously depending on the procedure, the ward class, and whether you go to a public or private hospital

- The same procedure can cost up to six times more at a private hospital than at a subsidised public ward

- A knee replacement, for example, costs a median of $6,993 in a public C ward but $48,746 at a private hospital

- Late-stage cancer treatment can cost $100,000 to $200,000 per year

- MediShield Life premiums are rising by up to 35% over three years, from 2025 to 2028

- From April 2026, Integrated Shield Plan rider rules have changed: deductibles are no longer fully coverable, and the annual co-payment cap has doubled from $3,000 to $6,000

SIDE NOTE

Most people's finances aren't a plan. They're a collection of separate decisions: a policy bought years ago, investments that don't talk to each other, a will that's still on the to-do list.

If that sounds familiar, there's a fix that doesn't require becoming a finance expert.

Here's the 7-step framework we use to organise everything into one system.

Quick Overview: Healthcare in Singapore

Singaporeans are living longer. Life expectancy currently stands at 83 years, one of the highest in the world, and it is expected to rise further in the coming decades.

That is broadly good news. The less welcome side of it is that more Singaporeans are spending longer periods in ill health. Cancer cases are rising, and chronic conditions such as diabetes are becoming more prevalent. As the population ages, demand on the healthcare system grows, and costs rise with it.

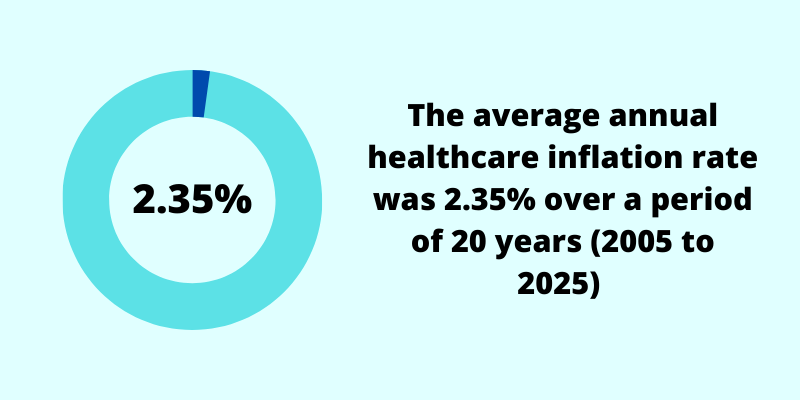

The average healthcare inflation rate over the past 20 years was 2.35% per year based on consumer prices, but insurers are experiencing far steeper increases.

According to WTW’s 2026 Global Medical Trends Survey, medical costs as reported by insurers rose by 15.5% in 2025 and are projected to reach 16.9% in 2026.

The question worth asking is whether your financial resources can withstand a large, unexpected medical bill. This article helps you understand what that bill might actually look like.

The Top 10 Causes of Hospital Admissions

A hospital stay can be triggered by almost anything. Whether it is an accident, a sudden illness, or the onset of a chronic condition, the hospital is typically the first port of call.

Here are the top 10 reasons for hospitalisation in Singapore based on the latest published data:

| Reason | % of Total Discharges |

|---|---|

| Accident, poisoning and violence | 8.8 |

| Cancer | 5.1 |

| Pneumonia | 4.6 |

| Ischaemic heart diseases | 2.9 |

| Intestinal infectious diseases | 2.6 |

| Other heart diseases | 2.6 |

| Infections of the skin and subcutaneous tissue | 2.5 |

| Cerebrovascular diseases (including stroke) | 2.1 |

| Disorder of gallbladder, biliary tract and pancreas | 1.8 |

| Diabetes mellitus | 1.7 |

These top 10 reasons account for just 34.7% of all hospital admissions. The remaining 65.3% covers a wide range of other conditions, which underscores how unpredictable hospitalisation can be. You may plan for the obvious risks and still be caught out by something entirely unexpected.

That unpredictability is precisely why understanding the cost of a hospital stay matters.

The Different Types of Costs in a Hospital

Whether you end up at a public or private hospital will have a significant bearing on what you pay. Within public hospitals, the ward class you choose matters too: the more beds in a ward, the greater the government subsidy, and the lower your bill.

That said, both public and private hospitals share a similar underlying cost structure. Costs broadly fall into two categories: outpatient and inpatient.

Outpatient care refers to treatment received without an overnight stay. Common examples include specialist consultations, diagnostic tests such as X-rays and blood work, and health screenings. Because outpatient treatments tend to be less resource-intensive, they are generally less expensive.

Inpatient care refers to treatment that requires a hospital admission. This includes room and board, nursing and medical care, and surgical procedures. Day surgeries also fall under this category, even if no overnight stay is involved. Inpatient costs are generally higher because they draw on more hospital resources and often involve more complex procedures.

Most of the significant bills Singaporeans face stem from inpatient care, which is why hospitalisation insurance coverage matters so much.

How Much Does a Hospital Stay Cost?

There is no single “average” hospital bill in Singapore. What you pay depends on three things: the procedure you need, the hospital you go to, and the ward class you choose. These variables can cause the same procedure to cost vastly different amounts.

Rather than relying on a broad average, MOH publishes a Bill Amount Information tool that allows you to look up estimated costs for specific procedures across different hospitals and ward classes. If you want to know what a particular treatment is likely to cost, that is the most reliable place to start.

The ward-class effect

The single biggest driver of cost variation is your choice of ward. Public hospitals in Singapore offer four ward classes: C, B2, B1, and A. Class C and B2 wards attract government subsidies, while B1 and A wards are unsubsidised. Private hospitals have no subsidised wards at all.

The difference in cost between a subsidised public ward and a private hospital can be dramatic.

Take a knee joint replacement as an example:

| Ward | Median Total Bill |

|---|---|

| Public – C | $6,993 |

| Public – B2 | $7,567 |

| Public – B1 | $24,358 |

| Public – A | $25,738 |

| Private | $48,746 |

The same procedure costs nearly seven times more in a private hospital than in a subsidised C ward. The jump from a B2 ward to a B1 ward (both within the same public hospital system) more than triples the bill. This is one of the most important things to understand about healthcare costs in Singapore: your ward choice is a financial decision as much as it is a medical one.

Note that these figures represent the median (50th percentile) total bill. For subsidised wards (C and B2), government subsidies are already reflected in the figures. MediSave withdrawals and insurance payouts are not factored in, so the actual amount you pay out of pocket will depend on your coverage.

For the most current and procedure-specific estimates, use MOH’s Bill Amount Information tool.

Example: The Cost of Treating Cancer

Cancer is the second most common reason for hospitalisation in Singapore and the leading cause of death. More than 17 Singaporeans die from it every day, and 1 in 4 Singaporeans is expected to develop cancer in their lifetime.

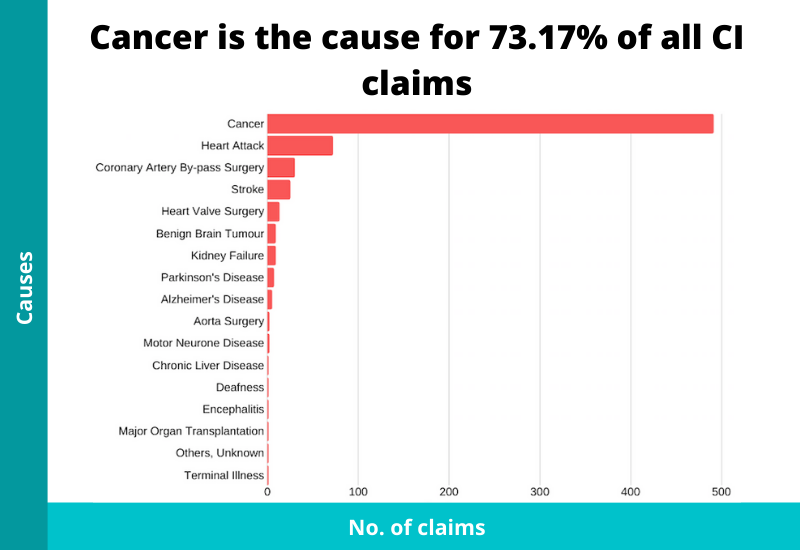

It is also the most common cause of both critical illness and death claims in Singapore, according to our analysis of life insurance claims data. Cancer alone accounts for over 73% of all critical illness claims.

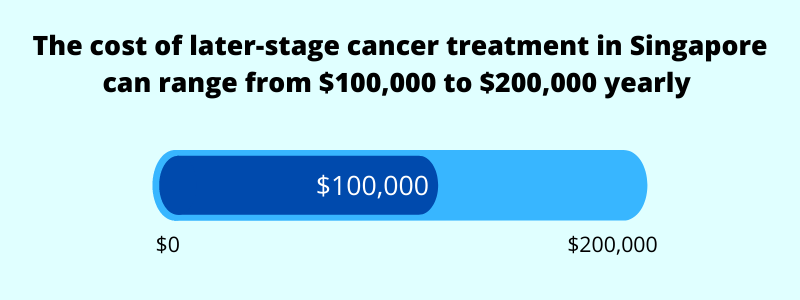

What makes cancer particularly costly is that treatment is rarely a single procedure. It typically involves a combination of diagnostic tests, surgery, radiotherapy, and chemotherapy, often sustained over months or years. Costs vary considerably depending on the type and stage of cancer, but for late-stage cancer, treatment can cost $100,000 to $200,000 per year.

Without comprehensive insurance coverage, bills of that magnitude can wipe out years of savings. This is why having the right hospitalisation and critical illness coverage in place before a diagnosis matters so much.

Other Examples: Heart Conditions and Stroke

Cancer is not the only condition that generates large hospital bills.

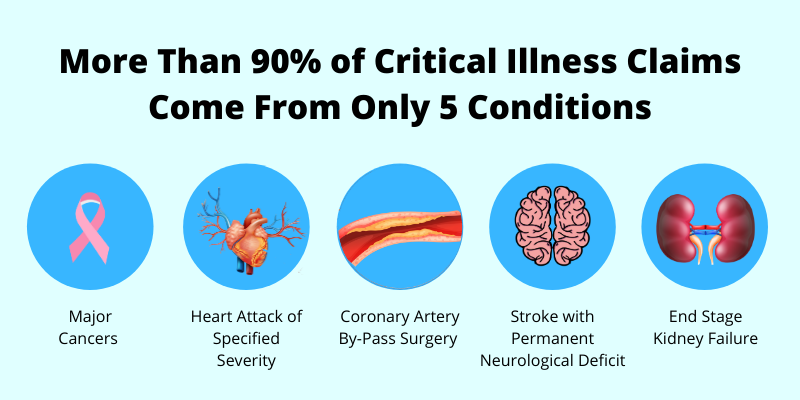

The five most common critical illnesses (major cancer, heart attack, coronary artery bypass surgery, stroke, and end-stage kidney failure) together account for more than 90% of all critical illness claims in Singapore.

Here is a closer look at two of them.

QUICK CHECK

Can you answer these three questions?

1) How much would your family receive if something happened to you tomorrow?

2) What monthly income will your savings and investments actually produce at 65?

3) Who gets your assets, in what proportion, if you never get round to a will?

Most people can answer one at best. Not because they're careless, but because nobody's shown them the order to work through things.

That order exists. Here's the 7-step framework, from income and protection through to investments and estate planning.

Heart conditions

A heart attack typically occurs when a blockage in the coronary artery restricts blood flow to the heart. One common treatment is a percutaneous coronary intervention (PCI), where a balloon catheter is used to open the blocked artery and a stent is inserted to keep it open.

Here are the median total bills for a multivessel PCI by ward class:

| Ward | Median Total Bill |

|---|---|

| Public – C | $7,027 |

| Public – B2 | $8,100 |

| Public – B1 | $25,572 |

| Public – A | $26,563 |

| Private | $58,852 |

Stroke

Stroke occurs when blood flow to the brain is interrupted, either by a clot or bleeding, causing brain cells to begin dying within minutes.

Here are the median total bills for a stroke admission by ward class:

| Ward | Median Total Bill |

|---|---|

| Public – C | $2,503 |

| Public – B2 | $2,795 |

| Public – B1 | $7,557 |

| Public – A | $9,525 |

| Private | $21,047 |

As with all the figures in this article, these are median total bills. For subsidised wards (C and B2), government subsidies are already reflected. MediSave withdrawals and insurance payouts are not factored in.

How to Reduce the Risk of Huge Medical Bills

Hospital bills can put serious strain on your savings. The good news is that Singapore has a well-structured system of schemes and insurance options to help manage that risk. Here is what is available.

1) MediShield Life

MediShield Life is Singapore’s national health insurance scheme. It is compulsory for all citizens and permanent residents, and you cannot opt out of it. Premiums are payable from your MediSave account.

The scheme provides basic hospitalisation coverage, primarily designed for stays in B2 and C ward classes at public hospitals. It also covers pre-existing conditions, which is an important distinction from private insurance.

One thing to be aware of is that MediShield Life premiums are increasing. Following a review in 2024, premiums are being raised in phases over three years, from April 2025 to March 2028, with the total increase capped at 35% and the average increase per policyholder reaching 22% by the end of the third year. These increases reflect the enhanced benefits the scheme now provides, but they do mean higher MediSave deductions going forward.

2) Integrated Shield Plans

If you want coverage beyond what MediShield Life provides, particularly for B1, A, or private hospital stays, you can upgrade with an Integrated Shield Plan (IP) offered by a private insurer. IPs build on top of MediShield Life and can include coverage for higher ward classes, private hospitals, and pre- and post-hospitalisation costs.

Most policyholders pair their IP with a rider to reduce their out-of-pocket costs further. However, rider rules changed significantly from 1 April 2026. New riders can no longer cover the minimum IP deductibles, which range from $1,500 to $3,500 depending on ward class. The annual co-payment cap has also doubled from $3,000 to $6,000, excluding the deductible. The minimum 5% co-payment requirement remains.

In practical terms, policyholders on new riders will face higher potential out-of-pocket costs when making a claim. The upside is that new rider premiums are projected to be around 30% lower on average than existing maximum coverage riders.

3) Healthier SG

One of the most effective ways to reduce the risk of a large hospital bill is to avoid hospitalisation in the first place. Healthier SG is a national preventive care initiative that encourages Singaporeans to enrol with a regular family doctor and take a more proactive approach to their health.

For enrolled citizens, nationally recommended vaccinations and health screenings covering cardiovascular risk factors, diabetes, high blood pressure, high cholesterol, and selected cancers are fully subsidised at participating clinics. Catching a problem early, before it requires hospitalisation, is almost always less costly, financially and otherwise.

4) Other Government Assistance

If you are still unable to meet your medical bills after MediShield Life and MediSave, you can apply to MediFund, an endowment fund set up by the government to help needy Singaporeans with their hospital expenses.

There is also the Medication Assistance Fund, which provides additional subsidies for eligible Singaporeans on drugs that are not in the Standard Drug List.

Covering Medical Costs Only Solves Half the Problem

Paying the hospital bill is only part of the challenge. What happens if you recover slowly and cannot work for an extended period? Your monthly expenses, loan repayments, and other financial commitments do not pause because you are in hospital.

This is where life insurance becomes important. Coverage for death, total and permanent disability, and critical illness can replace lost income during a period when you are unable to earn. Without it, even a well-insured hospital stay can lead to serious financial difficulty if recovery takes longer than expected.

Consider supplementing your hospitalisation coverage with early critical illness insurance, which pays out a lump sum on diagnosis rather than waiting until treatment is complete. Term insurance and whole life insurance can provide additional coverage for death and total and permanent disability, ensuring your dependants are protected as well.

If you are unsure whether you have enough coverage, you can get an estimate using our life insurance calculator.

Wrapping Up

Healthcare costs in Singapore are real and rising. The figures in this article are not meant to alarm, but to give you an honest picture of what a hospital bill can look like, and why it is worth being prepared.

The foundation is already in place for most Singaporeans: MediShield Life provides baseline hospitalisation coverage for all citizens and permanent residents. Building on that with an Integrated Shield Plan, the right level of critical illness cover, and healthy living habits gives you a much stronger position when something unexpected happens.

If you are not sure where your coverage currently stands, it is worth taking the time to review it.

BEFORE YOU GO

Everything on this site is written for everyone. But your financial goals, your responsibilities, and what you already have in place are yours alone.

FullCircle is our comprehensive financial planning session. You'll walk away with a clearer picture of where you stand and what to prioritise, across protection, retirement, and estate planning.