Recently in Singapore, there has been growing concern about rising medical costs.

In particular, discussions surrounding various types of insurance plans, including MediShield Life and its supplement, the Integrated Shield Plan, as well as fees charged by public and private doctors, are intensifying.

While many changes have been made to curb rising healthcare costs, they currently seem to be inadequate.

More changes are expected in the future, but for now, we’ll focus on the cost of healthcare and the average (and past) medical inflation rates in Singapore.

So, read on!

Summary of Key Findings

- From 2005 to 2025, the cost of healthcare has increased by 59.1%

- The healthcare inflation rate in 2025 was 2.7%

- Insurer-reported medical costs rose by 15.5% in 2025, and are projected to reach 16.9% in 2026

- In 2025, the cost of health insurance has risen by 12.7%

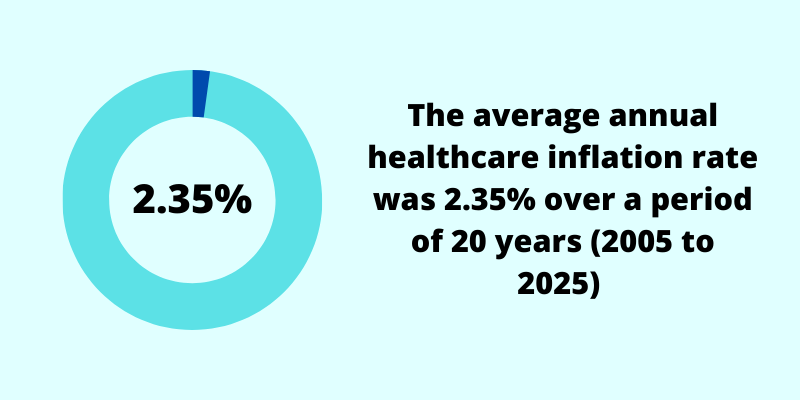

- The average healthcare inflation rate was 2.35% over 20 years (from 2005 to 2025)

SIDE NOTE

Most people's finances aren't a plan. They're a collection of separate decisions: a policy bought years ago, investments that don't talk to each other, a will that's still on the to-do list.

If that sounds familiar, there's a fix that doesn't require becoming a finance expert.

Here's the 7-step framework we use to organise everything into one system.

What Does Healthcare Inflation Mean?

Inflation happens when the prices of goods and services rise over time, usually measured yearly. On the other hand, negative inflation (or deflation) can also happen when such prices fall.

Generally, in a healthy economy, inflation happens as businesses and consumers spend and consume more. Higher demand (with supply being constant) pushes prices higher.

There are many categories of goods and services which make up Singapore’s overall inflation, and healthcare is one of them.

By just looking at the healthcare category, we’re able to gain insight into how the cost of healthcare changes over time.

The Healthcare Inflation Rate by Year (Singapore)

How much have the medical costs in Singapore risen?

One of the most reliable ways to measure inflation is by using the Consumer Price Index (CPI). This measure compiles national data from the Singapore Department of Statistics, and its objective is to measure the average change in prices of commonly consumed goods and services.

Healthcare is one of the 10 main categories that are tracked.

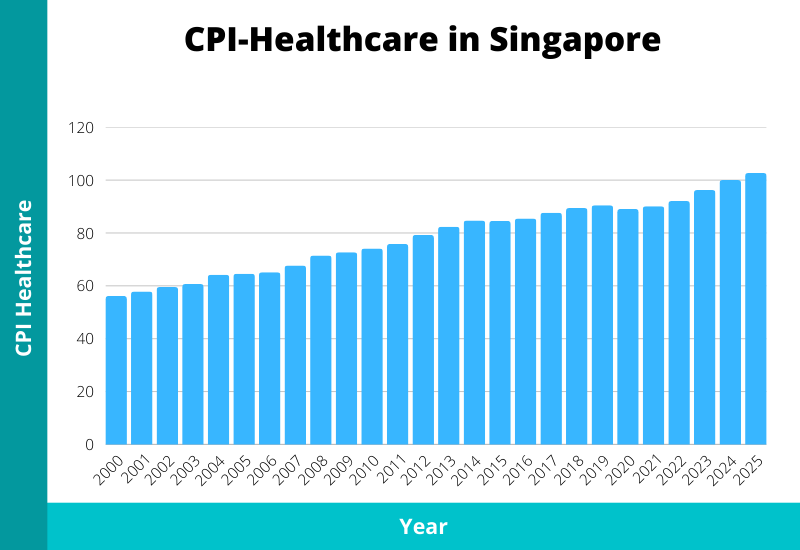

Here’s the CPI-Healthcare for the past 20 years:

| 2025 | 2024 | 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | 2013 | 2012 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | 2005 | 2004 | 2003 | 2002 | 2001 | 2000 | |

| CPI-Healthcare | 102.653 | 100 | 96.238 | 92.083 | 90.108 | 89.099 | 90.49 | 89.436 | 87.628 | 85.46 | 84.575 | 84.722 | 82.374 | 79.281 | 75.868 | 74.092 | 72.752 | 71.445 | 67.722 | 65.109 | 64.536 | 64.192 | 60.662 | 59.517 | 57.836 | 56.187 |

From 2005 to 2025, the CPI-Healthcare has increased by 59.1% (from 64.536 to 102.653). Hypothetically, this means that if an item in the healthcare category costs $10,000 in 2005, it’ll cost $15,910 in 2025.

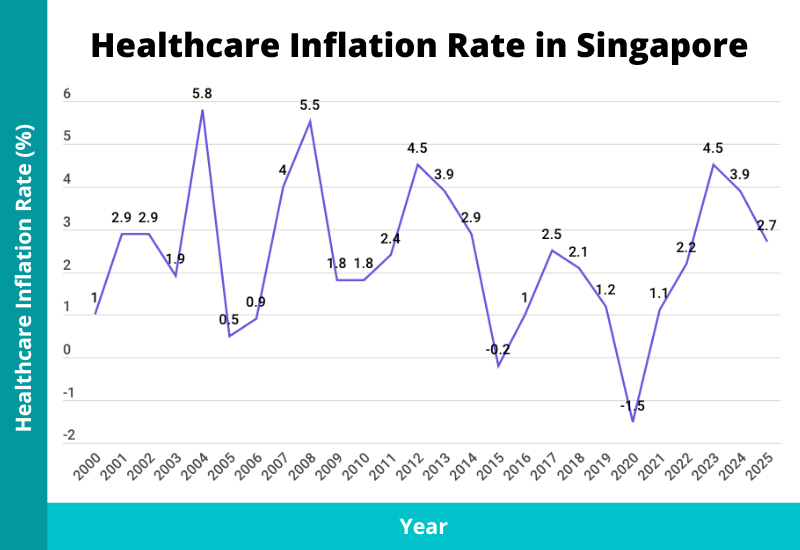

Here are the healthcare inflation rates by year:

| 2025 | 2024 | 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | 2013 | 2012 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | 2005 | 2004 | 2003 | 2002 | 2001 | 2000 | |

| CPI-Healthcare | 102.653 | 100 | 96.238 | 92.083 | 90.108 | 89.099 | 90.49 | 89.436 | 87.628 | 85.46 | 84.575 | 84.722 | 82.374 | 79.281 | 75.868 | 74.092 | 72.752 | 71.445 | 67.722 | 65.109 | 64.536 | 64.192 | 60.662 | 59.517 | 57.836 | 56.187 |

| Healthcare Inflation Rate (%) | 2.7 | 3.9 | 4.5 | 2.2 | 1.1 | -1.5 | 1.2 | 2.1 | 2.5 | 1.0 | -0.2 | 2.9 | 3.9 | 4.5 | 2.4 | 1.8 | 1.8 | 5.5 | 4.0 | 0.9 | 0.5 | 5.8 | 1.9 | 2.9 | 2.9 | 1.0 |

From the data, you can see a positive inflation happening every year except in 2015 and 2020, reflecting that the average prices are almost always increasing.

In 2025, there was an inflation of 2.7% in the healthcare category.

But this is just the main category of Healthcare. It can be broken down into subcategories:

- Medicines & Health Products

- Medicines & Health Supplements

- Medical Products

- Assistive Products

- Outpatient Care Services

- Fees At Polyclinics

- Fees At General Practitioners (GP) Clinics

- Fees At Specialist Outpatient Clinics

- Outpatient Dental Services

- Outpatient Care Services Nec

- Inpatient Care Services

- Other Health Services

- Diagnostic Imaging Services & Medical Laboratory Services

- Patient Emergency Transportation Services & Emergency Rescue

- Health Insurance

Let’s look at the data on the most interesting subcategories: Outpatient Care Services, Inpatient Care Services, and Health Insurance.

Outpatient Care Services:

| 2025 | 2024 | 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | |

| CPI-Outpatient Care Services | 99.734 | 100 | 96.118 | 90.82 | 88.299 | 88.078 | 91.749 | 90.485 | 89.029 | 86.956 | 84.629 | 88.495 |

| Outpatient Care Services Inflation Rate (%) | -0.3 | 4.0 | 5.8 | 2.9 | 0.3 | -4.0 | 1.4 | 1.6 | 2.4 | 2.7 | -4.4 | 2.0 |

Inpatient Care Services:

| 2025 | 2024 | 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | |

| CPI-Inpatient Care Services | 99.889 | 100 | 95.402 | 91.294 | 89.621 | 88.305 | 87.013 | 85.18 | 81.966 | 78.436 | 78.385 | 76.037 |

| Inpatient Care Services Inflation Rate (%) | -0.1 | 4.8 | 4.5 | 1.9 | 1.5 | 1.5 | 2.2 | 3.9 | 4.5 | 0.1 | 3.1 | 5.4 |

Health Insurance:

| 2025 | 2024 | 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | |

| CPI-Health Insurance | 112.679 | 100 | 95.164 | 91.845 | 90.092 | 85.888 | 85.88 | 85.832 | 85.457 | 84.094 | 83.662 | 83.703 |

| Health Insurance Inflation Rate (%) | 12.7% | 5.1 | 3.6 | 1.9 | 4.9 | 0 | 0.1 | 0.4 | 1.6 | 0.5 | 0 | 2.5 |

The Average Medical Inflation Rate in Singapore

In addition to knowing the yearly medical inflation rates, getting the average rate over a period of time will also help paint a clearer picture.

To get the average inflation rate, you can’t just take the sum of the yearly inflation rates (e.g., from 2005 to 2025) and divide it by the number of years.

The correct way to find the compound annual rate is by using this formula:

PV (1+r)^n = FV

Where

PV = the CPI-Healthcare of the 1st period

FV = the CPI-Healthcare of the 2nd period

n = the number of years

r = the annual compound rate

(You can use a financial calculator for this.)

And we’ll get the answer: 2.35%.

In short, over the past 20 years from 2005 to 2025, the average healthcare inflation rate in Singapore was 2.35%.

As the average healthcare inflation rate changes depending on the period used, here are other data:

| Average Healthcare Inflation Rate | |

| Over the last 10 years (2015 to 2025) | 1.96% |

| Over the last 20 years (2005 to 2025) | 2.35% |

| Over the last 30 years (1995 to 2025) | 2.38% |

Healthcare Inflation vs Headline (General) Inflation in Singapore

How does the cost of healthcare compare to the overall cost of living in Singapore?

To answer this question, let’s just look at the CPI All-Items for simplicity’s sake. There are, however, other measures, such as MAS Core Inflation.

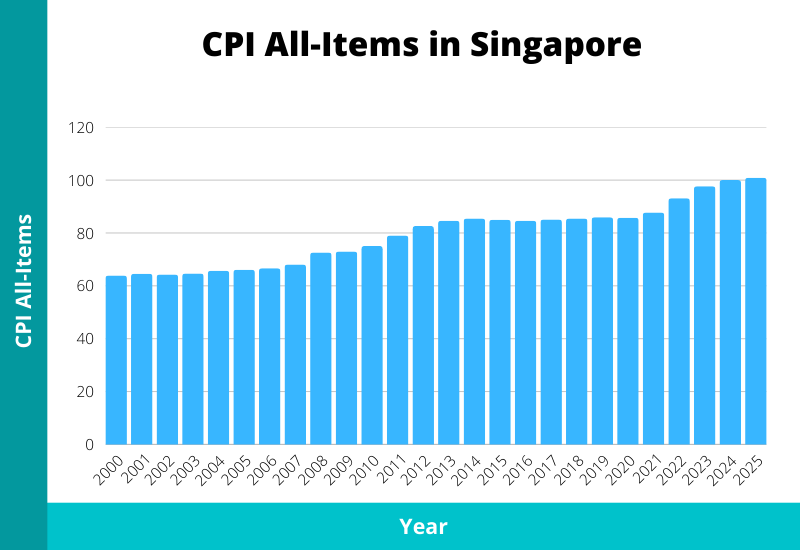

From 2005 to 2025, the CPI All-Items increased by 52.8%, while the CPI-Healthcare rose by 59.1%.

During that same period, the average headline inflation rate was 2.14%, while the average healthcare inflation rate was 2.35%.

So, what do these figures mean? The rising cost of healthcare outpaces the rising cost of living in Singapore.

QUICK CHECK

Can you answer these three questions?

1) How much would your family receive if something happened to you tomorrow?

2) What monthly income will your savings and investments actually produce at 65?

3) Who gets your assets, in what proportion, if you never get round to a will?

Most people can answer one at best. Not because they're careless, but because nobody's shown them the order to work through things.

That order exists. Here's the 7-step framework, from income and protection through to investments and estate planning.

What Insurers Are Seeing: Medical Cost Inflation in Singapore

The CPI data above shows how much consumer prices in the healthcare category have changed over time. But there is a second lens worth examining: what insurers themselves are experiencing in terms of medical cost increases.

These two measures often diverge significantly, and understanding why matters.

The insurer-reported medical inflation rate

According to WTW’s 2026 Global Medical Trends Survey, which surveyed 346 leading health insurers across 82 countries between June and July 2025, Singapore’s insurer-reported medical inflation rate was 15.5% in 2025. It is projected to climb further to 16.9% in 2026.

To put that in context, Singapore’s projected 2026 rate is well above the Asia Pacific (APAC) regional average of 14.0%, and more than one and a half times the global average of 10.3%.

Here is how Singapore compares:

| 2024 | 2025 | 2026 (Projected) | |

|---|---|---|---|

| Global | 9.5% | 10.0% | 10.3% |

| Asia Pacific | 11.8% | 13.2% | 14.0% |

| Singapore | 12.3% | 15.5% | 16.9% |

Why is the insurer figure so different from the CPI?

The CPI measures what consumers actually pay at the point of service. Because Singapore’s public healthcare system is heavily subsidised, that sticker price is significantly cushioned for most Singaporeans.

The WTW figure, by contrast, measures what healthcare is costing insurers before those subsidies, including rising utilisation rates and increasingly expensive technologies and treatments. They are measuring different things.

In short: the CPI of 2.7% in 2025 reflects what you as a consumer paid. The insurer figure of 15.5% reflects what your healthcare actually cost the system.

What is driving the increase?

According to WTW’s research, the top drivers of rising medical costs in Singapore and across APAC are:

- New medical technologies, cited by 77% of insurers as the primary driver

- Pharmaceutical advancements, named by 63% of insurers

- Little or no cost-sharing by policyholders, cited by 51%

From a disease standpoint, cancer is the leading cost driver globally. It is named as the fastest-growing and most expensive diagnosis by 58% of APAC insurers, with over 80% of insurers observing an increase in cancer incidence among individuals under the age of 40. Cardiovascular conditions ranked second (53%), followed by musculoskeletal conditions (34%), and diabetes (27%).

For Singapore specifically, WTW identified several local contributors: an ageing population, rising disease incidence, improved early detection, and the long-term management of conditions such as cancer, diabetes, and obesity. High operating costs driven by real estate prices and salaries, amid a shortage of healthcare workers, also feed into the trend.

The response from insurers has been to raise co-payments and deductibles, pushing more responsibility onto policyholders. This aligns with recent policy changes to MediShield Life premiums and Integrated Shield Plan rider rules, both of which are shifting a greater share of costs back to individuals.

What Can You Do About the Rising Costs?

Inflation, whether it’s general or healthcare, is driven by external factors. There are also specific reasons for the rise in healthcare costs, but it’s all out of your control.

However, you can better deal with it.

All Singaporeans – citizens and permanent residents – are covered by the national health insurance scheme, MediShield Life, which is meant to provide basic hospitalisation needs. We’re also given the option to enhance this coverage with an Integrated Shield Plan (IP).

In my view, getting “the best of the best” health insurance plans may not have broken the bank previously, but we may have to move away from those plans in the future simply because they’re either too expensive or they’re not available anymore.

We might need to look towards a solution that provides “value” instead, where co-payments are involved. That way, premiums remain affordable, and you’re still able to be covered substantially. Even when accidents happen, your savings will not take a huge hit.

Don’t forget to supplement your health insurance with other types of insurance policies, such as term insurance, whole life insurance, and early critical illness insurance.

And we should also remember the most underrated solution of all: implementing healthy living habits. That will certainly help you keep clear of hospitals.

BEFORE YOU GO

Everything on this site is written for everyone. But your financial goals, your responsibilities, and what you already have in place are yours alone.

FullCircle is our comprehensive financial planning session. You'll walk away with a clearer picture of where you stand and what to prioritise, across protection, retirement, and estate planning.