All things in life have a certain balance.

For example, a balanced healthy diet ensures optimal health. Overeating (or undereating) of a particular type of food results in unfavourable health implications.

Likewise, overexposure (or underexposure) to a certain asset class could cause negative effects on our portfolio’s performance.

And that’s why we should have a well-balanced asset allocation to ensure our investments are kept within parameters.

Today, we’ll look at how asset allocation, diversification and rebalancing play a part in the grand scheme of things.

So, read on!

3 Quick Reasons Why We Should Invest

Investing is an important aspect of proper financial planning.

Here are 3 reasons why:

SIDE NOTE When was the last time you conducted thorough financial planning or reviewed your finances? In this day and age in Singapore, doing so will absolutely improve the quality of life for you and your loved ones. Here are 5 reasons why financial planning is so important.

1) Make use of our disposable income

The best type of investments you can make are in your career and/or business, especially in our early life stages.

That’s because you should be great at what you do – in terms of knowledge and execution. In return, you’re rewarded accordingly.

These “returns on investments” come in various forms:

- higher salary

- promotions

- performance bonuses

- etc

All these give you a bigger pool of money which should be put into better use.

2) Doing nothing hurts even more

When you do nothing with your excess cash, you should expect nothing in return.

But in reality, it’s even worse.

With the low interest rates in the bank savings accounts and the much higher inflation rate, you’re losing value over time.

In years to come, you’d realise that you don’t have as much as you thought.

It’s a silent killer.

3) Exploit the compounding effect

Investments can give you returns.

But staying invested throughout can give you even greater returns.

And that’s evident by the power of compounding:

The value of investments grow exponentially because of 2 components: (interests on your principal) + (interests on your interests).

So knowing about investments is vital if you want to achieve a strong financial standing.

But First, Ensure Protection Is In Place

I get the enthusiasm of wanting to make more money.

But sometimes, taking a step back can allow you to push forward easier.

Having sufficient insurance coverage may seem counter-intuitive as it’s an expense, but it may also turn out to be your greatest asset one day.

How?

Firstly, having proper hospitalisation coverage (MediShield Life and the Integrated Shield Plan) allows you to eliminate the risk of paying for huge medical bills which can wipe out your entire savings/investments, and even more.

Secondly, as your income contributes to almost everything, losing it will almost certainly put you in no man’s land.

Without life insurance coverage in place, and a permanent loss of income happens (death, total and permanent disability, and critical illnesses), there’ll be no insurance payout.

Where are you going to find the money to pay for all the day-to-day expenses, and your future commitments including retirement and kid’e education?

So if you’re not sure whether you have adequate life insurance coverage, check out our life insurance coverage calculator.

And the solutions to this are simple: term insurance, whole life insurance or early critical illness plans.

When you can eliminate the “what ifs”, it gives you the peace of mind to pursue the things that are within your control.

What Is Asset Allocation

When you’re just getting started on your investment journey, you start with a clean sheet of paper with no clue on what to invest in.

Asset allocation then becomes a decision-making process to answer questions such as:

- What type of asset classes to hold

- The percentage of each selected asset class

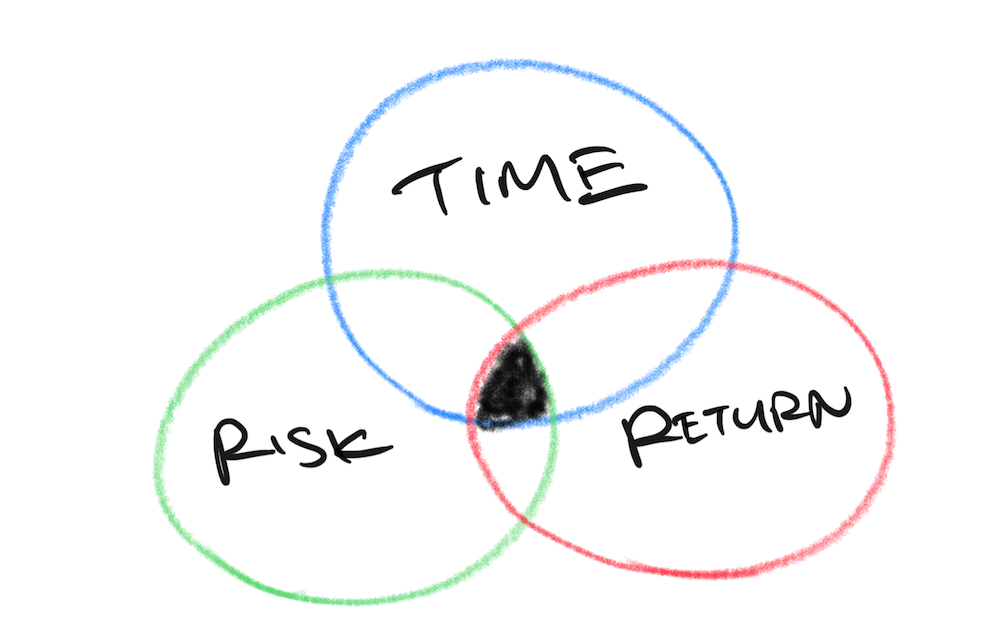

The answers to those questions would’ve considered your investment time horizon, risk profile, and expected returns, which all play a part.

Ultimately, you’re then be able to divide your surplus cash according to the allocation, and be able to cap how much risk you’re exposed to.

What Types of Asset Classes Are There

In the world of investments, there are certainly different types of assets you can hold.

But in my opinion, there are 3 main ones:

- Cash and Cash Equivalents

- Bonds (Fixed Income)

- Equities (Stocks & Shares)

In this article, the focus is on those 3. There are also subclasses within each asset class (e.g large-cap, small-cap stocks, industry specific, etc)

There’s still a little bit of information on other assets towards the later part.

1) Cash and Cash Equivalents

In cash and its equivalents, there are certain characteristics to them:

- the value doesn’t fluctuate much or at all

- low risk

- liquidable

- low expected returns

Assets under this category could be bank savings accounts (including high yield), fixed deposits, and money market funds.

Holding cash and its equivalents have its purposes:

- as a storage of value before making long term financial decisions

- for the extremely risk-averse people

- emergency funds that require quick access

- when you need to use it in the short term – whether it’s for daily expenses, or for financial goals which are coming soon

Having said that, you may not want to hold too much of it because of opportunity costs.

Apart from your short term financial commitments, consider holding at least 6-12 months of income/expenses as emergency funds. If you wish, you can hold a small percentage of total holdings as cash.

2) Bonds (Fixed Income)

When corporations and governments want to raise money, they may issue bonds.

When you’re buying a bond, you’re “lending” them money. In return, you’re entitled to receive coupons (interests) regularly, and at the end of the bond’s maturity, you can receive back your principal.

Bonds usually give higher expected returns compared to cash and its equivalents. Although it’s relatively low risk (depending on the credit rating of the corporation/government), there’s still a possibility that the bond issuer doesn’t pay out the agreed coupons and/or the principal back.

With a higher credit rating, the coupons are usually lower, and vice versa.

You can buy bonds through various methods:

- bond ETFs/unit trusts

- individual bonds from exchanges

- Singapore saving bonds (SSB)

- etc

The reason why you want to have bonds in your portfolio is because if you have too much in cash (too conservative), you may end up not hitting your financial goals. In addition, you’re not exposed to excessive risks.

And if you’re more aggressive, it also makes financial sense to hold some. It can act as a counter-weight to provide stability against the volatile equities, and be the ammunition to buy “cheap” equities when markets fall.

DID YOU KNOW? According to a survey conducted by MoneySense, about 3 out of 10 Singapore residents aged 30 to 59 had not started planning for their future financial needs. This isn't surprising because personal finance can seem complicated and daunting. But really, there are only a few things that you should focus on. Learn how to significantly improve your personal finances with the 7-step "wedding cake" strategy today.

3) Equities (Stocks & Shares)

When you buy a stock, you’re essentially buying an ownership of that business.

Stocks usually represent the growth element in your portfolio.

Although they have higher risk in the form of volatility (the value can fluctuate greatly) and potential loss of capital, the expected returns can be potentially high as well.

In general, when we look at long term, equities tend to outperform other asset classes. This is especially so when you’re able to select high quality value stocks.

Some form of risk is good (depending on your risk profile).

Because if you don’t participate in any and you’re relying purely on your income and savings, you may not hit your desired financial goals. But if you can achieve them without any risks, then that’s a whole different matter entirely.

Most equities can be bought via:

- individual stocks and shares at exchanges

- ETFs

- index funds

- unit trusts

- etc

3 Reasons Why Asset Allocation Is Crucial

Here are some reasons why you should have an asset allocation in place:

1) Start with the bigger picture

All of us are humans. We want the highest possible returns at the lowest risks.

The deciding factors will always be how much risk can we tolerate and how far are you towards your financial goals.

If you belong to the aggressive category, yet you’re able to achieve your goals easily by just earning an income from your career/business and holding cash, would you even want to put yourself in risky situations?

If you’re more conservative, and don’t even want to look at options that have volatility and potential loss of capital, and just want to keep your money in safer options, can you even hit your goals?

In consideration of all these, having an asset allocation would allow you to have a starting point, and come to a comfortable mix.

After that, you can even break the allocation down even further by subclasses (e.g split for equities: 30% US, 30% China, 40% Singapore).

2) Diversifying minimises risks

It all starts with knowing what type of risk profile you have.

Whichever you are, diversification can help. The act of having an asset allocation is diversification in itself.

Equities provide the volatile side while generally bonds provide the less volatile side.

And in the long run, as long as you’ve chosen proper investments, both would generally rise, even though they’ll experience falls in markets, from time to time.

Traditionally, when equities rise, bonds fall, and vice versa. Although there are times when both rise/fall together, they’re not expected to do that forever.

Why is this important?

Moving against each other (but growing in the long run) will ensure that most of the times, your portfolio won’t see a sea of red.

Diversifying ensures that you’re benefitting from upsides, while minimising downsides.

3) Eliminate emotions and overthinking which can drain you

By sticking to the ratio, you’re setting guidelines to follow no matter what may come.

It also simplifies your thought process.

By eliminating emotions and irrational thoughts, you won’t get affected by every single thing.

If you’ve done some investing before, you’d realise all these may consume you. You would think that every small aspect matters (and that could be true), but if we zoom out to the bigger picture by letting it do its thing, it should work out in the end.

With all these reasons, see how an asset allocation can play out in different scenarios.

Example of a Simple Asset Allocation Strategy by Age

When you’re young, you can afford to take more risks to achieve the highest potential returns. Because if it doesn’t work out well, you have the luxury of time for markets to recover.

This isn’t the same when you’re old and time is severely limited.

(On a side note, this corresponds to how investment strategies for retirement work.)

In fact, in my view, volatile investments should only be held for the longer term. If you’re investing for the short term, non-volatile assets may be more suitable.

A very common model of asset allocation is this:

The percentage of equities you should hold equals (100 minus your age).

So if you’re 30 years old, then 70% in equities and 30% in bonds.

Of course, this is just a starting point.

With the life expectancy in Singapore increasing, it means that we have a longer time horizon as well. As such, you may even consider (110 or 120 minus your age).

Although age (and thus long time horizon) plays a part, you can still have a ratio according to your risk preferences.

A conservative investor generally has a larger bond-to-equity ratio. And an aggressive investor would have a larger equity-to-bond ratio.

If you’ve no idea where to start with, you can approach a financial advisor. In the Know Your Client (KYC), there’s a risk assessment.

Keep Your Eggs in Baskets and Have Money to Buy More

The above asset allocation strategy itself is simple.

This section goes even deeper to explain the rationale of having an equity/bond ratio.

It spells out some scenarios and how all that we talked about will play out.

I’m also taking the following opinion:

Equities provide growth and bonds provide stability. Within each asset class, there should be further diversification too.

Over the long run, equities outperform other asset classes. There will be times when markets rise, and fall. When markets fall, given time, it’ll recover. As it’s falling or have fallen, it could be a good time to buy more equities because they’re “cheap”.

Although that is easier said than done, throughout an investment journey, most of us would’ve faced emotions – greed and fear – that will affect our decisions.

For example:

When equities rise, it may seem like it’s getting expensive and that puts us off investing more but we shouldn’t discount the fact that it can rise further. At the very same time, it can be “overvalued”, so would it be a good time to sell?

If equities fall, what if it falls further? Should I sell now? Or should I buy more because it’s “cheaper” now?

Considering that we can’t really time the market, and we may not be experts, what can we rely on to make this decision for us?

That’s when your equity-bond ratio comes in.

When that ratio changes, this is a very simplified way of saying, “hey, your equities are getting cheaper. Remember your ratio? It’s time to stick with it.”

That way, you’ll want to buy more equities by selling some bonds (bonds are your ammunition when there are bargains to be bought).

This brings us to the next point..

The Act of Rebalancing

Continuing from the previous section, rebalancing is meant to stick to the asset allocation ratio you’ve set for yourself.

It means to sell off some of the overweighted asset and buy the underweighted one so that the ratio is back again.

So for example, if say you have 50/50 equity-bond ratio, and when equities prices go up, it becomes 70/30.

This may mean that you’re holding too much equities (and risk) so you want to sell off some of these equities and use the proceeds to buy bonds. The thinking behind this is also to lock in profits from equities and fortifying it using bonds.

If equities prices go low, and it becomes 30/70 instead:

That would mean to sell off some bonds and buy equities to maintain that 50/50 ratio. This ensures that with the ammunition you have from bonds, you can use it to buy equities which are deemed “cheaper” now.

Rebalancing helps you to keep your sanity. With this simple guideline, you wouldn’t be bogged down by emotions and constantly think of what’s your next action would be. This allows to concentrate on the more important things in life – career/business, personal and family relationships.

When to rebalance is entirely up to you. It can be automatic or manual depending on the platform you subscribe to.

And if you have excess cash, you can also consider injecting new funds and buying the underweighted asset class.

Other Asset Classes to Take Note of

Apart from cash, bonds, and equities, there are other assets out there.

They can be applicable depending on your needs and preferences.

Examples of such assets:

- Residential/commercial property

- REITs

- Retirement annuity plans

- Commodities like gold and silver

- etc

You can include them into your asset mix.

What’s Next?

Investing is an important topic to know about.

From the money we’ve earned from our employment and/or business, it needs to be put into better use.

To start off, it’s always good to know WHY we want to invest. For what purpose?

Is it because you want to plan for your retirement? Cater for your kid’s education? General savings/investment?

Knowing your why alters what type of investments to make as well.

So take a step back, and start from that big picture thinking.