Medical costs in Singapore are rising faster than most people realise. And of all the conditions driving that increase, cancer sits at the top.

Not just because of how common it is, but because of how expensive it has become to treat. Surviving cancer today often means years of ongoing treatment, maintenance drugs, and follow-up care. The financial tail is much longer than it used to be.

There is also a newer variable: the Cancer Drug List (CDL). Not all cancer drugs are covered by MediShield Life, and if your prescribed drug is not on the approved list, you may face significant out-of-pocket costs. The right insurance plans, particularly those covering early-stage critical illnesses, can help mitigate this risk.

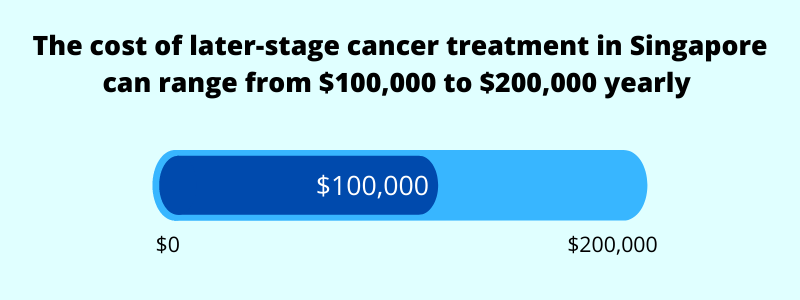

The numbers involved are significant. Late-stage cancer treatment in Singapore can easily cost $100,000 to $200,000 a year, or roughly $8,400 to $16,700 a month.

In Summary

- Cancer is the leading cause of death in Singapore, accounting for 26.2% of all deaths

- Around 50 Singaporeans are diagnosed with cancer every day

- The lifetime risk of developing cancer by age 75 is 1 in 4

- Cancer drives 73% of all critical illness claims and 40% of all death claims

- Late-stage cancer treatment can cost $100,000 to $200,000 a year (or $8,400 to $16,700 a month)

- Private hospital cancer treatment over 18 months can range from $98,000 for prostate cancer to $273,000 for lung cancer

- If your cancer drug is not on the CDL, MediShield Life will not cover it. Some IP riders may provide partial coverage, but this varies by plan

SIDE NOTE

Most people's finances aren't a plan. They're a collection of separate decisions: a policy bought years ago, investments that don't talk to each other, a will that's still on the to-do list.

If that sounds familiar, there's a fix that doesn't require becoming a finance expert.

Here's the 7-step framework we use to organise everything into one system.

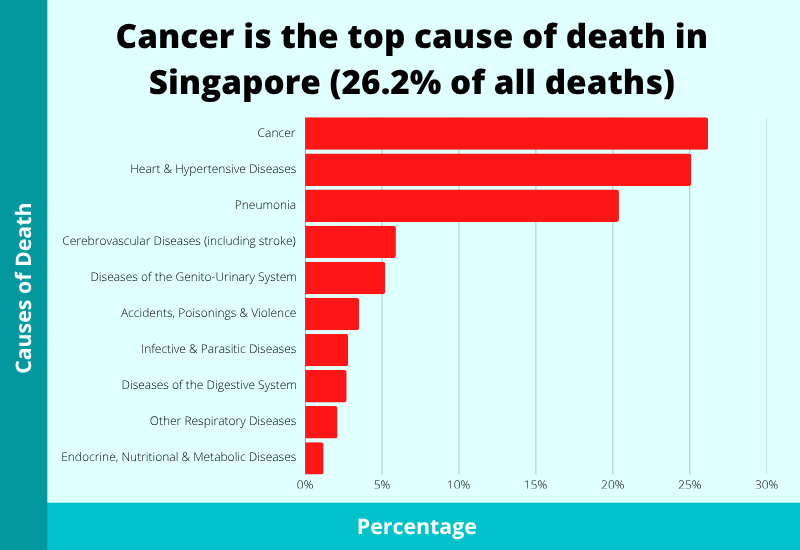

Why Is Cancer a Big Issue in Singapore?

Cancer is the leading cause of death in Singapore. It accounts for 26.2% of all deaths, or more than one in every four.

And while Singapore’s average life expectancy of 83 years is something to be proud of, living longer also means a greater likelihood of encountering a serious illness along the way.

The scale of cancer in Singapore is worth understanding.

Around 50 Singaporeans are diagnosed with cancer every single day. The lifetime risk of developing cancer by age 75 is estimated at 1 in 4, with male and female lifetime risks sitting at 26.8% and 26.2% respectively, according to the SCR Annual Report.

There is also a worrying trend among younger Singaporeans. Over 80% of insurers globally have observed a rise in cancer incidence among people under the age of 40, according to WTW’s 2026 Global Medical Trends Survey.

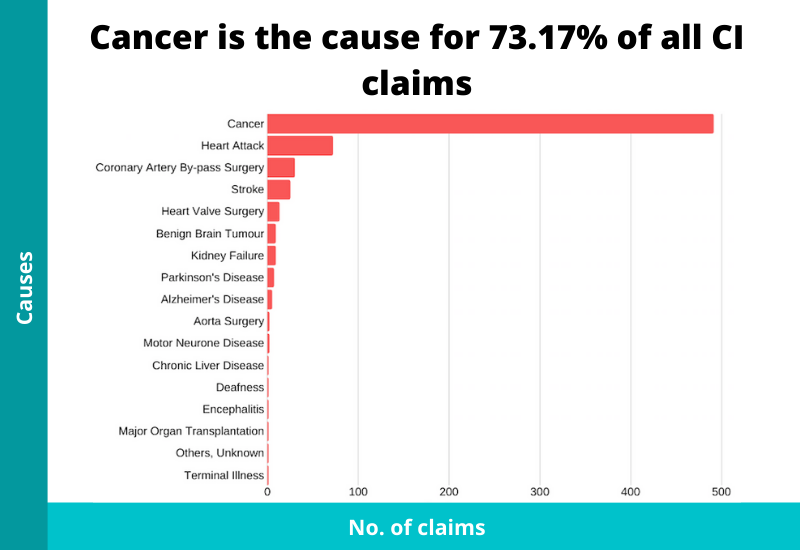

When we look at life insurance claims data, cancer accounts for 73% of all critical illness claims.

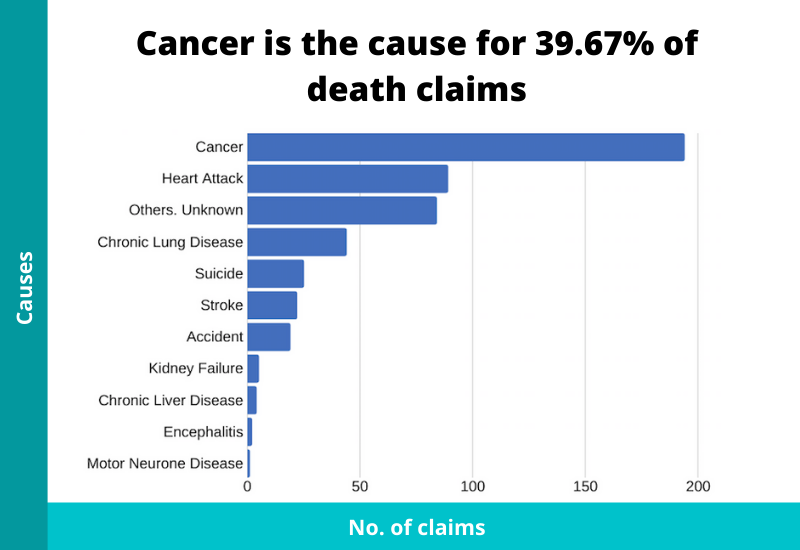

It is also responsible for 40% of all death claims.

No other condition comes close.

The Survival Picture Has Changed

Here is where the story gets more nuanced.

Overall five-year cancer survival rates in Singapore have improved dramatically, from 22.6% in the late 1970s to 61.4% in the 2019 to 2023 period. More people are surviving cancer today than ever before.

But this comes with a financial consequence that is easy to overlook.

Surviving cancer no longer means a single surgery and a clear bill of health. It often means years of maintenance drugs, regular follow-up scans, specialist reviews, and ongoing care. The financial exposure does not end when the treatment does. For many patients, it stretches on for years afterwards.

That is why cancer demands more financial planning attention than any other critical illness.

The Most Common Cancers in Singapore

Before we get into costs, it helps to know which cancers are most prevalent here, as that shapes everything from screening decisions to insurance planning.

According to the SCR Annual Report, here are the top cancers for men and women:

Top cancers in men:

| Type of Cancer | Percentage |

|---|---|

| Prostate | 18.0% |

| Colorectal | 15.8% |

| Lung | 13.2% |

Top cancers in women:

| Type of Cancer | Percentage |

|---|---|

| Breast | 29.9% |

| Colorectal | 12.6% |

| Lung | 8.1% |

For the full rankings, refer to our cancer statistics article.

Survival rates vary widely by cancer type

Not all cancers carry the same prognosis, and this has a direct bearing on the financial planning conversation.

Some cancers now have very high five-year survival rates. Prostate cancer sits at 90.3%, breast cancer at 84.2%, and non-melanoma skin cancers above 93%. Others remain very difficult to treat. Lung cancer has a five-year survival rate of just 24.2% for men, and pancreatic cancer sits at around 13%.

The key point is this: higher survival rates are good news, but they also mean longer treatment timelines and more years of ongoing costs. Surviving longer does not mean spending less.

Factors that Influence the Cost of Cancer Treatments

Medical costs in Singapore are rising significantly. According to WTW’s 2026 Global Medical Trends Survey, medical costs in Singapore rose 15.5% in 2025 and are projected to reach 16.9% in 2026, the highest rate in the region. Cancer is cited as the single biggest driver of that increase.

But within cancer itself, costs vary enormously from patient to patient. Here are the key factors that determine how much you end up paying.

1) Stage of cancer at diagnosis

The later the stage at diagnosis, the higher the cost of treatment. Advanced-stage cancer typically requires more aggressive and prolonged treatment, which adds up quickly. Early detection almost always means lower costs and better outcomes.

2) Potential for complications

If cancer is located near a vital organ, the complexity of treating or removing it increases. Complications along the way, including relapses or a weakened condition, can require additional care and extend the treatment period significantly.

3) Preferred hospital and ward class

Treatment at a private hospital costs considerably more than at a public hospital, and even within public hospitals, ward class makes a material difference. Most Singaporeans want the best care available when it comes to cancer, which is understandable. But it is worth knowing upfront what that choice costs.

4) Type of treatments needed

A single treatment is rarely sufficient. Most patients require a combination of surgery, chemotherapy, radiotherapy, and increasingly, immunotherapy or targeted drug therapies. The more treatments needed, and the longer they run, the higher the total bill.

5) Cancer Drug List (CDL) status

This is now one of the most significant cost variables of all.

The CDL is MOH’s approved list of cancer drugs covered under MediShield Life. If your oncologist recommends a drug on the list, your insurance can help pay for it. If the drug is not on the list, MediShield Life will not cover it. Some IP riders may offer partial coverage for certain non-CDL drugs, but the extent of that coverage varies by insurer and plan, and is not guaranteed.

Given that drug costs are the single biggest expense in cancer treatment, as you will see in the sections below, the CDL status of your prescribed drugs can mean the difference between a manageable bill and a financially devastating one.

The Different Types of Cancer Treatment Costs

There are two broad phases: diagnosis and treatment. Both come with significant costs, and both need to be planned for.

1) Diagnostic tests and screenings

With cancer, waiting for symptoms to appear can be costly. By the time symptoms show up, the cancer may already be at an advanced stage.

That is why regular screenings matter. Common diagnostic tests include blood tests, MRI scans, CT scans, PET-CT scans, colonoscopies, mammograms, and biopsies.

If imaging alone is inconclusive, a biopsy may be needed to extract and analyse tissue from the affected area.

Here are the average costs of biopsies by cancer type:

| Type of Cancer | Type of Hospital | Average Bill Size |

|---|---|---|

| Breast | Private | $9,598 |

| Public (Unsubsidised) | $4,047 | |

| Public (Subsidised) | $1,193 | |

| Lung | Private | $6,822 |

| Public (Unsubsidised) | $2,472 | |

| Public (Subsidised) | $605 | |

| Colorectal | Private | $3,241 |

| Public (Unsubsidised) | $1,740 | |

| Public (Subsidised) | $644 | |

| Prostate | Private | $12,006 |

| Public (Unsubsidised) | $4,530 | |

| Public (Subsidised) | $1,470 |

Source: MOH fee benchmarks. Bills listed can be for either inpatient or day surgeries.

Note that even after treatment is complete, many of these tests will need to be repeated regularly to monitor for recurrence.

QUICK CHECK

Can you answer these three questions?

1) How much would your family receive if something happened to you tomorrow?

2) What monthly income will your savings and investments actually produce at 65?

3) Who gets your assets, in what proportion, if you never get round to a will?

Most people can answer one at best. Not because they're careless, but because nobody's shown them the order to work through things.

That order exists. Here's the 7-step framework, from income and protection through to investments and estate planning.

2) Surgeries

Cancer surgery is one of the oldest and most effective forms of treatment. It involves removing the tumour and, where necessary, surrounding tissue to ensure complete removal.

How the surgery is performed, whether open or minimally invasive, also affects the cost. Surgeries are often paired with other treatments such as chemotherapy or radiotherapy.

Here are the average costs of cancer surgeries:

| Type of Cancer | Type of Hospital | Average Bill Size |

|---|---|---|

| Breast | Private | $32,378 |

| Public (Unsubsidised) | $12,014 | |

| Public (Subsidised) | $3,404 | |

| Lung | Private | $76,758 |

| Public (Unsubsidised) | $36,277 | |

| Public (Subsidised) | $7,479 | |

| Colorectal | Private | $55,865 |

| Public (Unsubsidised) | $23,887 | |

| Public (Subsidised) | $6,288 | |

| Prostate | Private | $67,809 |

| Public (Unsubsidised) | $28,409 | |

| Public (Subsidised) | $8,850 |

Source: MOH fee benchmarks. Bills listed can be for either inpatient or day surgeries.

3) Chemotherapy

Chemotherapy uses drugs to kill cancer cells or stop them from spreading. It can be administered intravenously or orally, and is often used in cycles over several months.

Because chemotherapy affects the whole body, side effects can be significant, including fatigue and hair loss. The cost depends on the type of drugs used and how frequently they are administered.

| Type of Hospital | Average Bill Size |

|---|---|

| Private | $12,766 |

| Public (Unsubsidised) | $2,058 |

| Public (Subsidised) | $774 |

Source: MOH fee benchmarks. Bills listed can be for either inpatient or day surgeries.

4) Radiotherapy

Radiotherapy uses high doses of radiation to kill cancer cells in a targeted area. Unlike chemotherapy, it does not affect the whole body. However, there is a lifetime limit on how much radiation any given area can receive.

The cost of radiotherapy in Singapore ranges from $25,000 to $30,000.

5) Immunotherapy and newer treatments

Immunotherapy is increasingly common, particularly for late-stage cancers. It works by stimulating the body’s own immune system to identify and attack cancer cells.

It is also among the most expensive treatments available. According to Singlife, a single dose costs approximately $9,000, administered every two to three weeks. Over a full course of treatment, total costs can reach $156,000 to $234,000.

Some newer immunotherapy drugs may not yet be on the CDL, meaning MediShield Life may not cover them. Some IP riders may offer partial coverage for certain non-CDL drugs, but the extent of that coverage depends on your specific plan.

6) Post-discharge and hidden costs

This is the part that most people do not plan for.

Once active treatment ends, the costs do not stop. Follow-up PET-CT scans and specialist reviews continue for years. Many patients remain on long-term maintenance drugs to prevent recurrence. These ongoing costs are real and can stretch well into the future.

There are also indirect costs that rarely appear on any hospital bill: transport to frequent medical appointments, domestic help or childcare when the patient is too fatigued to manage daily responsibilities, and in more advanced cases, palliative or hospice care.

These hidden costs are not covered by most insurance plans. They are worth factoring into your financial planning long before a diagnosis occurs.

The Average Cost of Treating Cancer in Singapore

With so many variables involved, there is no single number that captures the cost of cancer treatment. But we can get reasonably close.

According to insights from Seedly and the Singapore Cancer Society, late-stage cancer treatment in Singapore can easily cost $100,000 to $200,000 a year, or roughly $8,400 to $16,700 a month.

To see how these costs accumulate in practice, claims data from Singlife covering an 18-month period at private hospitals (May 2023 to October 2024) gives a more granular picture:

| Type of Cancer | Total Cost (18 Months) | Primary Cost Driver |

|---|---|---|

| Lung | ~$273,000 | Drug treatment (~$190,000) |

| Breast | ~$184,000 | Drug treatment (~$156,000) |

| Colorectal | ~$128,000 | Drug treatment (~$65,000) |

| Prostate | ~$98,000 | Drug treatment (~$87,000) |

Note: Figures are based on private hospital claims and exclude pre and post-hospitalisation costs.

The pattern across all four cancers is clear: drug costs are the dominant expense, accounting for the majority of the total bill in every case. This is precisely why the CDL status of your prescribed drugs matters so much, and why a gap in drug coverage can translate quickly into a very large out-of-pocket bill.

To put these figures in context, Singapore’s median household income sits at around $10,000 a month. A lung cancer diagnosis treated at a private hospital could consume close to two and a half years of a household’s total income over just 18 months of treatment.

How to Finance the Costs

Knowing the costs is one thing. Knowing how to cover them is another. Here is a breakdown of your options.

1) MediShield Life

MediShield Life is Singapore’s compulsory basic health insurance scheme, covering all citizens and permanent residents. It provides a baseline level of protection, primarily calibrated for treatments at B2 and C class wards in public hospitals.

For cancer specifically, MediShield Life covers treatments on the CDL, up to the applicable claim limits. If you choose a private hospital or an A-class ward, or if your treatment involves drugs not on the CDL, MediShield Life will not bridge that gap.

Think of it as a foundation, not a full solution.

2) The Cancer Drug List (CDL)

The CDL was introduced by MOH to manage the rising cost of cancer drug treatments and ensure that public subsidies are directed towards drugs with proven clinical benefit.

Here is how it works in plain terms.

The Cancer Drug Treatment Limit covers the cost of approved cancer drugs on the CDL. If your oncologist prescribes a drug on the list, MediShield Life and your IP can help pay for it, up to the stated limits.

The Cancer Drug Services Limit covers supportive care that accompanies your treatment, such as blood tests, follow-up scans, and medications to manage side effects like nausea, pain, or infection risk. This limit applies even if your main cancer drug is not on the CDL, meaning some of your treatment-related costs can still be claimed in that scenario.

If your prescribed drug is not on the CDL, MediShield Life will not cover the drug cost itself. Your options at that point include discussing alternative CDL-listed drugs with your oncologist, applying for assistance through the Medication Assistance Fund if the drug is on the MAF list, or relying on an IP rider that offers partial coverage for certain non-CDL drugs, subject to your plan’s terms.

3) Integrated Shield Plans

An Integrated Shield Plan (IP) is a private insurance upgrade on top of MediShield Life. It extends your coverage to higher ward classes and private hospitals, and typically includes benefits that MediShield Life does not, such as pre and post-hospitalisation costs.

Adding a rider to your IP can further reduce your out-of-pocket expenses by covering deductibles and co-insurance. Some riders also offer partial coverage for non-CDL drugs, though the extent of this varies by insurer.

A portion of your IP premium can be paid using MediSave, with the remainder in cash.

Note: If you have pre-existing conditions, getting coverage may be difficult. The best time to get an IP in place is when you are healthy.

4) Government and other financial assistance

If your hospital bills remain unmanageable even after MediShield Life claims and MediSave, there are further options available.

MediFund is a government endowment fund that helps Singapore citizens who face difficulties paying their remaining hospital bills. You can approach a Medical Social Worker at your public healthcare institution to apply, provided you are receiving subsidised care.

The Medication Assistance Fund (MAF) subsidises high-cost cancer drugs at public healthcare institutions that are not on the standard drug list but have been assessed as clinically necessary. It is available to eligible subsidised patients, with Singapore citizens receiving up to 75% in subsidies and permanent residents up to 20%.

Organisations such as the Singapore Cancer Society also offer financial assistance and support to patients who need it.

5) Life insurance and critical illness coverage

The financing options above address the cost of treatment. But there is a second financial blow that often goes unplanned for: the loss of income.

A cancer diagnosis frequently means time away from work, sometimes for an extended period. In many cases, a spouse or family member also reduces their working hours or stops work entirely to provide care. That is a potential double loss of household income at precisely the moment when expenses are at their highest.

This is where life insurance with critical illness (CI) coverage plays a critical role. A CI payout is a lump sum paid directly to you upon diagnosis. It is not tied to specific medical bills. You can use it to cover treatment costs not reimbursed by your IP, ongoing household expenses, loan commitments, or to replace lost income while you recover.

Most term insurance and whole life insurance plans allow you to add a CI rider covering all stages of illness. If you want standalone coverage, there are also early critical illness plans that pay out at an earlier stage of illness, giving you more financial breathing room before costs escalate further.

You can use our life insurance calculator to estimate how much CI coverage you may need.

Wrapping Up

Cancer is the one critical illness that demands your financial attention more than any other. The costs are high, the treatment timelines are long, and the variables involved, from hospital choice to CDL drug status, can shift the bill dramatically in either direction.

The good news is that there is a clear framework for protecting yourself. MediShield Life provides the base. An Integrated Shield Plan extends your coverage for hospitalisation. And a critical illness plan plugs the gaps that neither can fill, including lost income and out-of-pocket drug costs.

If you are unsure where your current coverage stands, start with our life insurance calculator to get a sense of how much CI coverage you may need. From there, you can explore term insurance, whole life insurance, or a standalone early critical illness plan depending on what suits your needs.

The best time to get these plans in place is before you need them.

BEFORE YOU GO

Everything on this site is written for everyone. But your financial goals, your responsibilities, and what you already have in place are yours alone.

FullCircle is our comprehensive financial planning session. You'll walk away with a clearer picture of where you stand and what to prioritise, across protection, retirement, and estate planning.