Compare and get personalised quotes from 19 life insurance providers to find the best maternity insurance plan in Singapore for your needs.

What Is Maternity Insurance & Why Is It Important?

Maternity insurance provides a lump sum payout and/or a hospital cash benefit if the pregnant mother suffers a pregnancy complication and needs to be hospitalised.

It also covers the newborn if the baby is diagnosed with a congenital illness. Some pregnancy insurance plans even allow the newborn to get life insurance coverage despite being born with medical conditions.

Maternity plans can come as standalone policies or bundled with another plan.

The payouts ensure you don’t need to dig into your hard-earned savings for unexpected medical costs, which are usually not covered by regular health insurance.

Enjoy greater peace of mind and give the best to your baby.

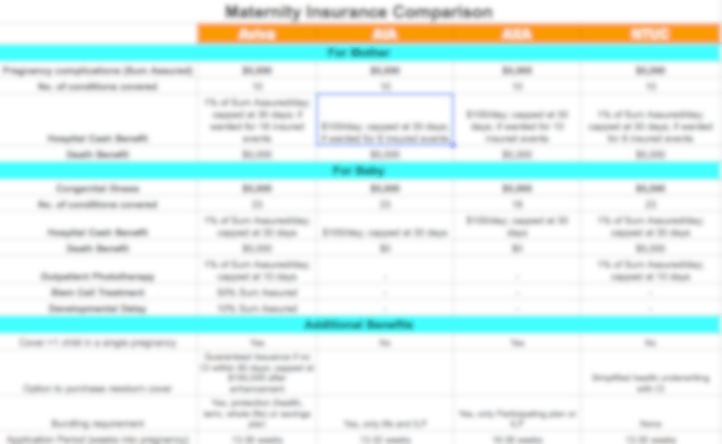

Best Maternity Insurance in Singapore (Comparison for 2026)

Here’s a non-exhaustive list of pregnancy plans that we can compare:

| Insurance Company | Plan Name |

|---|---|

| AIA | Mum2Baby Protect [Baby Protect Plus (III)] |

| Singlife | Singlife Maternity Care |

| HSBC Life (formerly AXA) | HappyMummy / HappyFamily (EmpoweredMum) |

| Manulife | ReadyMummy |

| Income Insurance (formerly NTUC Income) | Maternity 360 |

Singlife Maternity Care

Singlife Maternity Care protects mother and baby over a three-year term, with the premium paid once upfront. For a limited period, it can be purchased as a standalone policy without having to sign up for a qualifying plan.

The plan covers 10 types of pregnancy complications, 23 congenital illnesses, and loss of life. Both mother and child also receive financial assistance if hospitalised due to illnesses or pregnancy complications.

What is unique about this plan is its coverage for multiple births. It covers up to 4 babies in a single pregnancy, with each baby insured as a separate child, and accepts pregnancies through IVF. It also provides a one-time payout if the child requires stem cell transplant surgery or shows developmental delay.

After birth, you can buy a Singlife Whole Life Choice policy for your newborn within 90 days without medical underwriting. Eligible policyholders can also enrol their newborn in Singlife Shield within 180 days.

Manulife ReadyMummy

Manulife ReadyMummy is a standalone maternity plan that covers the expecting mother from the 13th week of pregnancy onwards, and the child from birth until the end of the three-year term.

The plan covers the mother against 14 pregnancy complications, including miscarriage due to accident, and the child against 24 congenital illnesses. Both mother and child receive a daily hospital cash benefit for each day of hospital stay, and pregnancies through IVF can be covered with an additional premium.

What is unique about this plan is its mental wellness benefit. ReadyMummy is the first of its kind to cover psychotherapy treatment, providing mental wellness support for the mother.

Within 90 days of birth, you also have the option to buy eligible Manulife plans with critical illness riders for your child with no health questions asked.

HSBC Life HappyMummy

HSBC Life HappyMummy pairs a pre-natal plan, EmpoweredMum, with a whole life plan, HSBC Life – Life Treasure III.

The mother is covered for 15 pregnancy complications, hospitalisation, and death, while the newborn is covered for 26 congenital illnesses, developmental delays in gross motor or speech development, hospitalisation, and death.

What is unique about this plan is its caesarean coverage, a first in the Singapore market. A payout is made if the mother delivers by caesarean section at less than 36 weeks of gestation.

You can also opt to transfer the base plan’s coverage from mother to newborn within 60 days of birth without underwriting. In addition, you can apply for an HSBC Life Shield Plan B cover for your newborn within 60 days of birth, with premiums waived for the first year.

AIA Mum2Baby Protect

AIA Mum2Baby Protect is a bundled maternity plan. It consists of a whole life base plan, AIA Guaranteed Protect Plus, paired with a pre-natal rider to form a maternity plan with all-round protection for the pregnant mum and child from as early as the 13th week of pregnancy.

The mother is covered for pregnancy complications, hospitalisation, death, and even childbirth medical negligence. The baby is covered against congenital illnesses, with a hospital care benefit for events such as incubation, neonatal ICU stays due to premature birth, and severe neonatal jaundice.

The plan also includes a Major Hospitalisation Care Benefit, which provides a payout if the mother is hospitalised for more than 30 days or spends at least 5 days in the ICU.

Within 100 days of birth, you can transfer the base plan and its riders to your child with no medical questions asked, giving your child guaranteed lifelong protection.

Income Insurance Maternity 360

Income Insurance Maternity 360 is a single-premium plan that covers both mother and baby over a three-year term.

The mother is covered for pregnancy complications, hospitalisation, and death, while the child is covered for congenital illnesses, hospitalisation, and death. There’s also an outpatient phototherapy benefit if the baby needs treatment for severe neonatal jaundice using a rented phototherapy machine at home.

The plan accepts applications from expectant mothers between 13 and 35 weeks of pregnancy, with an entry age from 17 to 44.

Through the simplified application benefit, you can take up an eligible plan for your child within 60 days of birth based on a simplified health declaration.

We Compare 19 Insurance Companies to Find the Best Maternity Insurance Plan for Your Needs

Our Trusted Providers

- AIA

- Allianz

- China Life

- China Taiping

- Etiqa

- Friends Provident

- FWD

- HSBC Life

- Income Insurance

- Life Insurance Corporation

- Manulife

- Monument International

- Raffles Health

- Singlife

- Sun Life

- Swiss Life

- Tokio Marine

- Transamerica

- Utmost International

Frequently Asked Questions

- What is a maternity insurance plan in Singapore?

It is a policy that provides a lump sum payout and/or a hospital cash benefit if the mother or the newborn suffers from an insured condition. Bundled maternity plans usually come with a wider scope of coverage. - Is maternity insurance necessary?

While most babies are born without issues, it is not always the case. When there are medical issues, it may become harder for the child to get hospitalisation and life insurance coverage later on. Maternity plans typically allow you to purchase coverage for your newborn with no or simplified underwriting, even if the baby is born with medical conditions. - Is this service free?

Yes, there’s no fee involved. - How long does the appointment take?

It typically takes around 45 minutes. However, it can be longer for more complex situations or if you have further questions. - Are there any obligations?

Depending on your situation, we may or may not recommend solutions. If we do, it’s entirely up to you to go ahead with it. As consumers ourselves, we dislike high-pressure tactics. - Should I bring my existing policies?

Yes! If you do have them, do bring them along (or a policy summary) as we can provide more accurate feedback. - How is this appointment conducted?

This can be done over a zoom video call or a meet-up.